Sterling drops broadly today as BoE minutes indicated that the central bank is already discussing implementation negative interest rates. On the other hand, Yen is currently the strongest one, extending this week’s strong rally. Risk aversion and falling treasury yields are both helping the Yen higher. Dollar lost some momentum after initial post-FOMC rise, but remains the second strongest for the day. Overall risk sentiments would now be the main driver in the markets, probably till weekly close.

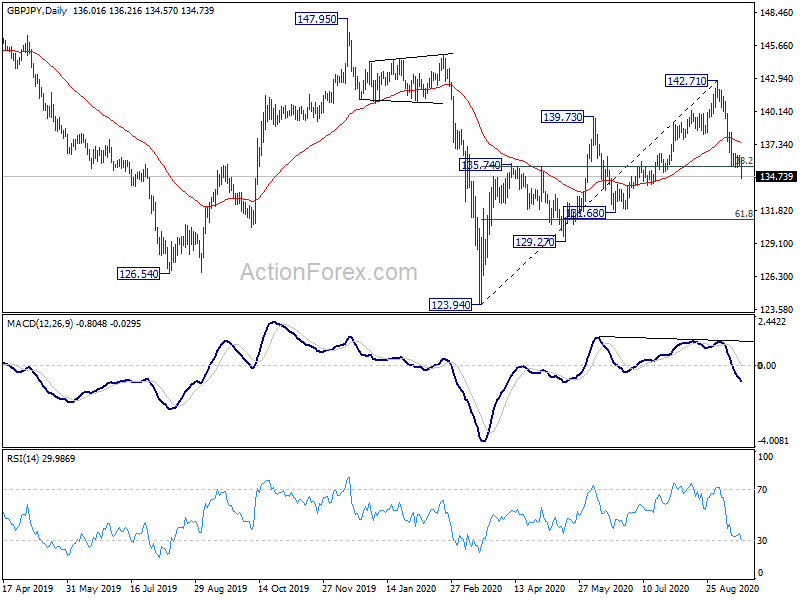

Technically, GBP/JPY finally breaks 135.53 fibonacci support firmly. The development now raises the chance that whole rebound form 123.94 has completed at 142.71. The corrective structure in turn argue that larger down trend is still in progress. Focus is now on 61.8% retracement at 131.11 next.

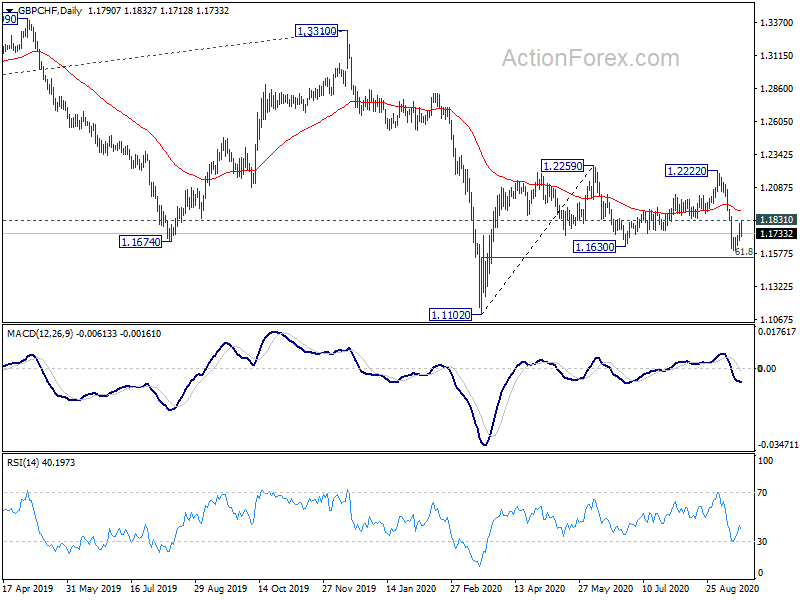

GBP/CHF was rejected by 1.1831 minor resistance. Break of 11598 temporary should pave the wave to retest 1.1102 low. The development could also affirm medium term bearishness for down trend resumption.

