The overall markets remain rather mixed so far. Rebound in US stocks overnight didn’t carry forward to Asian session. Nikkei is weighed down by poor Tankan survey data. Dollar’s rally attempt was somewhat knocked down by up trend resumption in Gold. Recovery in oil prices also dragged down the greenback and lifted Canadian. Focus will now turn to US ADP employment and ISM manufacturing, as well as tomorrow’s NFP. Hopefully, these data could trigger some meaningful breakouts in the markets.

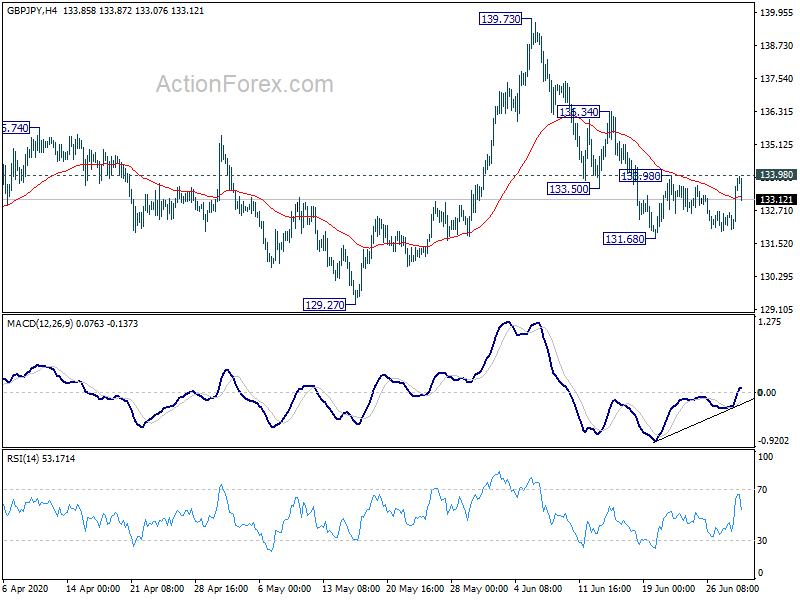

Technically, Gold’s break of 1779.16 indicates up trend resumption for 61.8% projection of 1451.16 to 1765.25 from 1670.66 at 1864.76. A focus now is how EUR/USD would follow, by breaking 1.1168 support, or 1.1348 minor resistance. EUR/GBP’s break of 0.9079 minor support suggests resistance from 0.9182 fibonacci level. GBP//USD’s breach of 1.2389 minor resistance also suggests temporary bottoming. But GBP/JPY’s recovery was rejected by 113.98 minor resistance. It remains to be seen in the Pound could stage a sustainable rebound.

In Asia, currently, Nikkei is down -0.21%. China Shanghai SSE is up 0.91%. Singapore Strait Times is up 0.96%. Hong Kong is on holiday. Japan 10-year JGB yield is up 0.018 at 0.051. Overnight, DOW rose 0.85%. S&P 500 rose 1.54%. NASDAQ rose 1.87%. 10-year yield rose 0.017 to 0.654.

Japan tankan large manufacturing dropped to -34, worst since 2009

BoJ’s Tankan large manufacturing index dropped to -34 in Q2, down from -8, hitting the lowest level since 2009. That’s also worse than expectation of -31. Manufacturing outlook for September dropped to -27. Large non-manufacturing index dropped to -17, slightly better than expectation of -18. Non-manufacturing outlook also dropped to -14, but beat expectation of -15. On the positive side, all large industry capex rose 3.2%, versus expectation of 2.1%.

Japan PMI manufacturing finalized at 50.1, change of V-shape recovery slim

Japan PMI Manufacturing was finalized at 50.1 in June, up from May’s 38.4. Markit noted that firms still operate full capacity due to slow-moving order books. Export demand declines as coronavirus disruptions linger on. But business confidence rebounds into positive territory.

Joe Hayes, Economist at IHS Markit, said: “The chance of a V-shape recovery in the manufacturing sector appears slim at this stage, which opens up the possibility of a two-speed economy if the domestic-focused service sector shows more signs of activity.”

Australia AiG manufacturing rose to 51.5, building approvals dropped -16.4%

Australia AiG Performance of Manufacturing Index rose 9.9 pts to 51.5 in June, back into expansion region. AiG said that this only “indicates an improvement from the depths of April and May, rather than a recovery to buoyant conditions”. Also, “almost all of the improvement in June was concentrated in the large food and beverages sector”.

Also released, total building approvals dropped -16.4% mom in May, much worse than expectation of -6.0% mom. Private sector houses dropped -4.4% mom. Private sector dwellings excluding houses dropped -34.9% mom.

From New Zealand, building permits rose 35.6% mom in May.

China Caixin PMI manufacturing rose to 51.2, limited impact from recent coronavirus flare up

China Caixin PMI Manufacturing rose to 51.2 in June, up from 50.7, beat expectation of 50.5. Markit said output expands again as sector continues to recover from the coronavirus crisis. Total new work increases for the first time since January, but external demand remains subdued.

Wang Zhe, Senior Economist at Caixin Insight Group said: “Around mid-June, the epidemic flared back up in some parts of China, but its impact on the overall economy was limited. The gauge for future output expectations continued to rise in June, reflecting manufacturers’ confidence that there would be a further relaxation of epidemic controls and a normalization of economic activities.”

