Commodity currencies tumble generally in Asian session today. New Zealand Dollar softens as RBNZ further affirm that it’s in progress for more monetary easing, including negative interest rates. Aussie also tumble on increasing expectation of on imminent RBA rate cut in October. On the other hand, while US stocks closed higher overnight, recovery was not strong enough to warrant completion of the correction. That is, risks in stocks remain on the downside for now. The overall sentiments are supporting Dollar and Yen in general.

Technically, Dollar is finally making progress in confirming it’s momentum for a sustainable near term rebound. EUR/USD broke 1.1737 support firmly. GBP/USD breached 1.2762 support. AUD/USD also breached 0.7135 support. USD/CHF broke 0.9200 resistance. More upside is likely in the greenback for the near term.

In Asia, currently, Nikkei is down -0.47%. Hong Kong HSI is up 0.01%. China Shanghai SSE is up 0.07%. Singapore Strait Times is down -0.01%. Japan 10-year JGB yield is down -0.0069 at 0.008. We’ll see if it’s heading back to negative. Overnight, DOW rose 0.52%. S&P 500 rose 1.05%. NASDAQ rose 1.71%. 10-year yield dropped -0.007 to 0.664.

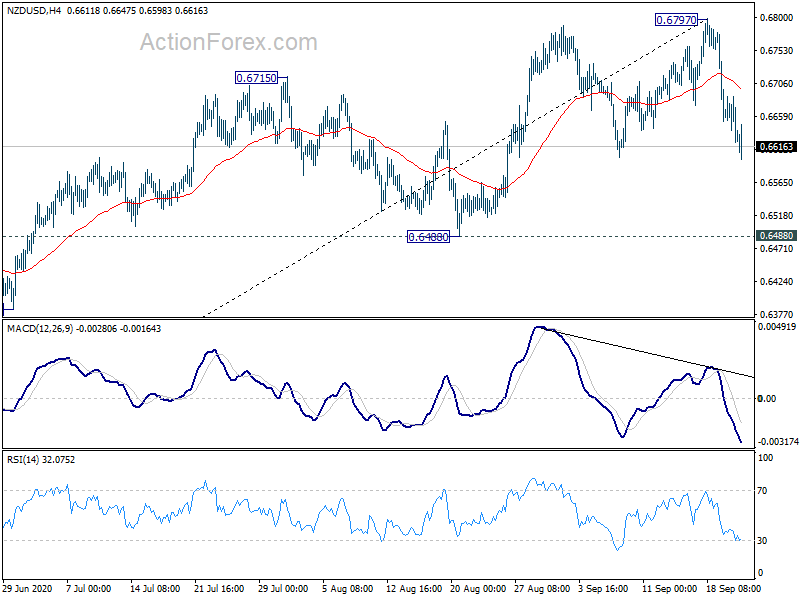

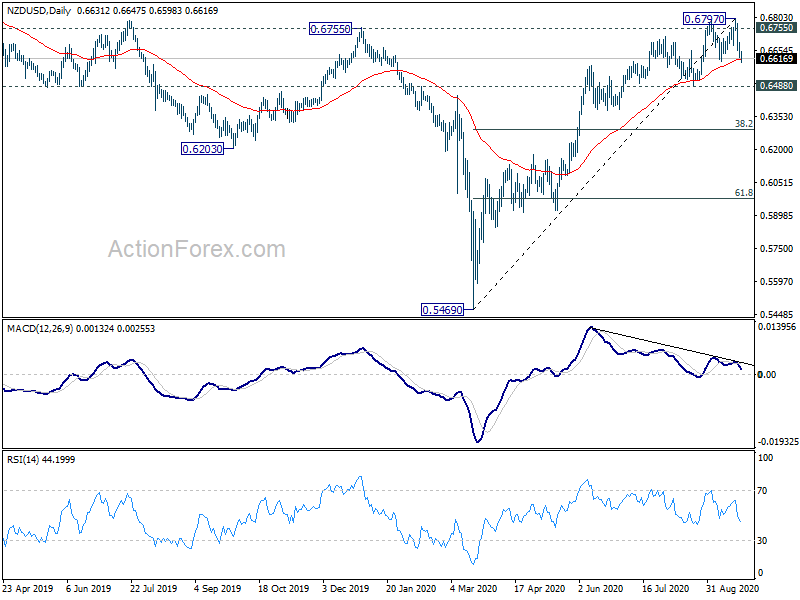

RBNZ holds OCR at 0.25% and prepares for more stimulus, NZD/USD fall continues

RBNZ held OCR unchanged at 0.25% as widely expected. The Large Scale Asset Purchase program is also kept at a maximum of NZD 100B by June 2022. The action is “necessary to further lower household and business borrowing rates in order to achieve the Committee’s inflation and employment remit.”

RBNZ also made progress on deploying additional monetary instruments, including “a Funding for Lending Programme (FLP), a negative OCR, and purchases of foreign assets.” It noted that “a package of an FLP and a lower or negative OCR could provide an effective way to deliver additional monetary stimulus.”

On the economy, RBNZ expects “a rise in unemployment and an increase in firm closures, as resource reallocation continues”. Significant monetary policy support is needed “for a long time”. In the minutes, it also noted that “further monetary stimulus may be needed” to help achieve its remit objectives and promote financial stability.

Some volatility is seen in NZD/USD after the release but it’s, after all, still extending the fall from 0.6797. Further decline is expected for 0.6488 support. The case of topping at 0.6797 is building up, with bearish divergence condition in daily MACD, and repeated failure to sustain above 0.6755 resistance. Firm break of 0.6488 will confirm that it’s at least correcting the rise from 0.5469 and should target 38.2% retracement at 0.6290.