In Europe, currently, FTSE is down -0.37%. DAX is down -0.81%. CAC is down -0.96%. Germany 10-year yield is down -0.024 at -0.504. Earlier in Asia, Nikkei dropped -0.67%. Hong Kong HSI dropped -1.56%. China Shanghai SSE dropped -0.41%. Singapore Strait Times dropped -0.17%. Japan 10-year JGB yield dropped -0.0065 to 0.014.

US initial jobless claims dropped to 860k, continuing claims down to 12.6m

US initial jobless claims dropped -33k to 860k in the week ending September 12, above expectation of 825k. Four-week moving average of initial claims dropped -61k to 912k. Continuing claims dropped -916k to 12628k in the week ending September 5. Four-week moving average of continuing claims dropped -533k to 13489k.

Also released, Philadelphia Fed manufacturing index dropped to 15.0 in September, down form 17.2, above expectation of 14.5. Housing starts dropped to 1.42m annualized rate in August while building permits dropped to 1.47m.

BoE kept policy unchanged, MPC briefed on plans to explore negative rates

BoE kept Bank Rate unchanged at 0.1% as widely expected. The target of asset purchases was also held at GBP 745B. Both decisions were made by unanimous votes. The central bank pledged to continue to “monitor the situation closely and stands ready to adjust monetary policy accordingly to meet its remit”. It “does not intend to tighten monetary policy until there is clear evidence that significant progress is being made in eliminating spare capacity and achieving the 2% inflation target sustainably.”

The central bank also noted that “recent domestic economic data have been a little stronger than the Committee expected” at the time of the August Monetary Policy Report. However, “it is unclear how informative they are about how the economy will perform further out.” Recent increases in coronavirus cases is some parts of the world “have the potential to weigh further on economic activity”. Meanwhile, “there remains a risk of more persistent period of elevated unemployment”.

In the minutes, it’s noted that the Committee “had discussed its policy toolkit, and the effectiveness of negative policy rates”. The MPC had been briefed on the plans to explore how a negative Bank Rate could be implemented effectively, should the outlook for inflation and output warrant it at some point during this period of low equilibrium rates.”

Eurozone CPI finalized at -0.2% in Aug, EU CPI at 0.4%

Eurozone CPI is finalized at -0.2% yoy in August, down from July’s 0.4% yoy. The highest contribution to the annual euro area inflation rate came from food, alcohol & tobacco (+0.33 percentage points, pp), followed by services (+0.30 pp), non-energy industrial goods (-0.03 pp) and energy (-0.77 pp).

EU CPI was finalized at 0.4% yoy, up from July’s 0.9% yoy. The lowest annual rates were registered in Cyprus (-2.9%), Greece (-2.3%) and Estonia (-1.3%). The highest annual rates were recorded in Hungary (4.0%), Poland (3.7%) and Czechia (3.5%). Compared with July, annual inflation fell in sixteen Member States, remained stable in five and rose in six.

BoJ Kuroda: Given the pandemic, inflation is falling quite a lot in many countries

BoJ left monetary policy unchanged as widely expected. Under the yield curve control framework, short term interest rate is kept at -0.1%. BoJ will also continue to purchase JGBs, without upper limit, to keep 10-year JGB yield at around 0%. The decision was made by 8-1 vote as usual, with Goushi Kataoka dissented, pushing to strengthen monetary easing.

In the post meeting press conference, Governor Haruhiko Kuroda said “domestic and overseas markets remain jittery but tensions have eased somewhat.” He pledged that “the BOJ will continue with measures that are exerting positive effects in the economy”.

“There is absolutely no need to change our 2% inflation target,” he said. “Given the pandemic, inflation is falling quite a lot in many countries. Prices may start falling in Japan as well. But that doesn’t mean Japan and western countries are discussing the need to change their inflation targets.”