Looking ahead

Germany will release retail sales and unemployment in European session. Eurozone and UK will release PMI manufacturing final. Swiss will release SVME PMI. Later in the day, US will release ADP employment, ISM manufacturing and construction spending. Fed will also release FOMC minutes.

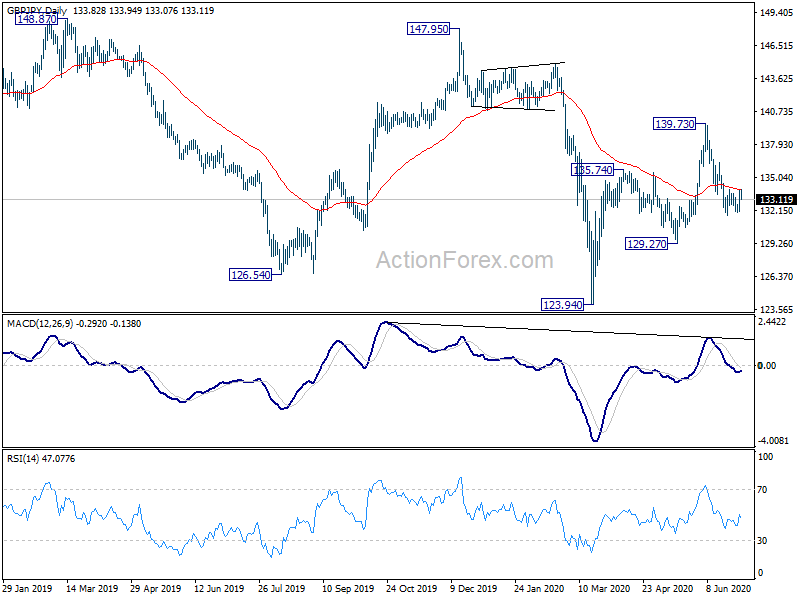

GBP/JPY Daily Outlook

Daily Pivots: (S1) 132.62; (P) 133.25; (R1) 134.49; More…

GBP/JPY failed to break through 131.98 minor resistance despite recovery. Intraday bias remains neutral first and further fall is in favor. On the downside, break 131.68 will resume the decline from 139.73 for 129.27 support. Decisive break there will confirm completion of rebound from 123.94. Deeper fall would be seen to retest 123.94 low. Nevertheless, firm break of 133.98 will now indicate short term bottoming and turn bias back to the upside for 136.34 resistance first.

In the bigger picture, we’re seeing price actions from 122.75 (2016 low) as a sideway consolidation pattern. As long as 147.95 resistance holds, an eventual downside breakout remains in favor. However, firm break of 147.95 will raise the chance of long term bullish reversal. Focus will then be turned to 156.59 resistance for confirmation.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Mfg Index Jun | 51.5 | 41.6 | ||

| 22:45 | NZD | Building Permits M/M May | 35.60% | -6.50% | -9.90% | |

| 23:01 | GBP | BRC Shop Price Index Y/Y May | -1.60% | -2.40% | ||

| 23:50 | JPY | Tankan Large Manufacturing Index Q2 | -34 | -31 | -8 | |

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q2 | -27 | -24 | -11 | |

| 23:50 | JPY | Tankan Non – Manufacturing Index Q2 | -17 | -18 | 8 | |

| 23:50 | JPY | Tankan Non – Manufacturing Outlook Q2 | -14 | -15 | -1 | |

| 23:50 | JPY | Tankan Large All Industry Capex Q2 | 3.20% | 2.10% | 1.80% | |

| 00:30 | JPY | Manufacturing PMI Jun | 40.1 | 37.8 | 37.8 | |

| 01:30 | AUD | Building Permits M/M May | -16.40% | -6.00% | -1.80% | -2.10% |

| 01:45 | CNY | Caixin Manufacturing PMI Jun | 51.2 | 50.5 | 50.7 | |

| 05:00 | JPY | Consumer Confidence Index Jun | 20.9 | 24 | ||

| 06:00 | EUR | Germany Retail Sales M/M May | 4.10% | -5.30% | ||

| 07:30 | CHF | SVME – PMI Jun | 48.1 | 42.1 | ||

| 07:45 | EUR | Italy Manufacturing PMI Jun | 48 | 45.4 | ||

| 07:50 | EUR | France Manufacturing PMI Jun F | 52.1 | 52.1 | ||

| 07:55 | EUR | Germany Unemployment Change Jun | 120K | 238K | ||

| 07:55 | EUR | Germany Unemployment Rate Jun | 6.60% | 6.30% | ||

| 07:55 | EUR | Germany Manufacturing PMI Jun F | 44.6 | 44.6 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Jun F | 46.9 | 46.9 | ||

| 08:30 | GBP | Manufacturing PMI Jun F | 50.1 | 50.1 | ||

| 11:30 | USD | Challenger Job Cuts Jun | 397.016K | |||

| 12:15 | USD | ADP Employment Change Jun | 3000K | -2760K | ||

| 13:45 | USD | Manufacturing PMI Jun F | 49.6 | 49.6 | ||

| 14:00 | USD | ISM Manufacturing PMI Jun | 49 | 43.1 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Jun | 36 | 40.8 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Jun | 35 | 32.1 | ||

| 14:00 | USD | Construction Spending M/M May | 1.00% | -2.90% | ||

| 14:30 | USD | Crude Oil Inventories | 1.4M | |||

| 18:00 | USD | FOMC Minutes |

{kind=link}