Global stock market crash on fear of Wuhan coronavirus pandemic continues today, while treasury yields are pressured too. Euro and Swiss Franc are currently the strongest ones. There are a couple of explanations, like safe haven flows out of US, due to free fall in stocks, as well as record low treasury yields. But we believe it’s more about repricing of impact on the economy. Euro took the lead down weeks ago, as the Eurozone economy, in particular export-led Germany, would be hit harder than US if the coronavirus outbreak is contained within China. But now, when every countries in dragged into it, traders are reversing the overstretched Euro bearishness.

Staying in the currency markets, Canadian Dollar is currently the weakest one, as oil’s free fall accelerates too. WTI is currently at 46.8, well on track to retest 42.05 low. Sterling is the second weakest after UK’s Brexit negotiation mandate showed it threatens to walk out from talks as soon as in June. Dollar is soft too, but weakness is not apparent, except against Euro and Swiss. The greenback’s resilience is somewhat reflected in range trading in gold too.

In US, DOW future is currently down -390 pts. 10-year yield is at new 1.275 after hitting new record low. In Europe, FTSE is down -2.88%. DAX is down -2.97%. CAC is down -3.07%. German 10-year yield is down -0.042 at -0.544. earlier in Asia, Nikkei dropped -2.13%. Hong Kong HSI rose 0.31%. China Shanghai SSE rose 0.11%. Singapore Strait Times dropped -0.19%. Japan 10-year JGB yield dropped -0.0094 to -0.103.

US durable goods orders dropped -0.2%, ex-transport orders rose 0.9%

US durable goods orders dropped -0.2% in January to USD 246.2B, better than expectation of -1.5% decline. Ex-transport orders rose 0.9%, above expectation of 0.2%. Ex-defense orders rose 3.6%.

The second estimate of US Q4 GDP showed 2.1% annualized growth, unrevised, unchanged from Q3’s reading. PCE price index was revised down from 1.6% to 1.3%. PCE core index was also revised down from 1.3% to 1.2%.

Initial jobless claims rose 8k to 219k in the week ending February 22, above expectation of 211k. Four-week moving average of initial claims rose 0.5k to 209.75k. Continuing claims dropped -9k to 1.724m in the week ending February 15. Four-week moving average of continuing claims rose 5.25k to 1.729m.

UK threatens to move our from negotiation with EU by June

UK government published today the negotiation mandate with EU in the document titled “The Future Relationship with the EU The UK’s Approach to Negotiations“. There the UK government threatens to walk out from the table by June if not enough progress is made.

UK reiterated that it “will not extend the transition period”. That still “leaves a limited but sufficient” time to reach an agreement. After an “appropriate number of negotiating rounds” between now and June, UK would hope that “the broad outline of an agreement would be clear and be capable of being rapidly finalised by September”.

However, “if that does not seem to be the case at the June meeting, the Government will need to decide whether the UK’s attention should move away from negotiations and focus solely on continuing domestic preparations to exit the transition period in an orderly fashion.”

Cabinet office minister Michael Gove told parliament that “a the end of the transition period on the 31st of December, the United Kingdom will fully recover its economic and political independence. We want the best possible trading relationship with the EU, but in pursuit of a deal we will not trade away our sovereignty.”

ECB Schnabel: We are very worried about spread of coronavirus

ECB Executive Board member Isabel Schnabel said policymakers are “very worried about what is currently happening with respect to the spread of the coronavirus.” “We know that this is really raising uncertainty to a large degree, for the global growth outlook but of course also for the outlook for the euro area.”

“But what we really need to understand when we are doing monetary policy is what are the potential medium-term implications, and at the moment this is unclear”, she added.

Eurozone economic sentiment rose to 103.5, on stronger consumers and industry managers

Eurozone economic sentiment indicator rose to 103.5 in February, up from 102.6, beat expectation of 101.5. The improvement resulted from higher confidence among consumers and, to a lesser extent, industry managers. Looking at some details, industry confidence rose from -7.0 to -6.1. Services confidence edged up from 11.0 to 11.2. Consumer confidence rose fro -8.1 to -6.6. Retail trade confidence dropped slightly from -0.1 to -0.2. Construction confidence dropped from 5.8 to 5.3.

Amongst the largest euro-area economies, the ESI saw marked improvements in the Netherlands (+2.0), France (+1.9) and Spain (+1.2), while a more moderate one in Germany (+0.6). Sentiment in Italy remained flat (+0.0).