On exchange rate, Kuroda reiterated that “currency rates should move in a way that reflects economic fundamentals.” He maintained the stance of “watching currency moves carefully from that perspective.”

Australia employment grew 111k in Aug, unemployment rate dropped to 6.8%

Australia employment grew strongly by 111k to 12.6m in August, much better than expectation of -40k contraction. Full-time jobs rose 36.2k to 8.58m. Part-time jobs rose 74.8k to 4.00m. Unemployment rate dropped notably by 0.7 pts to 6.8%, much better than expectation of 7.8%. Participation rate also rose 0.1% to 64.8%. Monthly hours worked in all jobs also rose 1.6m hours to 1683 hours.

All states and territories recorded increases in the number of employed people except for Victoria. The number of employed people in Victoria decreased by 42,400. In contrast, New South Wales recorded an increase of 51,500 employed people and there was an increase of 32,200 employed people in Western Australia. Unemployment rates decreased in most states and territories. The largest falls were seen in Northern Territory (down 3.3 pts to 4.2%). Increases were recorded in Victoria (up 0.4 pts to 7.1%) and Tasmania (up 0.3 pts to 6.3%).

New Zealand GDP contracted record -12.2% in Q2, NZD/JPY turning lower

New Zealand GDP contracted -12.2% qoq in Q2, the largest decline on record. But that’s slightly better than expectation of -12.5% qoq. Services industries, which contributed to 2/3 of the economy, dropped -10.9% qoq. Goods-producing industries, at about 1/5 of the economy, dropped -16.3% qoq. Primary industries dropped -8.7% qoq. Annual GDP in the year to June 2020 declined by -2.0%.

NZD/JPY trades lower today after failing to sustain above 4 hour 55 EMA. Focus is now back on 69.89 support. Break there will firstly resume the decline from 71.97. Secondly, that will add to the case that whole rise form 59.49 has completed with five waves up to 71.97. A deeper correction would then be underway to 68.75 support and probably further to 38.2% retracement at 67.20.

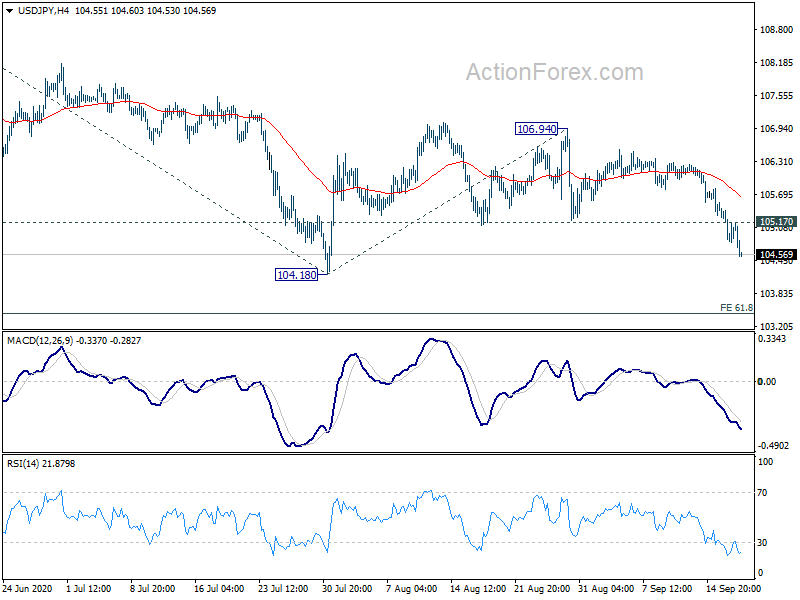

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 104.71; (P) 105.07; (R1) 105.35; More...

USD/JPY drops to as low as 104.52 so far and intraday bias on the downside for retesting 104.18 first. Break there will resume larger fall from 111.71 and target 61.8% projection of 109.85 to 104.18 from 106.94 at 103.43 next. On the upside, above 105.17 minor resistance will dampen this bearish view and turn intraday bias neutral again first.

