Investors in Asia remain generally cautious today as reflected in the mixed markets. US-China tensions look set to escalate further after President Donald Trump said closure of other Chinese missions is “always possible”. Yet, the developments give no special support to Dollar and Yen. Both remain the weakest for the week, and stay soft today. Australian Dollar is holding on to this week’s gains after the government said budget deficit is set to widen further in the current fiscal year. New Zealand Dollar is following as the second strongest.

Technically, there is prospect of a mild recovery in Dollar and Yen today. EUR/USD, AUD/USD and Gold are losing some upside momentum after hitting near term projection levels. EUR/JPY is also set to face 124.43 key resistance. Yet, even if recoveries occur, there wouldn’t be sign of bottoming until some near term levels are violated. The levels include 1.1402 support in EUR/USD, 0.6963 support in AUD/USD, 121.96 support in EUR/JPY and 1817.91 resistance turned support in Gold.

In Asia, Japan is on holiday today. Hong Kong HSI is up 0.45%. China Shanghai SSE is down -0.83%. Singapore Strait Times is up 0.95%. Overnight, DOW rose 0.62%. S&P 500 rose 0.57%. NASDAQ rose 0.24%. 10-year yield dropped -0.0012 to 0.595.

Australia budget deficit widened to 4.3% of GDP in fiscal 2020, sets to balloon further

Australia Treasurer Josh Frydenberg said the country’s budget balance had turned into a massive deficit of AUD 85.8B, or 4.3% of GDP, in the fiscal year ended June 2020. The deficit is expected to widen further to AUD 184.5B in fiscal 2020-21. Gross debt is projected to rise from AUD 684.3B in 2019-20 to AUD 851.9B in 2020-21.

He added that GDP could have falling by -7% in June quarter. GDP is expected to drop -0.25% in fiscal 2019-20 and -2.25% in fiscal 2020-21. Unemployment rate is expected to climb from 7.0% to 8.75% in 2020-21, and would probably hit 9.25% by Christmas this year.

S&P Global Ratings said Australia’s AAA credit rating could withstand the large widening in budget deficit as projected. The rating reflects the expectation that the economy will begin to recover from recessing during fiscal 2021. Nevertheless, “risks to our rating remain tilted toward the downside as the effects of the COVID-19 pandemic and government responses on the economy, budget, and financial markets evolve.”

Australia NAB business confidence dropped to -15 in Q2, forward looking conditions deteriorated

Australia NAB Quarterly Business Confidence dropped to -15 in Q2, down from Q1’s -12. Current Business Conditions dropped to -26, down from -3. That’s also the lowest reading since early 1990s. Conditions for next three months dropped to -22, down from -4. Conditions for the next 12 months dropped to -18, down form 7. Next 12 months capex plan also dropped to -8, down from 17.

South Korea GDP dropped -3.3% qoq in Q2, worst since 1998

South Korea’s GDP contracted -3.3% qoq in Q2, as shown in data released by Bank of Korea. The decline was the worst since Q1 1998, and steeper than analysts’ expectations of around -2.3% qoq. Also, with Q1’s -1.3% fall, South Korean’s economy has formally entered a technical recession this year, joining other major Asian countries like Japan and Singapore. Annually, GDP shrank -2.9% yoy in Q2.

“It’s possible for us to see China-style rebound in the third quarter as the pandemic slows and activity in overseas production, schools and hospitals resume,” South Korean finance minister finance minister Hong Nam-ki said after the data was released.

Looking ahead

Germany will release Gfk consumer confidence. UK will release industrial order expectations. Eurozone will also release consumer confidence. US will release jobless claims as usual on a Thursday.