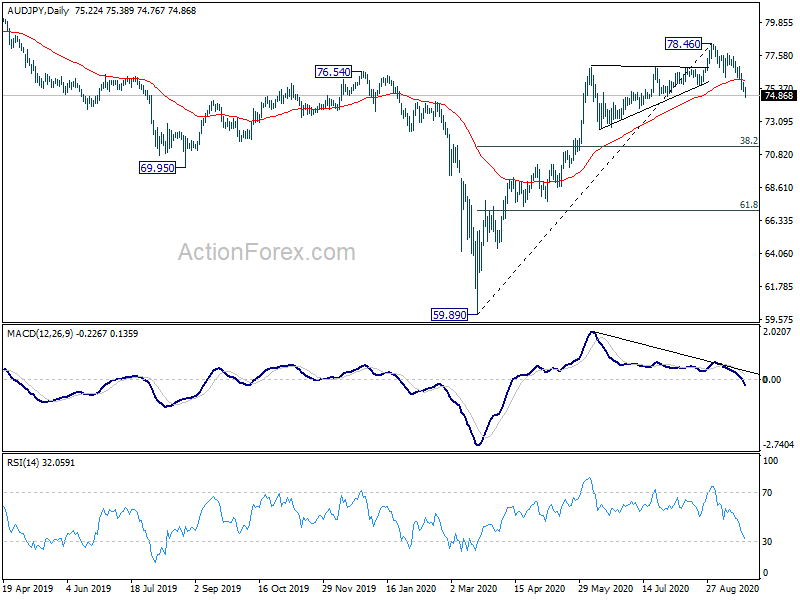

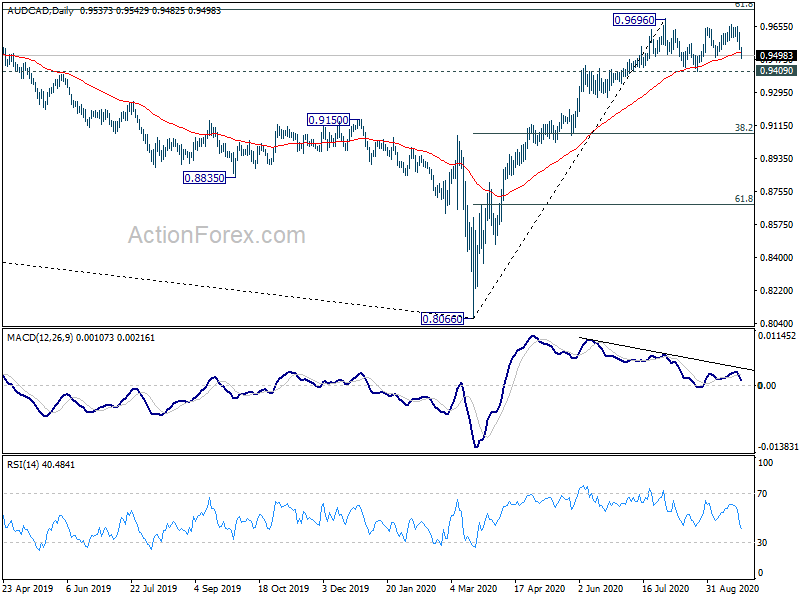

AUD/JPY and AUD/CAD tumble on speculation of Team Australia RBA rate cut

Australian Dollar weakens broadly today, on growing speculation of imminent easing after RBA Deputy Governor Guy Debelle’s speech yesterday. Westpac expects the measures to be announced on October 6, the same day as the government delivers budget, as a “Team Australia” move. RBA is expected to cut overnight cash rate down from 0.25% to 0.10%. Three year yield target will be lowered from 25% to 10% too. Additionally, RBA would expand asset purchases to government and semi government securities in maturities between 5 and 10 years.

AUD/JPY’s fall from 78.46 extends to as low as 74.76 so far today. The clean break of 55 day EMA affirms that tis’ now correcting whole rise form 59.89. AUD/JPY should be targeting 38.2% retracement at 7136.

AUD/CAD is also worth a watch as the Aussie has been outperforming other commodity currencies for the past few months. Break of 0.9409 support should confirm that it’s, at least, starting a correction to whole rise form 0.8066 to 0.9696. Deeper decline would be seen back to 38.2% retracement at 0.9073. That, if happens, would mark the near term U-turn in Aussie’s general fortune.

Australia PMI composite rose to 50.5 in Sep, retail sales dropped -4.2% mom in Aug

Australia PMI Manufacturing rose to 55.5 in September, up from 53.6, hitting a 29-month high. PMI Services also improved slightly to 50.0, up from 49.0. PMI Composite rose to 50.5, up from 49.4, back in expansion.