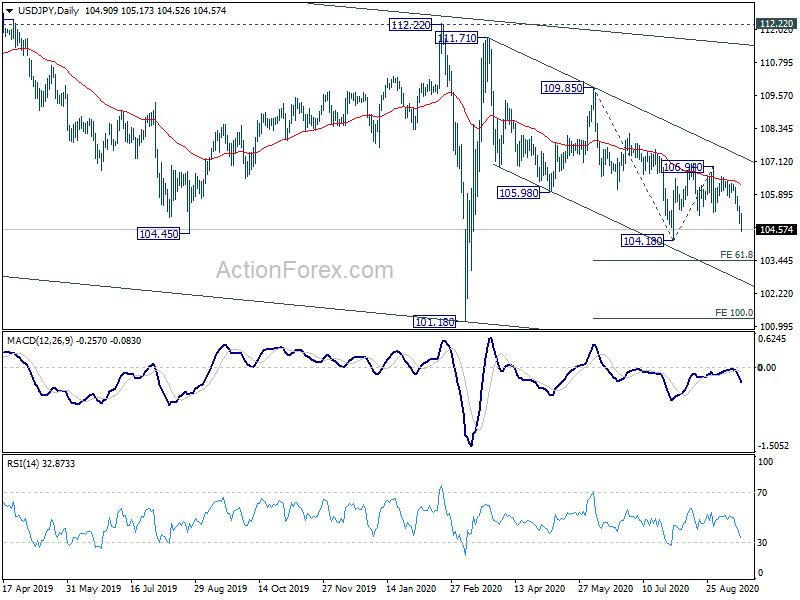

In the bigger picture, USD/JPY is still staying in long term falling channel that started back in 118.65 (Dec. 2016). Hence, there is no clear indication of trend reversal yet. The down trend could still extend through 101.18 low. However, sustained break of 112.22 should confirm completion of the down trend and turn outlook bullish for 118.65 and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | GDP Q/Q Q2 | -12.20% | -12.50% | -1.60% | -1.40% |

| 01:30 | AUD | Employment Change Aug | 111.0K | -40.0K | 114.7K | 119.2K |

| 01:30 | AUD | Unemployment Rate Aug | 6.80% | 7.80% | 7.50% | |

| 01:30 | AUD | RBA Bulletin | ||||

| 03:00 | JPY | BoJ Interest Rate Decision | -0.10% | -0.10% | -0.10% | |

| 03:00 | JPY | BoJ Monetary Policy Statement | ||||

| 06:00 | CHF | Trade Balance (CHF) Aug | 3.58B | 3.20B | 3.38B | 3.34B |

| 08:00 | EUR | Italy Trade Balance (EUR) Jul | 9.69B | 5.20B | 6.23B | |

| 09:00 | EUR | Eurozone CPI Y/Y Aug F | -0.20% | -0.20% | -0.20% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Aug F | 0.40% | 0.40% | 0.40% | |

| 11:00 | GBP | BoE Interest Rate Decision | 0.10% | 0.10% | 0.10% | |

| 11:00 | GBP | BoE Asset Purchase Facility Sep | 745B | 745B | 745B | |

| 11:00 | GBP | MPC Official Bank Rate Votes | 0–0–9 | 0–0–9 | 0–0–9 | |

| 11:00 | GBP | MPC Asset Purchase Facility Votes | 0–0–9 | 0–0–9 | 0–0–9 | |

| 12:30 | CAD | ADP Employment Change Aug | -205.4K | 1149.8K | -523.0K | |

| 12:30 | USD | Initial Jobless Claims (Sep 11) | 860K | 825K | 884K | 893K |

| 12:30 | USD | Housing Starts Aug | 1.42M | 1.47M | 1.50M | 1.49M |

| 12:30 | USD | Building Permits Aug | 1.47M | 1.51M | 1.50M | 1.48M |

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Sep | 15 | 14.5 | 17.2 | |

| 14:30 | USD | Natural Gas Storage | 76B | 70B |

{kind=link}