Dollar is back under pressure as rebound attempt faltered quickly again. Nevertheless, New Zealand Dollar remains the worst one. Canadian Dollar is currently the strongest one in Asian session, lifted as crude oil rebounded quickly after a spike lower overnight. As for the week, Sterling and Yen are currently the strongest while Dollar and Kiwi are the weakest.

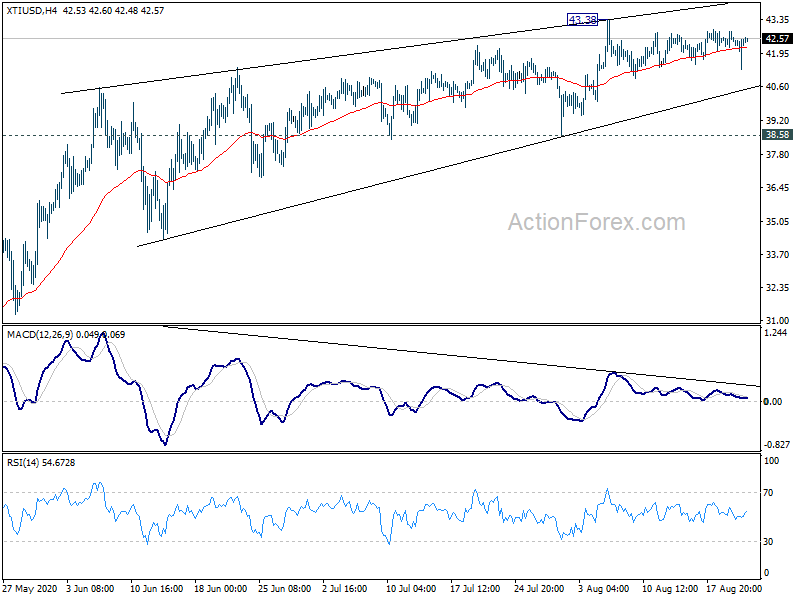

Technically, despite a rather steep spike overnight, WTI crude oil is quickly back above 4 hour 55 EMA. It’s also held well above near term trend line support. Thus, further rally is in favor through 43.38 sooner or later. Yet, upside momentum is weak considering persistent bearish divergence condition in 4 hour MACD. Upside potential could be limited even in case of a breakout. Translating into USD/CAD, the pair might get some strong support from 1.3056 long term fibonacci level, at least on first attempt.

In Asia, currently, Nikkei is up 0.32%. Hong Kong HSI is up 1.14%. China Shanghai SSE is up 0.82%. Singapore Strait Times is up 0.67%. Japan 10-year JGB yield is up 0.0004 at 0.030. Overnight, DOW rose 0.17%. S&P 500 rose 0.32%. NASDAQ rose 1.06% to 11264.95, new record. 10-year yield dropped -0.031 to 0.644.

Japan PMI composite unchanged at 44.9, prospect of a solid recovery remains highly uncertain

Japan PMI Manufacturing rose to 46.6 in August, up from 45.2, above expectation of 45.0. PMI Services edged down to 45.0, down from 45.4. PMI Composite was unchanged at 44.9.

Bernard Aw, Principal Economist at IHS Markit, said: “The prospect of a solid recovery remains highly uncertain as Japanese firms were pessimistic about the business outlook on balance during August. Rising unemployment may also hit domestic household income and spending in the months ahead.”

Japan core CPI unchanged at 0% in July

Japan all item inflation rose to 0.3% yoy in July, up from 0.1%. Core CPI, all item ex fresh food, was unchanged at 0.0% yoy, below expectation of 0.1% yoy. Core-core CPI, all item ex fresh food and energy was unchanged at 0.4% yoy.

Outlook for core inflation suggests that Japan is close to, if not already in, a deflationary situation. It’s becoming increasingly unrealistic to achieve BoJ’s 2% inflation target in any projection horizon.

Australia CBA PMI composite tumbled to 48.8, back in contraction

Australia CBA PMI Manufacturing dropped slightly to 53.9 in August, down from 54.0. However, PMI Services sharply sharply by more than -10 pts to 48.1, down from 58.2, back in contraction. PMI Composite also tumbled to 48.8, down from 57.8, back in contraction too.

