Risk sentiments continues to be weak today but selloff in the stock markets is so far limited. Euro rides on the indecisive markets and surges broadly today, with help by strong rally against Sterling. Swiss Franc is following as the second strongest so far. On the other hand, New Zealand Dollar is the worst performing one for today. Sterling is the second worst as weighed down by weaker than expected GDP rebound. Dollar is mixed, showing little reaction to stronger than expected CPI reading in June.

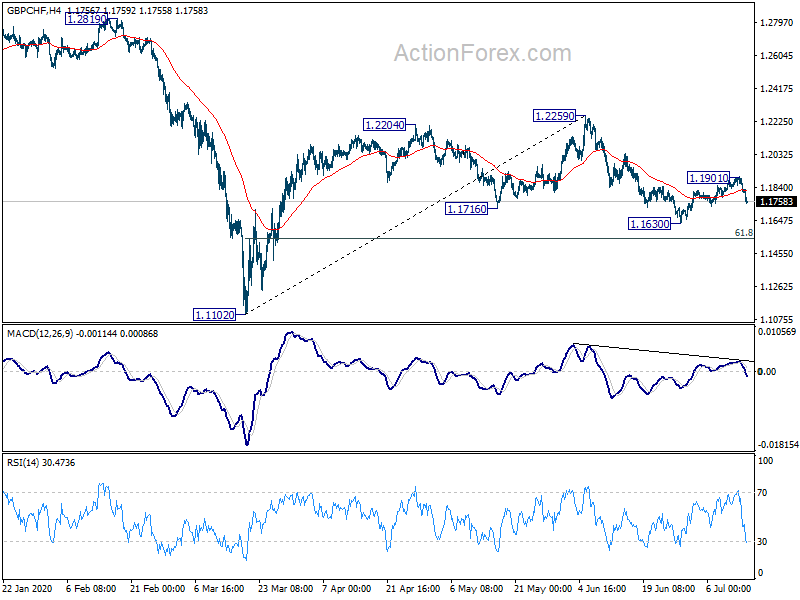

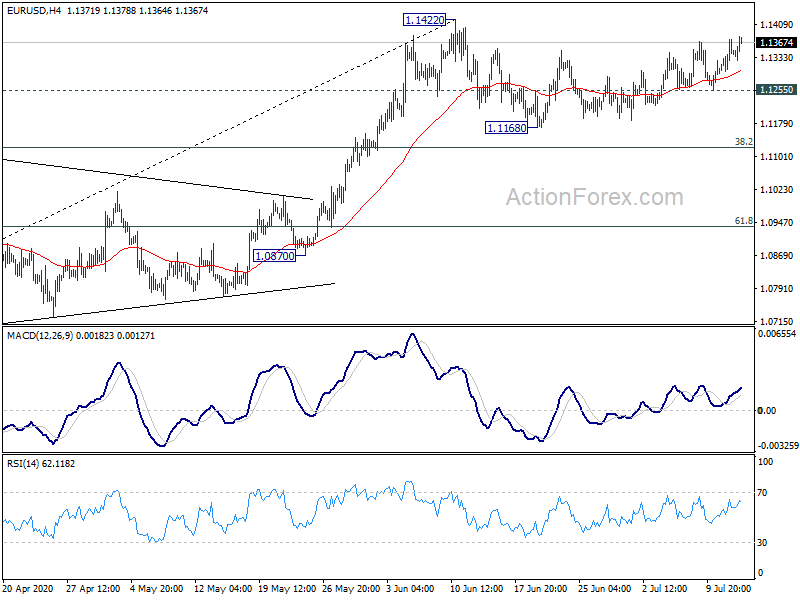

Technically, EUR/GBP’s break of 0.9067 resistance suggests completion of pull back from 0.9175. More importantly, rebound from 0.8670 is not over and it’s probably ready to resume. GBP/CHF’s recovery from 1.1630 has possibly completed at 1.1901 and focus is back on 1.130. Break will resume the decline from 1.2259 to 61.8% retracement of 1.1102 to 1.2259 at 1.1154. EUR/USD is on track to 1.1422 and above. But for now, we’re not seeing enough upside momentum to get through 1.1496 key resistance yet. Hence, we’ll look for sign of topping above 1.1422.

