The forex markets are generally in range trading today, with mild weakness seen in Sterling after CPI release. Markets are staying in mild risk-on mode, with Australian Dollar and Canadian Dollar firmer. However, there is no one-sided risk trading as see in the divergence in Yen and Swiss Franc. Markets will look forward to Fed Chair Jerome Powell’s testimony again today. But he’s unlikely to provide any fresh inspirations.

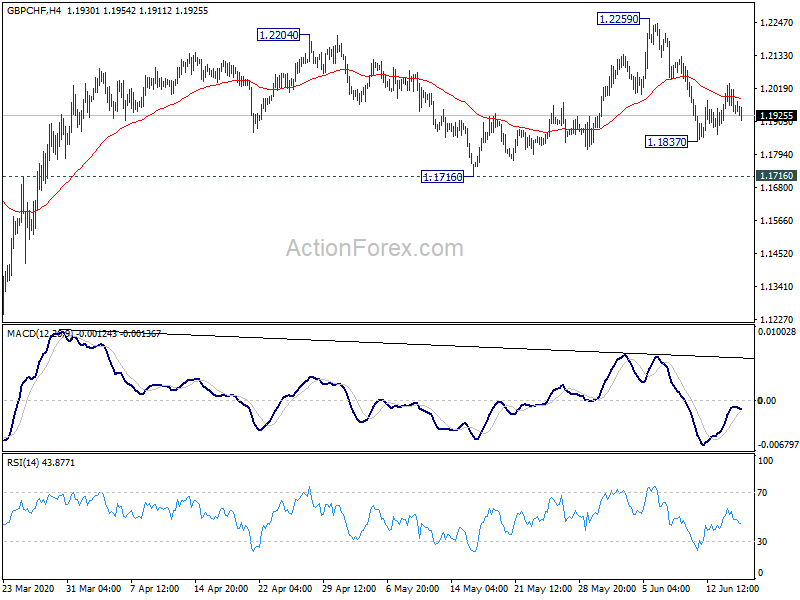

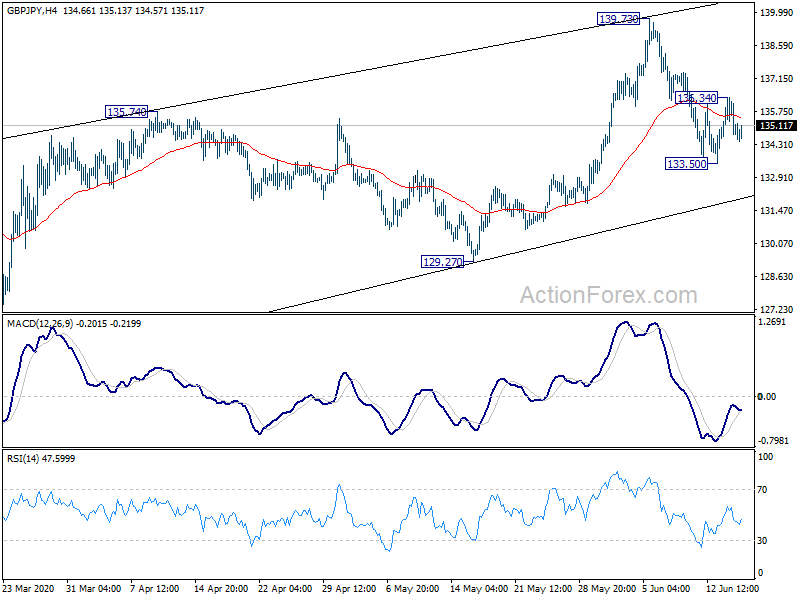

Technically, EUR/GBP is still engaging in range trading despite some volatility this week. With 0.8866 minor support intact, further rise is still in favor through 0.9054 at a later stage. GBP/JPY’s recovery also quickly lost steam after breaching 136.04 minor resistance. Focus could quickly turn back to 133.50 temporary low and break will resume recent fall from 139.73. GBP/CHF’s recovery also lost momentum after brief breach of 4 hour 55 EMA. Break of 1.1837 temporary low will extend the fall from 1.2259 to 1.1716 key near term support.