CBA Head of Australian Economics, Gareth Aird said: “The decline in business activity over August is hardly surprising given the lockdown measures in Victoria. With the August composite flash PMI only modestly in contractionary territory it is highly likely that outside of Victoria private output continued to expand over the month”.

“The fall in employment is the inevitable consequence of shutting down large parts of the Victorian economy. Encouragingly, firms collectively retain an optimistic view on the outlook despite the setback in Victoria. Ongoing fiscal support for households and businesses remains critical to ensuring that optimism is not misplaced”.

Australia retails grew in July, except in Victoria

July’s preliminary reading showed retail sales grew 3.3% mom in Australia. Sales rose in all states and territories except Victoria, coinciding with the resurgence of coronavirus cases and reintroduction of stage 3 restrictions.

“The rise across the rest of the country was driven by continued strength in household goods retailing, and the recovery in cafes, restaurants and takeaway food services, and clothing, footwear and personal accessory retailing” said Ben James, Director of Quarterly Economy Wide Surveys.

UK Gfk consumer confidence unchanged at -27

UK Gfk Consumer Confidence was unchanged at -27 in August, worse than expectation of -25. General economic situation over the last 12 months dropped -1 pts to -62. General economic situation over the next 12 months also dropped -1 pts to -42.

Joe Staton, GfK’s Client Strategy Director, says: “Employment is now the big issue because the pandemic has ended years of job security. Yes, discounted dinners have proved a winner with hungry consumers across the country this month, but it’s difficult to see significantly increased appetite for other types of spending for now.”

Looking ahead

PMIs will be the main focuses for today and will be released from Eurozone, UK, and US. UK will also release retail sales and public sector borrowing. Canada will release new housing price index and retail sales. US will release existing home sales.

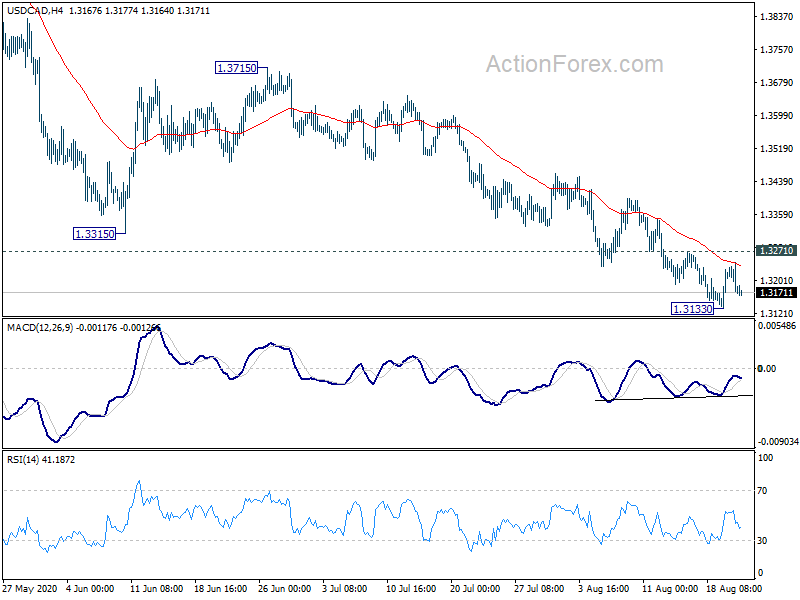

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3152; (P) 1.3199; (R1) 1.3228; More….

Intraday bias in USD/CAD stays neutral for consolidations above 1.3133 temporary low. Outlook stays bearish with 1.3271 resistance intact. Break of 1.3133 will resume the fall from 1.4667 to long term fibonacci level at 1.3056. Nevertheless, considering bullish convergence condition, firm break of 1.3271 should confirm short term bottoming. Intraday bias will be turned back to the upside for rebound to 55 day EMA (now at 1.3448).