Bernard Aw, Principal Economist at IHS Markit, said: “The latest PMI data showed signs of stabilisation in Australia’s private sector business conditions during September, with activity and sales increasing marginally after falling in August amid tightening containment measures to contain a surge in new infection cases. However, other survey indicators suggest that the rebound may lack legs going forward. The absence of capacity pressure led to a further and sharper decline in workforce numbers, highlighting the prospect of rising unemployment.”

Retail sales dropped -4.2% mom, or AUD -1.28B, in August. Over the year, though, sales was up 6.9% yoy comparing with August 2019. Sales dropped sharply by -12.6 mom in Victoria, due to stage-4 restriction sin Melbourne. Excluding Victoria, sales in the rest of Australia dropped -1.5% mom.

Japan PMI composite edged up to 45.5, setting the scene for more Q3 weakness

Japan PMI Manufacturing edged up to 47.3 in September, from August’s 47.2. PMI Services also rose to 45.6, up from 45.0. PMI Composite rose to 45.5, up from 45.2.

Bernard Aw, Principal Economist at IHS Markit, said: “Flash PMI survey data indicated a further decline in Japanese private sector output during September, setting the scene for further economic weakness in the third quarter… That said, the picture of the economy remained much improved when compared to the height of the pandemic during the second quarter.

