Neither fiscal nor monetary stimulus is able to provide sustainable support to market so far. Stock markets are back under pressure today despite the massive USD 1T stimulus proposal by the US. Additionally, sentiments are pressured by the sudden spike in Italian treasury yields, and break of a key support level in oil price. Coronavirus pandemic continues to spread all over Europe.

In the currency markets, Australian Dollar is currently the weakest one for today, followed by Canadian and then New Zealand. Yen is the strongest, together with Swiss Franc and Dollar. Technically, WTI crude oil beaks through 27.50/69 key support zone decisive break, and it’s trading below 25 handle. WTI is extending long term down trend, possibly targeting long term support zone between 10.65 and 17.12 made between 1998/2001. GBP/USD’s break of 1.1946 key support also confirms long term down trend resumption. We might see GBP/JPY breaks corresponding support zone of 122.75/126.54 soon.

In Europe, currently, FTSE is down -4.57%. DAX is down -5.06%. CAC is down -5.53%. German 10-year yield is up 0.163 at -0.270. Earlier in Asia, Nikkei dropped -1.68%. Hong Kong HSI dropped -4.18%. China Shanghai SSE dropped -1.83%. Singapore Strait Times dropped -1.18%. Japan 10-year JGB yield rose 0.0582 to 0.066.

Canada CPI slowed to 2.2%, impact of coronavirus to be more deeply felt in subsequent months

Canada CPI slowed to 2.2% yoy in February, down from 2.4% yoy, but beat expectation of 2.1% yoy. CPI common was unchanged at 1.8% yoy, matched expectations. CPI median slowed to 2.1% yoy, down from 2.2% yoy, missed expectation of 2.2% yoy. CPI trimmed slowed to 2.0% yoy, down from 2.1% yoy, missed expectation of 2.1% yoy.

Statistics Canada commented on the impact of coronavirus on CPI. Flight suspensions, travel advisories and cancellations of public evens may leader to lower prices for trave services. Crude oil prices tumbled due to slow down in activity and travel, as well as tensions between oil-producing nations. Also, there are supply chain disruptions, closure of stores and services, lower interest rates and slowing of economic activity. “The price effects of the outbreak could be more deeply felt in subsequent months.”

From US, housing starts dropped to 1.46m annualized rate in February, below expectation of 1.51m. Building permits dropped to 1.60m, above expectation of 1.50m.

ECB reiterates readiness to adjust policy after communication chaos

ECB Executive Board member Isabel Schnabel told German news paper Die Zeit that the central bank is “ready to do everything in its mandate to counter market turmoil that disrupts monetary policy transmission, otherwise monetary policy cannot function,””. But she also cautioned against overestimating the power of central banks, and emphasized monetary policy alone could not solve the problem of coronavirus pandemic.

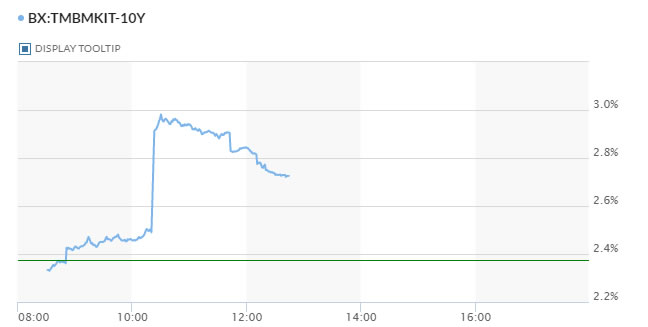

Italy’s 10-year benchmark yield spiked to as high as 2.983 earlier today, on comments from Austrian central bank head Robert Holzmann that ECB’s policy was at its limit. Additionally, Italy is the most serious epicenter of the pandemic in Europe. Holzmann’s comments problem and ECB official response, saying that the March 12 decision was unanimous and it stands ready to adjust all of its measures. Holzmann himself later also clarified that “”Monetary policy has not yet reached its limits, not by a long stretch.”

Eurozone CPI finalized at 1.2%, services the biggest contributor

Eurozone CPI was finalized at 1.2% yoy in February, slowed from 1.4% yoy. The largest contribution came from services (+0.72%), followed by food, alcohol & tobacco (+0.41%), non-energy industrial goods (+0.13%) and energy (-0.03%).

EU27 CPI was finalized at 1.6% yoy, down from 1.7% yoy. The lowest annual rates were registered in Italy (0.2%), Greece (0.4%) and Portugal (0.5%). The highest annual rates were recorded in Hungary (4.4%), Poland (4.1%) and Czechia (3.7%). Compared with January, annual inflation fell in twenty-one Member States, remained stable in one and rose in five.

Also from Eurozone, trade surplus came in at EUR 17.3B, below expectation of EUR 93.B.

Released earlier, New Zealand current account deficit narrowed to NZD -2.66B in Q4, versus expectation of NZD -2.83B. Australia leading index dropped -0.4% mom in February. Japan trade balance showed JPY 0.50T surplus in February, versus expectation of JPY 0.54T.