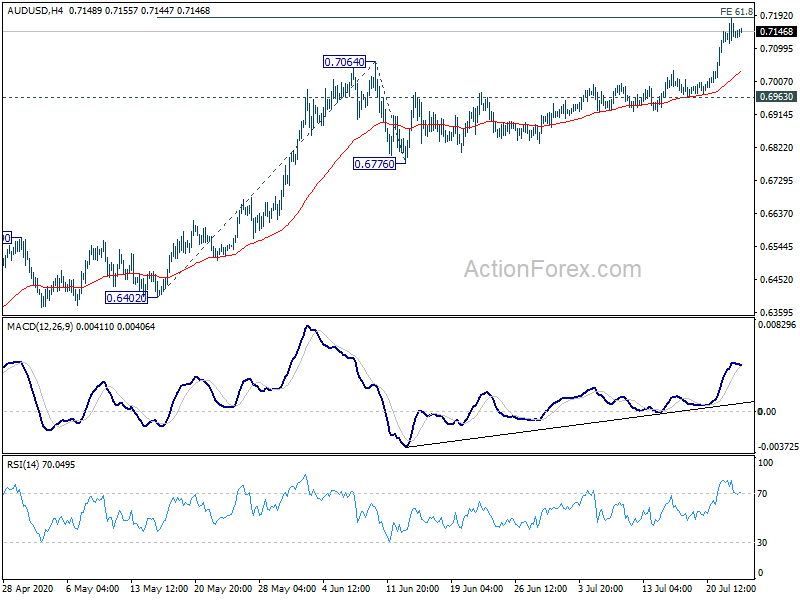

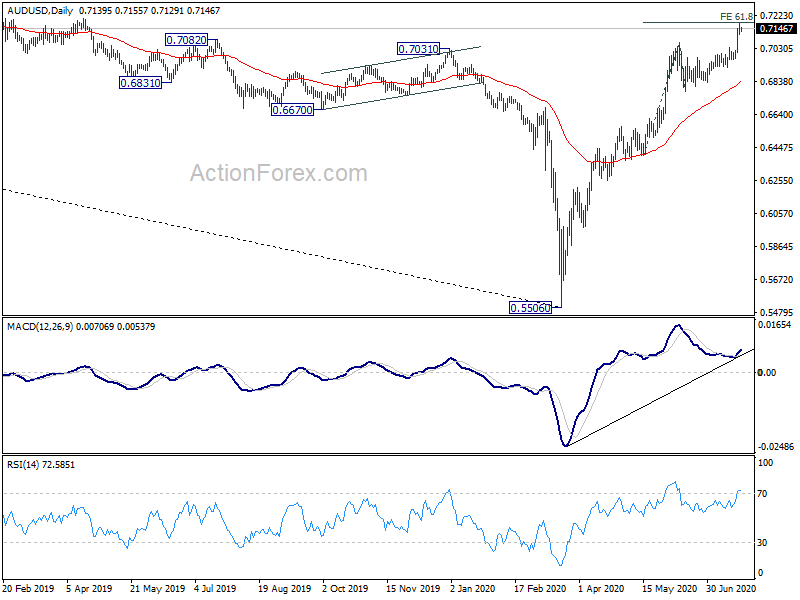

AUD/USD Daily Report

Daily Pivots: (S1) 0.7109; (P) 0.7146; (R1) 0.7178; More…

AUD/USD rises to as high as 0.7183 so far, just inch below 61.8% projection of 0.6402 to 0.7064 from 0.6776 at 0.7185. Intraday bias stays on the upside first. Sustained break of 0.7185 will target t long term EMA level at 0.7311 next. On the downside, break of 0.6963 support is needed to confirm short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, rebound from 0.5506 medium term bottom could be correcting whole long term down trend from 1.1079 (2011 high). Further rally would be seen to 55 month EMA (now at 0.7311). This will remain the preferred case as long as it stays above 55 week EMA (now at 0.6750). Sustained trading below 55 week EMA will turn focus back to 0.5506 low instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:30 | AUD | NAB Business Confidence Q2 | -15 | -11 | -12 | |

| 6:00 | EUR | Germany Gfk Consumer Confidence Aug | -4.5 | -9.6 | ||

| 10:00 | GBP | CBI Industrial Order Expectations Jul | -35 | -58 | ||

| 12:30 | USD | Initial Jobless Claims (Jul 17) | 1280K | 1300K | ||

| 14:00 | EUR | Eurozone Consumer Confidence Jul P | -12 | -15 | ||

| 14:30 | USD | Natural Gas Storage | 45B |

{kind=link}