BoJ Kataoka: Coronavirus outbreak may weaken consumption and capital expenditure

BoJ known dove Goushi Kataoka warned today coronavirus out break could hurt consumption and poses uncertainty to the economy. He called by stronger actions by the central bank. He said, “we need to be mindful that consumption may weaken further as a trend”, and, “worsening sentiment among automakers and retailers could also affect the outlook for capital expenditure.”

In his view, BoJ should deepen the negative interest rate further. Additionally, it’s “very important” for government and the central bank to coordinate their policies. He added, “I believe there’s room for the BOJ to review its policy framework and re-examine its effect including how it interacts with fiscal and pro-growth policies.”

Separately, Deputy Governor Masayoshi Amamiya said that with digital currencies, central banks could stifle private-sector financial innovation and draw money away from deposits at commercial banks. However, central banks must also conduct a “comprehensive study” on how digital currencies would affect their settlement and financial systems.

Bank of Korean stands pat, micro support for businesses more effective than rate cut

Bank of Korea defied some expectations and kept base rate unchanged at 1.25%, despite intensifying coronavirus outbreak in the country. The decision was not unanimous, though, as two board members voted for a cut.

Governor Lee Ju-yeo wide reaching rate cut is not the appropriate response to the outbreak at this instead. Instead, there should be targeted support for companies that are most affected. “A health security crisis is the cause of the current economic difficulties,” he said. “In a situation like that, micro support for self-employed businesses and companies in trouble is more effective than an interest-rate cut.”

Nevertheless, the central bank lowered this year’s growth forecasts from 2.3% to 2.1%. Lee said, “the revised outlook of 2.1 percent is based on the assumption that the new coronavirus (COVID-19) outbreak would peak out in March.” Further downgrade is possible is the outbreak lasts beyond Q1.

PBoC pledges ample liquidity and targeted support

China’s PBoC insisted that economy goals for 2020 can still be achieved in spite of the coronavirus outbreak, and pledged to have measures to ensure ample liquidity. Liu Guoqiang, Vice Governor of PBoC said “We’ll further release the long-term liquidity via multiple open market operations. And make targeted RRR cuts in appropriate time for banks that meet the requirement of releasing inclusive loans and serve the smaller firms.”

Xiao Yuanqi, the chief risk officer of the China’s Banking and Insurance Regulatory Commission emphasized “Support policies are mainly for smaller firms facing difficulties because of the virus outbreak, not those in difficult situations before. We’ll prevent non-performing companies from getting a free ride from the push, and prevent related moral hazard.”

