Market moods turned sour again today as outbreak of the coronavirus seems to be getting more serious outside China. In particular, South Korea cases surged by 52 to 156. In China, there were 889 new confirmed cases yesterday, with total accumulated cases rose to 75465. China’s Science and Technology said vaccine could be submitted for clinical trials around late April. But that’s firstly too late for containing the outbreak. Secondly, markets just ignore such comments.

In the currency markets, New Zealand and Australian Dollars are trading as the weakest for today while Yen recovers. However, Yen remains the weakest one for the week on concern of economic and political impact of the coronavirus that originated in China. Canadian and Dollar are currently the strongest for the week.

Technically, 0.6583 projection level in AUD/USD will be a level to watch today. There is prospect of bottoming there, but sustained break will likely bring further downside acceleration. 1.0608 in EUR/CHF is another level to watch. Break there will resume larger down trend. More importantly, that might drag USD/CHF away from 0.9851 fibonacci resistance.

In Asia, Nikkei is currently down -0.11%. Hong Kong HSI is down -0.73%. China Shanghai SSE rose 0.46%. Singapore Strait Times rose 0.01%. Japan 10-year JGB yield is down -0.0245 to -0.063. Overnight, DOW dropped -0.44%. S&P 500 dropped -0.38%. NASDAQ dropped -0.67%. 10-year yield dropped -0.045 to 1.525.

Japan national CPI core rose to 0.8%, but core-core slowed

Japan national CPI core (all items ex-fresh food), rose to 0.8% yoy in January, up from 0.7% yoy, matched expectations. But it remains well below BoJ’s 2% target. Headline CPI slowed to 0.7% yoy, down form 0.8% yoy. CPI core-core (all items ex-fresh food, energy slowed to 0.8% yoy, down fro 0.9% yoy.

BoJ Governor Haruhiko Kuroda told the parliament today that he saw the economy to continue with moderate recovery. The central bank won’t hesitate to take additional easing measures if necessary. But he didn’t believe it’s needed now.

Kuroda added that uncertainty regarding China’s coronavirus outbreak is high, because of the impact on exports, production, and tourism. He’d watching the effects with “grave concern.” Also, the coronavirus will be the “biggest topic on the agenda” at this week’s G20 meeting.

Japan PMI composite dropped to 47.0, Q1 recovery hope dashed

Japan PMI Manufacturing dropped to 47.6 in February, down from 48.8. PMI services dropped to sharply to 46.7, down from 51.0, dipped into contraction. PMI Composite also dropped to 47.0, down from 50.1, now in contraction too.

Joe Hayes, Economist at IHS Markit, said: “latest PMI data dash any hopes of a first quarter recovery in Japan and significantly raise the prospect of a technical recession”. February’s data “stack the odds heavily against Q1 growth, despite Abe’s best efforts to stimulate the economy after the sales tax hike”.

Australia PMI composite dropped to 48.3, fiscal stimulus needed

Australia CBA PMI Manufacturing rose 0.2 to 49.8 in February, up from 49.6. However, PMI Services dropped to 48.4, down from 50.6. PMI Composite also turned into contraction at 48.3, down from 50.2. The rate of output reduction was the “steepest seen since data collection began in May 2016”. Panel membered linked this to “a combination of subdued client demand, adverse weather and the Covid-19 outbreak”.

CBA Senior Economist, Gareth Aird said: “The February flash PMIs imply a contraction in private demand. Whilst this is clearly a disappointing result, it is not altogether surprising given the two exogenous shocks that have hit the Australian economy – the bushfires and the coronavirus (Covid-19).”

“Our main concern is that these event have hit the global and local economies at a time when domestic demand was already soft. The level of both the services and manufacturing PMIs highlights the need for more policy stimulus. With monetary policy doing most of the heavy lifting an easing in fiscal policy continues to look the most appropriate response to support aggregate demand.”

Looking ahead

Eurozone and UK PMIs will be the major focuses in European session. In particular, poor readings from Eurozone could trigger new round of selloff in Euro. Eurozone will also release CPI final. Later in the day, Canada will release retail sales. US will release PMIs and existing home sales.