In Europe, currently, FTSE is down -0.63%. DAX is down -1.64%. CAC is down -1.83%. German 10-year yield is down -0.021 at -0.435. Earlier in Asia, Nikkei dropped -0.87%. Hong Kong HSI dropped -1.14%. China Shanghai SSE dropped -0.83%. Singapore Strait Times dropped -0.41%. Japan 10-year JGB yield dropped -0.0067 to 0.025.

US CPI picked up to 0.6% in June, core CPI unchanged at 1.2%

US CPI rose 0.6% mom in June, above expectation of 0.5% mom. Core CPI rose 0.2% mom, also above expectation of 0.1% mom. Annually, CPI accelerated back to 0.6% yoy, up from 0.1% yoy, above expectation of 0.3% yoy. Core CPI was unchanged at 1.2% yoy, above expectation of 1.1% yoy.

German ZEW dipped back to 59.3, gradual GDP growth expected in H2

Germany ZEW Economic Sentiment dropped to 59.3 in July, down from 63.4, missed expectation of 60.0. Current Situation index rose to -80.9, up form -83.1, missed expectation of -64.0. Eurozone ZEW Economic Sentiment rose to 59.6, up from 58.6, beat expectation of 55.8. Eurozone Current Situation rose 0.9 pts to -88.7.

“The outlook for the German economy largely remains unchanged compared to the previous month. After a very poor second quarter, the experts expect to see a gradual increase in gross domestic product in the second half of the year and in early 2021,” comments ZEW President Professor Achim Wambach.

Eurozone industrial production rose 12.4% mom in may, below expectations

Eurozone industrial production rose 12.4% mom in May, below expectation of 12.4% mom. That’s also insufficient to recovery April’s -18.2% mom decline. Looking at some details, production of durable consumer goods rose by 54.2% mom, capital goods by 25.4% mom, intermediate goods by 10.0% mom, non-durable consumer goods by 2.8% mom and energy by 2.3% mom.

EU industrial production rose 11.4% mom in May, versus April’s -18.2% mom decline. The highest increases were registered in Italy (+42.1%), France (+20.0%) and Slovakia (+19.6%). The largest decreases were observed in Ireland (-9.8%), Croatia (-3.5%) and Finland (-1.3%).

Also released, Germany CPI was finalized at 0.6% mom, 0.9% yoy in June. Swiss PPI came in at 0.5% mom, -3.5% yoy in June.

UK GDP grew just 1.8% mom in May, economy still a quarter below Feb level

UK GDP grew notably by 1.8% mom in May but the rebound was somewhat disappointing and missed expectation of 5.0% mom. Production jumped sharply by 6.0% mom, with manufacturing up 8.4%. Services rose 0.9% mom while construction rose 8.2% mom. But all were insufficient to recover the contraction in April (production -20.2% mom, manufacturing -24.4% mom, services -18.9% mom, construction -40.2% mom. Agriculture continued contraction by -6.2% mom.

For the three months to May, GDP dropped by -19.1% 3mo3m. Production dropped -15.5% 3mo3m. Manufacturing dropped -18.0% 3mo3m. Service dropped -18.9% 3mo3m. Construction dropped -29.8% 3mo3m. Agriculture dropped -6.3% 3mo3m.

Jonathan Athow, Deputy National Statistician for Economic Statistics, said: “Manufacturing and house building showed signs of recovery as some businesses saw staff return to work. Despite this, the economy was still a quarter smaller in May than in February, before the full effects of the pandemic struck. In the important services sector, we saw some pickup in retail, which saw record online sales. However, with lockdown restrictions remaining in place, many other services remained in the doldrums, with a number of areas seeing further declines.”