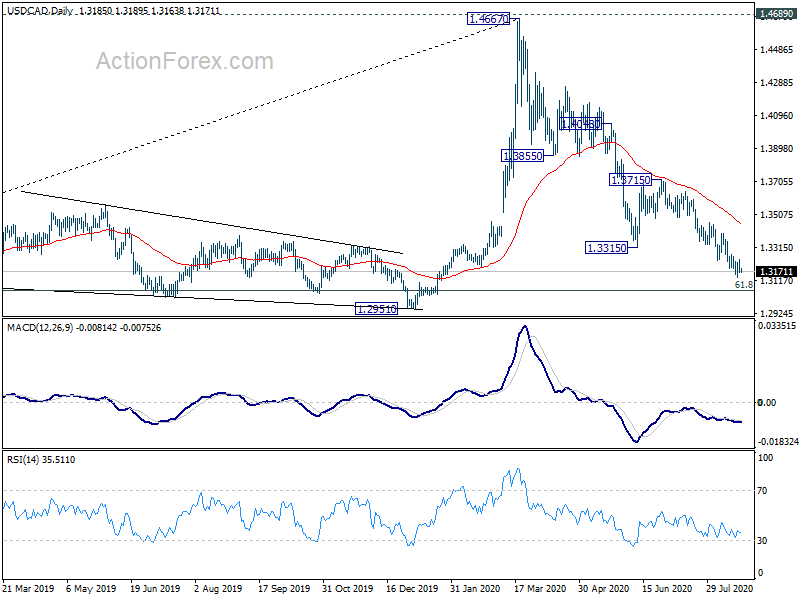

In the bigger picture, the rise from 1.2061 (2017 low) could have completed at 1.4667 after failing 1.4689 (2016 high). Fall from 1.4667 could be the third leg of the corrective pattern from 1.4689. Deeper fall is expected to 61.8% retracement of 1.2061 to 1.4667 at 1.3056 and possibly below. This will now remain the favored case as long as 1.3715 resistance holds. However, sustained break of 1.3715 will turn focus back to 1.4689 key resistance.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:00 | AUD | CBA Manufacturing PMI Aug P | 53.9 | 54.0 | ||

| 23:00 | AUD | CBA Services PMI Aug P | 48.1 | 58.2 | ||

| 23:01 | GBP | GfK Consumer Confidence Aug | -27 | -25 | -27 | |

| 23:30 | JPY | National CPI Core Y/Y Jul | 0.00% | 0.10% | 0.00% | |

| 00:30 | JPY | Manufacturing PMI Aug P | 46.6 | 45.0 | 45.2 | |

| 06:00 | GBP | Retail Sales M/M Jul | 2.00% | 13.90% | ||

| 06:00 | GBP | Retail Sales Y/Y Jul | 0.00% | -1.60% | ||

| 06:00 | GBP | Retail Sales ex-Fuel M/M Jul | 0.20% | 13.50% | ||

| 06:00 | GBP | Retail Sales ex-Fuel Y/Y Jul | 1.50% | 1.70% | ||

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Jul | 28.3B | 34.8B | ||

| 07:15 | EUR | France Manufacturing PMI Aug P | 53 | 52.4 | ||

| 07:15 | EUR | France Services PMI Aug P | 56.3 | 57.3 | ||

| 07:30 | EUR | Germany Manufacturing PMI Aug P | 52.5 | 51 | ||

| 07:30 | EUR | Germany Services PMI Aug P | 55.6 | 55.6 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Aug P | 53 | 51.8 | ||

| 08:00 | EUR | Eurozone Services PMI Aug P | 54 | 54.7 | ||

| 08:30 | GBP | Manufacturing PMI Aug P | 53.6 | 53.3 | ||

| 08:30 | GBP | Services PMI Aug P | 57 | 56.5 | ||

| 12:30 | CAD | New Housing Price Index M/M Jul | 0.10% | 0.10% | ||

| 12:30 | CAD | Retail Sales M/M Jun | 18.70% | |||

| 12:30 | CAD | Retail Sales ex Autos M/M Jun | 10.60% | |||

| 13:45 | USD | Manufacturing PMI Aug P | 51.5 | 50.9 | ||

| 13:45 | USD | Services PMI Aug P | 50.7 | 50 | ||

| 14:00 | USD | Existing Home Sales Jul | 5.10M | 4.72M | ||

| 14:00 | EUR | Eurozone Consumer Confidence Aug P | -15 | -15 |

{kind=link}