UK CPI slowed to 0.5% in May, lowest since 2016

UK CPI slowed further to 0.5% yoy in May, down from 0.8% yoy, matched expectations. That’s the lowest level since 2016. Nearly all categories of prices contributed to the decline in CPI, except food and non-alcoholic beverages. Core CPI dropped to 1.2% yoy, down from 1.4% yoy, matched expectations too.

Also released, RPI slowed to 1.0% yoy in May, down from 1.5% yoy, missed expectation of 1.3% yoy. PPI input came in at 0.3% mom, -10.0% yoy, versus expectation of -4.0% mom, -8.7% yoy. PPI output was at -0.3% mom, -1.4% yoy, versus expectation of -0.1% mom, -0.9% yoy. PPI output core was at 0.0% mom, 0.6% yoy versus expectation of 0.1% mom, 0.7% yoy.

RBNZ Orr confident with the plenty of tools

RBNZ Governor Adrian Orr said he’s “very pleased” with the impact of the central bank’s QE program. As for the next steps in monetary easing, he’s confidence that there are “plenty of tools”. But for now, the main game in town is about fiscal policy.

Orr added the next steps for RBNZ could include an increase in the size of QE, and the number of instruments included in the program. Also, negative case rate is still a possibility.

Asian business sentiment plunged to record low in Q2

The Thomson Reuters/ INSEAD Asian Business Sentiment index plunged to 35 in Q2, down from 53. That’s a 11-year low, and the second time the index fell below 50. Around 16% of the 93 companies surveyed said a “deepening recession” was a key risk for the next six months. More than half expects declining staffing and levels and business volumes.

“We ran this survey right at the edge when things were getting really bad,” said Antonio Fatas, economics professor at global business school INSEAD. “We can see this complete pessimism which is spread across sectors and countries in a way that we haven’t seen before.”

Fed Clarida: Inflation at risk of falling below the range consistent with target

Fed Vice Chair Richard Clarida said in a speech yesterday that before the current downturn, long-term inflation expectations were already “at the low end” of the range that’s consistent with Fed’s objective. Give the “likely depth of this downturn”, inflation expectations are “at risk of falling below” that range.

Hence, “I will place a high priority on advocating policies that will be directed at achieving not only maximum employment, but also well-anchored inflation expectations consistent with our 2 percent objective,” he added. “Depending on the course of the virus and the course of the economy, more support from both fiscal and monetary policy may be called for,” he added.

Looking ahead

Eurozone will release May CPI final in European session. Later in the day, Canada will release CPI. US will release housing starts and building permits.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 134.29; (P) 135.32; (R1) 135.92; More…

GBP/JPY’s recovery lost momentum after failing to sustain above 4 hour 55 EMA. Intraday bias is turned neutral first. On the upside, break of 136.34 minor resistance will extend the rebound from 133.50 to retest 139.73 high. On the downside, sustained break of 55 day EMA (now at 134.40) will argue that whole rebound from 123.94 has completed. Fall from 139.73 should then target 129.27 support to confirm this bearish case.