Also from UK, trade deficit narrowed to GBP -2.8B in May, better than expectation of GBP -8.2B. BRC retail sales monitor rose 10.9% yoy in June.

Australia NAB business confidence turned positive, turnaround faster than expected

Australia NAB Business Confidence rose to 1 in June, up from May’s -20, turned positive after rebounding sharply from the record lows over the past three months. Business Conditions also improved notably to -7, up from -24. Looking at some details, trading conditions rose to -7, up from -19. Profitability conditions rose from -8, up from -19. Employment conditions also rose to -11, up from -31.

Alan Oster, NAB Group Chief Economist, said: “Overall, there has been a very large and fast rebound in the business survey over the past two months, but keeping perspective over just how large the hit to both activity and confidence is very important. While the turnaround has possibly occurred faster than expected, things have certainly not fully recovered. Conditions and capacity utilisation remain very weak and will take some time to recover”.

China trade surplus narrowed to USD 46.4B in June as imports jumped more than exports

In June, in USD term, China’s total trade rose 1.5% yoy to USD 380.7B. Exports rose 0.5% yoy to USD 213.6B. Imports rose 2.7% yoy to USD 167.2B. Trade surplus narrowed to USD 46.4B, down from May’s USD 62.9B.

From January to June, total trade dropped -6.6% ytd yoy to USD 2029.7B. Exports dropped -6.2% ytd yoy to USD 1098.8B. Imports dropped -7.1% ytd yoy to USD 931.0B. Trade surplus came in at USD 167.8B year-to-June.

From January to June, with EU, total trade dropped -4.9% ytd yoy to USD 284.2B. Exports dropped -1.5% ytd yoy to USD 172.3B. Imports dropped -9.6% ytd yoy to USD 111.9B.

From January to June, with US, total trade dropped -9.7% ytd yoy to USD 234.0B. Exports dropped -11.1% ytd yoy to USD 177.6B. Imports dropped -4.8% ytd yoy to USD 56.4B.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1300; (P) 1.1338; (R1) 1.1379; More….

Intraday bias in EUR/USD remains mildly on the upside. Rebound from 1.1168 would target 1.1422 resistance first. Break will resume whole rebound from 1.0635 to 1.1496 key resistance. On the downside, however, break of 1.1255 minor support will turn bias back to the downside for 1.1168 support, and possibly further to 38.2% retracement of 1.0635 to 1.1422 at 1.1121.