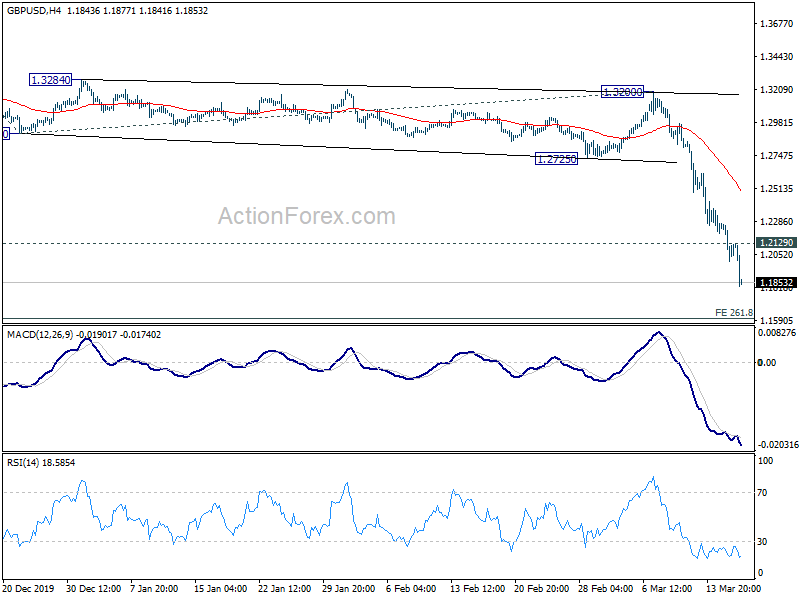

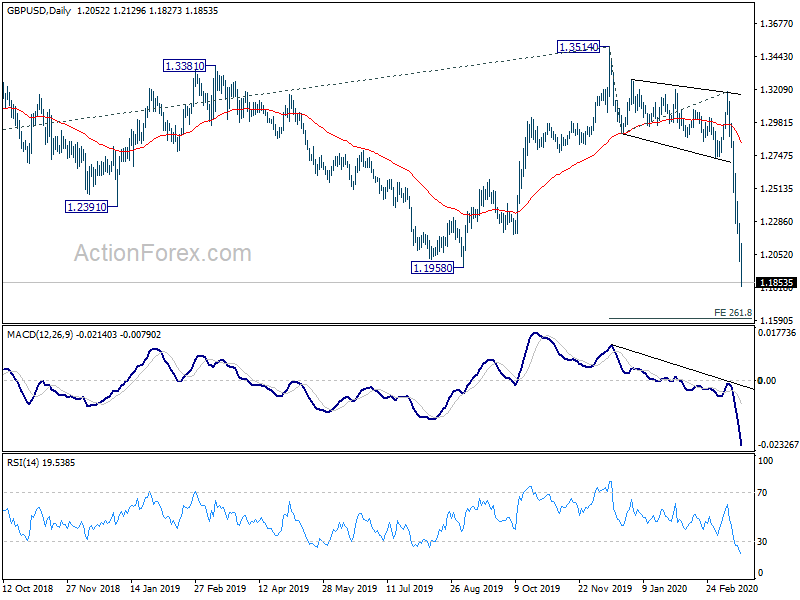

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1950; (P) 1.2112; (R1) 1.2221; More…

GBP/USD drops to as low as 1.1827 so far. Break of 1.1946/58 key support confirms larger down trend resumption. Intraday bias stays on the downside. Next near term target is 261.8% projection of 1.3514 to 1.2905 from 1.3200 at 1.1606 next. On the upside, above 1.2129 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another fall.

In the bigger picture, break of 1.1946 (2016 low) indicates that larger down trend from 2.1161 (2007 high is resuming). Next medium term target will be 61.8% projection of 1.7190 to 1.1946 from 1.3514 at 1.0273. In any case, outlook will remain bearish as long as 1.3514 resistance holds, in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Current Account (NZD) Q4 | -2.66B | -2.83B | -6.35B | -6.26B |

| 23:30 | AUD | Westpac Leading Index M/M Feb | -0.40% | 0.10% | 0.00% | |

| 23:50 | JPY | Trade Balance (JPY) Feb | 0.50T | 0.54T | -0.22T | -0.08T |

| 10:00 | EUR | Eurozone Trade Balance (EUR) Jan | 17.3B | 19.3B | 22.2B | |

| 10:00 | EUR | Eurozone CPI Y/Y Feb | 1.20% | 1.20% | 1.20% | |

| 10:00 | EUR | Eurozone CPI Core Y/Y Feb | 1.20% | 1.20% | 1.20% | |

| 11:00 | USD | MBA Mortgage Applications (Mar 13) | -8.40% | 55.40% | ||

| 12:30 | USD | Building Permits Feb | 1.60M | 1.50M | 1.55M | 1.62M |

| 12:30 | USD | Housing Starts Feb | 1.46M | 1.51M | 1.57M | 1.55M |

| 12:30 | CAD | CPI M/M Feb | 0.40% | 0.40% | 0.30% | |

| 12:30 | CAD | CPI Y/Y Feb | 2.20% | 2.10% | 2.40% | |

| 12:30 | CAD | CPI Common Y/Y Feb | 1.80% | 1.80% | 1.80% | |

| 12:30 | CAD | CPI Median Y/Y Feb | 2.10% | 2.20% | 2.20% | |

| 12:30 | CAD | CPI Trimmed Y/Y Feb | 2.00% | 2.10% | 2.10% | |

| 14:30 | USD | Crude Oil Inventories | 3.5M | 7.7M |

{kind=link}