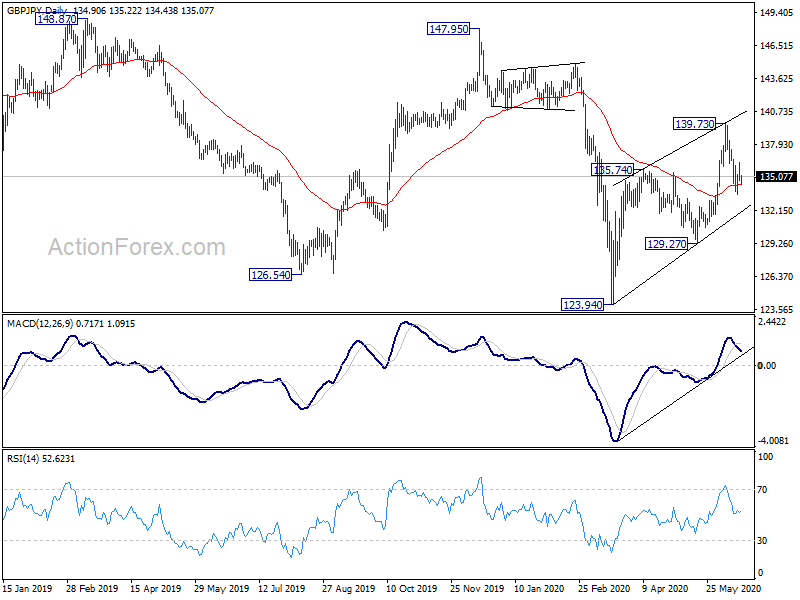

In the bigger picture, we’re still seeing price actions from 122.75 (2016 low) are seen as a sideway consolidation pattern. As long as 147.95 resistance holds, an eventual downside breakout remains in favor. however, firm break of 147.95 will raise the chance of long term bullish reversal. Focus will then be turned to 156.59 resistance for confirmation.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Current Account (NZD) Q1 | 1.56B | 1.59B | -2.66B | -2.77B |

| 23:50 | JPY | Trade Balance (JPY) May | -0.60T | -0.68T | -1.00T | -1.04T |

| 1:00 | AUD | Westpac Leading Index M/M May | 0.20% | -1.50% | ||

| 6:00 | GBP | CPI M/M May | 0.00% | 0.00% | -0.20% | |

| 6:00 | GBP | CPI Y/Y May | 0.50% | 0.50% | 0.80% | |

| 6:00 | GBP | Core CPI Y/Y May | 1.20% | 1.20% | 1.40% | |

| 6:00 | GBP | RPI M/M May | -0.10% | 0.10% | 0.00% | |

| 6:00 | GBP | RPI Y/Y May | 1.00% | 1.30% | 1.50% | |

| 6:00 | GBP | PPI Input M/M May | 0.30% | -4.00% | -5.10% | -5.50% |

| 6:00 | GBP | PPI Input Y/Y May | -10.00% | -8.70% | -9.80% | -10.20% |

| 6:00 | GBP | PPI Output M/M May | -0.30% | -0.10% | -0.70% | -0.80% |

| 6:00 | GBP | PPI Output Y/Y May | -1.40% | -0.90% | -0.70% | |

| 6:00 | GBP | PPI Output Core M/M May | 0.00% | 0.10% | -0.10% | 0.00% |

| 6:00 | GBP | PPI Output Core Y/Y May | 0.60% | 0.70% | 0.60% | 0.70% |

| 9:00 | EUR | Eurozone CPI Y/Y May F | 0.10% | 0.10% | ||

| 9:00 | EUR | Eurozone CPI Core Y/Y May F | 0.90% | 0.90% | ||

| 12:30 | USD | Housing Starts May | 1.10M | 0.89M | ||

| 12:30 | USD | Building Permits May | 1.23M | 1.07M | ||

| 12:30 | CAD | CPI M/M May | -0.70% | |||

| 12:30 | CAD | CPI Y/Y May | -0.20% | |||

| 12:30 | CAD | CPI Common Y/Y May | 1.60% | 1.60% | ||

| 12:30 | CAD | CPI Median Y/Y May | 1.90% | 2.00% | ||

| 12:30 | CAD | CPI Trimed Y/Y May | 1.70% | 1.80% | ||

| 14:30 | USD | Crude Oil Inventories | 5.7M | |||

| 16:00 | USD | Fed’s Chair Powell testifies |

{kind=link}