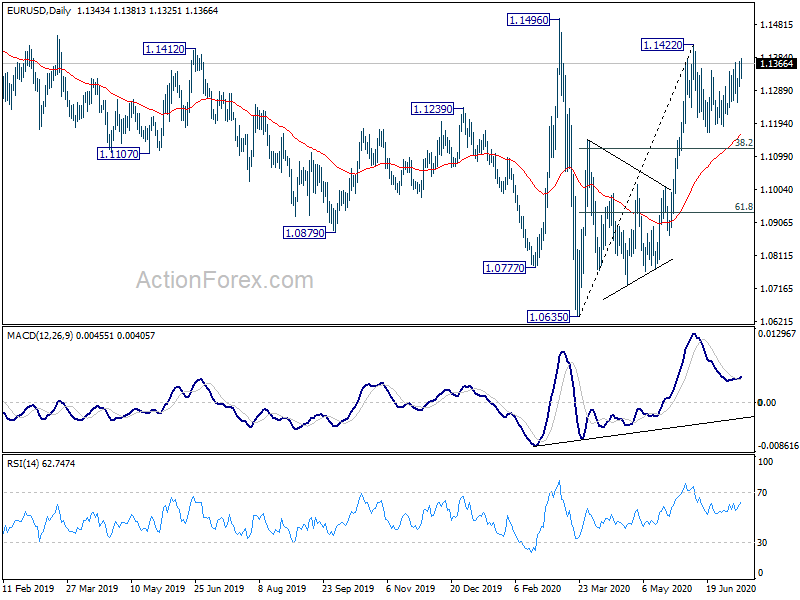

In the bigger picture, as long as 1.1496 resistance holds, whole down trend from 1.2555 (2018 high) should still be in progress. Next target is 1.0339 (2017 low). However, sustained break of 1.1496 will argue that such down trend has completed. Rise from 1.0635 could then be seen as the third leg of the pattern from 1.0339. In this case, outlook will be turned bullish for retesting 1.2555.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Retail Sales Monitor Y/Y Jun | 10.90% | 7.90% | ||

| 01:30 | AUD | NAB Business Conditions Jun | -7 | -24 | ||

| 01:30 | AUD | NAB Business Confidence Jun | 1 | -20 | ||

| 02:55 | CNY | Trade Balance (USD) Jun | 46.4B | 58.3B | 62.9B | |

| 02:55 | CNY | Exports (USD) Y/Y Jun | 0.50% | -3.30% | ||

| 02:55 | CNY | Imports (USD) Y/Y Jun | 2.70% | -16.70% | ||

| 02:55 | CNY | Trade Balance (CNY) Jun | 329B | 410B | 443B | |

| 02:55 | CNY | Exports (CNY) Y/Y Jun | 4.30% | 1.40% | ||

| 02:55 | CNY | Imports (CNY) Y/Y Jun | 6.20% | -12.70% | ||

| 04:30 | JPY | Industrial Production M/M May F | -8.90% | -8.40% | -8.40% | |

| 06:00 | GBP | GDP M/M May | 1.80% | 5.00% | -20.40% | -20.30% |

| 06:00 | GBP | Industrial Production M/M May | 6.00% | 6.00% | -20.30% | -20.20% |

| 06:00 | GBP | Industrial Production Y/Y May | -20.00% | -21.00% | -24.40% | -23.80% |

| 06:00 | GBP | Manufacturing Production M/M May | 8.40% | 8.00% | -24.30% | -24.40% |

| 06:00 | GBP | Manufacturing Production Y/Y May | -22.80% | -24.00% | -28.50% | -28.20% |

| 06:00 | GBP | Index of Services 3M/3M May | -18.90% | -16.90% | -9.90% | -10.70% |

| 06:00 | GBP | Goods Trade Balance (GBP) May | -2.8B | -8.2B | -7.5B | -4.8B |

| 06:00 | EUR | Germany CPI M/M Jun F | 0.60% | -0.10% | 0.60% | |

| 06:00 | EUR | Germany CPI Y/Y Jun F | 0.90% | 0.90% | 0.90% | |

| 06:30 | CHF | Producer and Import Prices M/M Jun | 0.50% | -0.90% | -0.50% | |

| 06:30 | CHF | Producer and Import Prices Y/Y Jun | -3.50% | -5.00% | -4.50% | |

| 09:00 | EUR | Eurozone Industrial Production M/M May | 12.40% | 13.40% | -17.10% | -18.20% |

| 09:00 | EUR | Germany ZEW Economic Sentiment Jul | 59.3 | 60 | 63.4 | |

| 09:00 | EUR | Germany ZEW Current Situation Jul | -80.9 | -64 | -83.1 | |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Jul | 59.6 | 55.8 | 58.6 | |

| 10:00 | USD | NFIB Business Optimism Index Jun | 100.6 | 90.9 | 94.4 | |

| 12:30 | USD | CPI M/M Jun | 0.60% | 0.50% | -0.10% | |

| 12:30 | USD | CPI Y/Y Jun | 0.60% | 0.30% | 0.10% | |

| 12:30 | USD | CPi Core M/M Jun | 0.20% | 0.10% | -0.10% | |

| 12:30 | USD | CPi Core Y/Y Jun | 1.20% | 1.10% | 1.20% |

{kind=link}