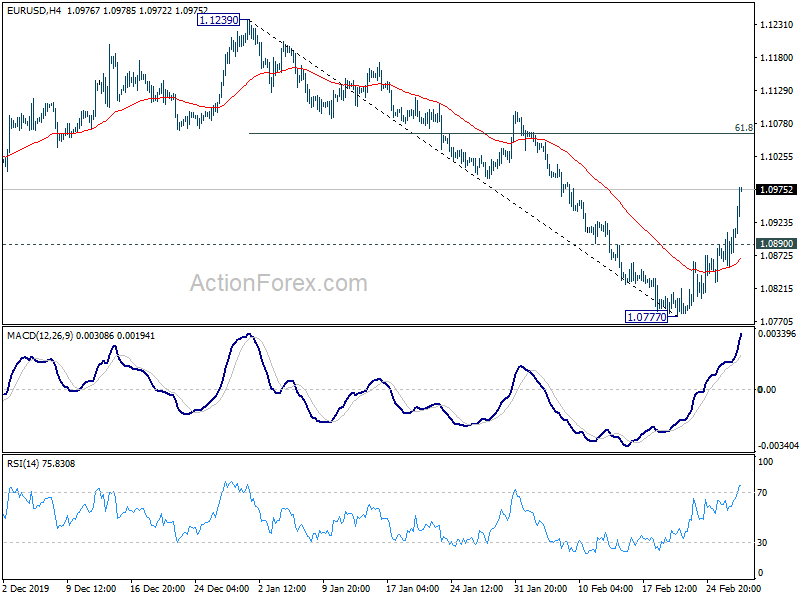

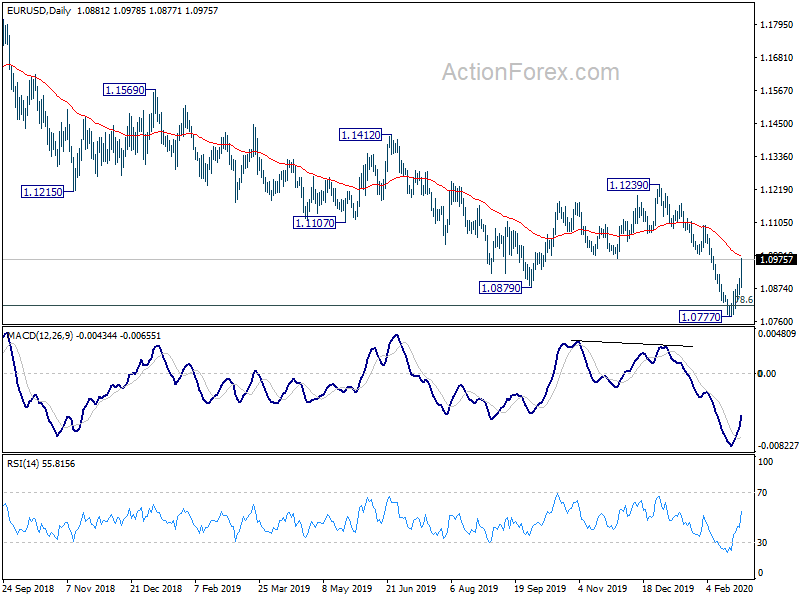

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0853; (P) 1.0881; (R1) 1.0907; More…

EUR/USD’s rebound from 1.0777 extends further to as high as 1.0978 today. The strength suggests that it’s corrective whole fall from 1.1239 to 1.0777. Intraday bias remains on the upside for 61.8% retracement of 1.1239 to 1.0777 at 1.1063 next. We’d expect strong resistance from there to limit upside. Below 1.0890 minor support will turn bias to the downside for retesting 1.0777 low. However, sustained break of 1.1063 will raise the chance of larger reversal and target 1.1239 key resistance.

In the bigger picture, down trend from 1.2555 (2018 high) has just resumed and prior rejection by 55 week EMA affirms medium term bearishness. Sustained break of 78.6% retracement of 1.0339 (2017 low) to 1.2555 at 1.0813 will pave the way to retest 1.0339 low. For now, outlook will remain bearish as long as 1.1239 resistance holds, in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Jan | -340M | -530M | 547M | 384M |

| 00:00 | NZD | ANZ Business Confidence Jan | -19.4 | -13.2 | ||

| 00:30 | AUD | Private Capital Expenditure Q4 | -2.80% | 0.50% | -0.20% | -0.40% |

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Jan | 5.20% | 5.50% | 5.00% | 4.90% |

| 09:00 | EUR | Private Loans Y/Y Jan | 3.70% | 3.70% | 3.70% | |

| 10:00 | EUR | Eurozone Business Climate Feb | -0.04 | -0.24 | -0.23 | |

| 10:00 | EUR | Eurozone Economic Sentiment Feb | 103.5 | 101.5 | 102.8 | 102.6 |

| 10:00 | EUR | Eurozone Industrial Confidence Feb | -6.1 | -7.8 | -7.3 | -7 |

| 10:00 | EUR | Eurozone Services Sentiment Feb | 11.2 | 10.8 | 11 | |

| 10:00 | EUR | Eurozone Consumer Confidence Feb F | -6.6 | -6.6 | -6.6 | -8.1 |

| 13:30 | CAD | Current Account (CAD) Q4 | -8.8B | -9.00B | -9.86B | -10.9B |

| 13:30 | USD | Initial Jobless Claims (Feb 21) | 219K | 211K | 210K | 211K |

| 13:30 | USD | GDP Annualized Q4 P | 2.10% | 2.10% | 2.10% | |

| 13:30 | USD | GDP Price Index Q4 P | 1.30% | 1.40% | 1.40% | |

| 13:30 | USD | Durable Goods Orders Jan | -0.20% | -1.50% | 2.40% | 2.90% |

| 13:30 | USD | Durable Goods Orders ex Transportation Jan | 0.90% | 0.20% | -0.10% | 0.10% |

| 15:00 | USD | Pending Home Sales M/M Jan | 2.00% | -4.90% | ||

| 15:30 | USD | Natural Gas Storage | -158B | -151B |

{kind=link}