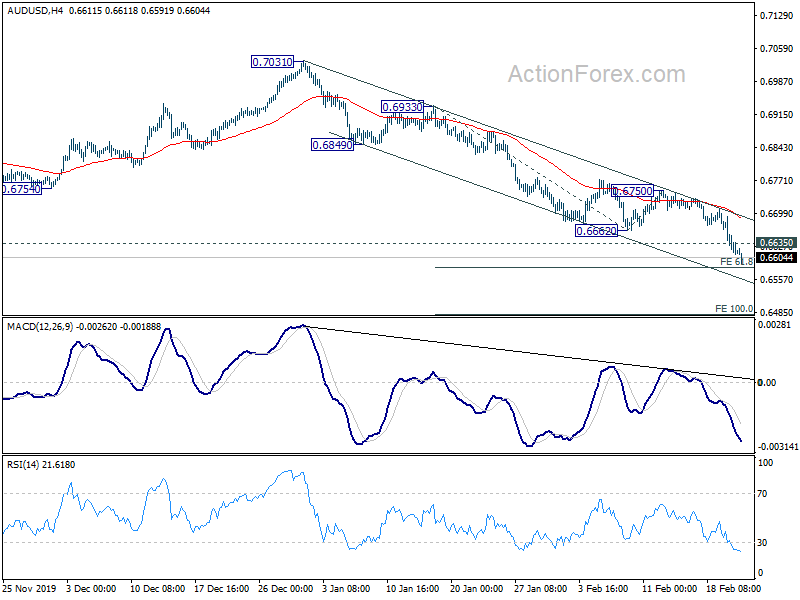

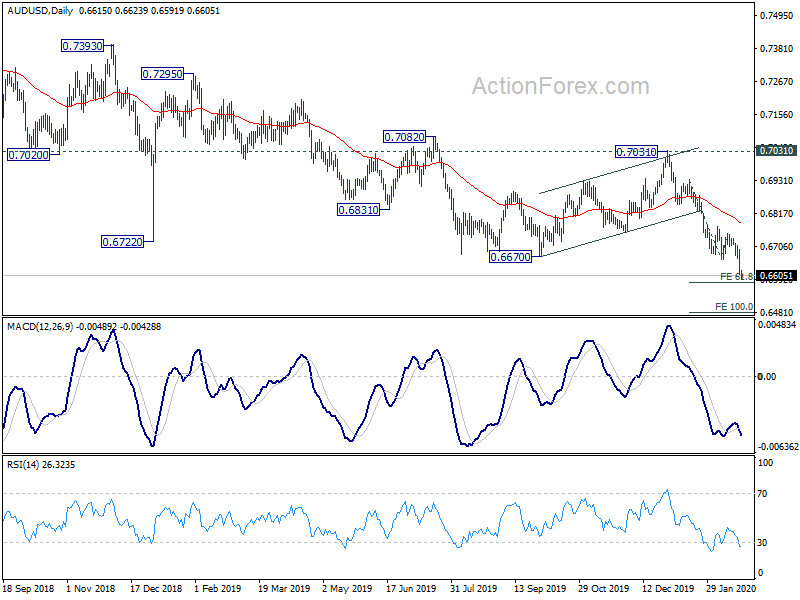

AUD/USD Daily Report

Daily Pivots: (S1) 0.6584; (P) 0.6639; (R1) 0.6669; More….

AUD/USD’s decline continues today and reaches as low as 0.6591 so far. Intraday bias remains on the downside for deeper decline. Break of 61.8% projection of 0.6933 to 0.6662 from 0.6750 at 0.6583 will pave the way to 100% projection at 0.6479. On the upside, above 0.6635 minor resistance will turn intraday bias neutral first. But recovery should be limited below 0.6750 resistance to bring fall resumption.

In the bigger picture, AUD/USD’s decline from 0.8135 (2018 high) is still in progress. It’s part of the larger down trend from 1.1079 (2011 high). Rejection by 55 week EMA affirms medium term bearishness. Next target is 0.6008 (2008 low). Outlook will stay bearish as long as 0.7031 resistance holds, even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:00 | AUD | CBA Manufacturing PMI Feb P | 49.8 | 49.6 | ||

| 22:00 | AUD | CBA Services PMI Feb P | 48.4 | 50.6 | ||

| 23:30 | JPY | National CPI Core Y/Y Jan | 0.80% | 0.70% | 0.70% | |

| 0:30 | JPY | Manufacturing PMI Feb P | 47.6 | 48.8 | ||

| 4:30 | JPY | All Industry Activity Index M/M Dec | 0.30% | 0.90% | ||

| 8:15 | EUR | France Manufacturing PMI Feb P | 50.7 | 51.1 | ||

| 8:15 | EUR | France Services PMI Feb P | 51.2 | 51 | ||

| 8:30 | EUR | Germany Manufacturing PMI Feb P | 44.8 | 45.3 | ||

| 8:30 | EUR | Germany Services PMI Feb P | 54 | 54.2 | ||

| 9:00 | EUR | Eurozone Manufacturing PMI Feb P | 47.5 | 47.9 | ||

| 9:00 | EUR | Eurozone Services PMI Feb P | 52.2 | 52.5 | ||

| 9:30 | GBP | Manufacturing PMI Feb P | 49.7 | 50 | ||

| 9:30 | GBP | Services PMI Feb P | 53.4 | 53.9 | ||

| 9:30 | GBP | Public Sector Net Borrowing (GBP) Jan | -12.0B | 4.0B | ||

| 10:00 | EUR | CPI M/M Jan F | -1.00% | 0.30% | ||

| 10:00 | EUR | CPI Y/Y Jan F | 1.40% | 1.40% | ||

| 10:00 | EUR | CPI – Core Y/Y Jan F | 1.10% | 1.10% | ||

| 13:30 | CAD | Retail Sales M/M Dec | 0.00% | 0.90% | ||

| 13:30 | CAD | Retail Sales ex Autos M/M Dec | 0.40% | 0.20% | ||

| 14:45 | USD | Manufacturing PMI Feb P | 51.4 | 51.9 | ||

| 14:45 | USD | Services PMI Feb P | 53.5 | 53.4 | ||

| 15:00 | USD | Existing Home Sales Jan | 5.48M | 5.54M |

{kind=link}