“The survey also revealed some positive signs. Firstly, employment moved closer to stabilisation, with only a marginal drop in workforce numbers that was the weakest in the current sequence of job shedding. Secondly, business sentiment improved to the strongest since the start of the year, with manufacturing firms particularly optimistic about the year-ahead outlook.”

Looking ahead

PMIs from Eurozone and UK will be the major focuses in European session. Germany will also release Gfk consumer sentiment. Later in the day, US will release house price index, as well as PMIs.

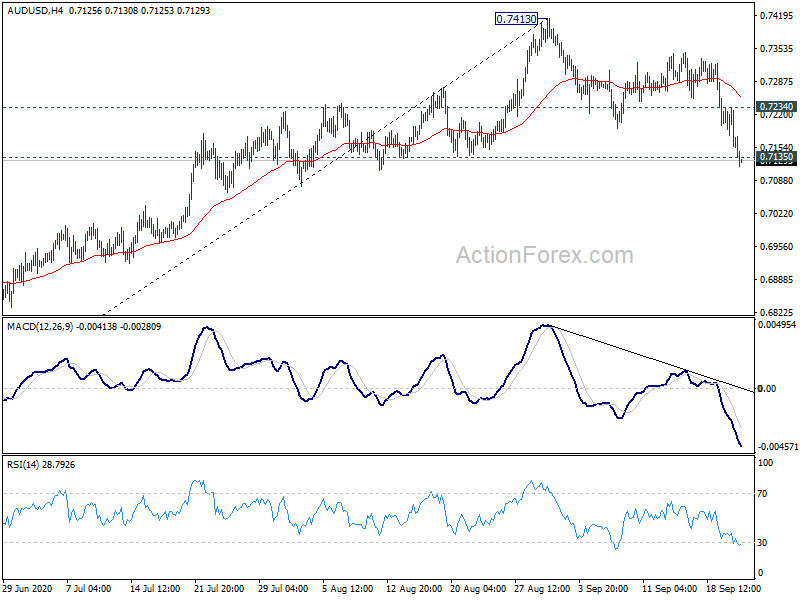

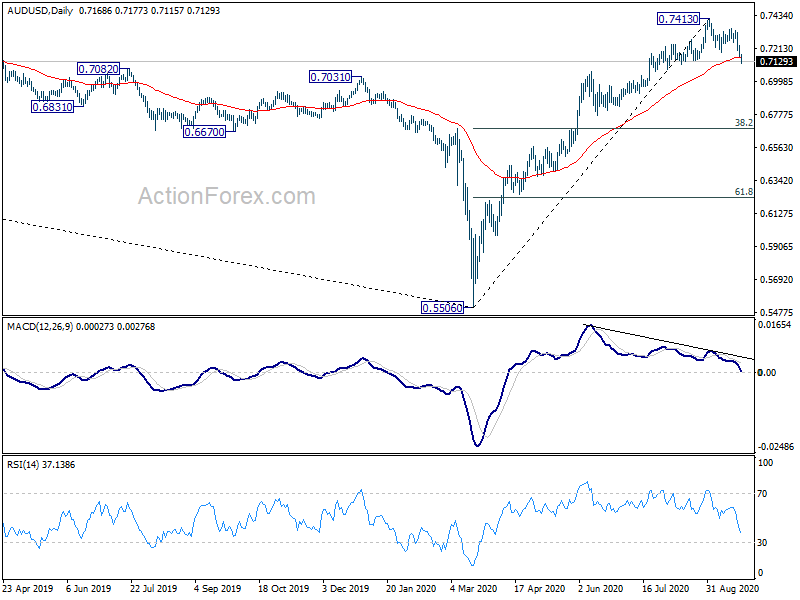

AUD/USD Daily Report

Daily Pivots: (S1) 0.7138; (P) 0.7186; (R1) 0.7218; More…

AUD/USD’s break of 0.7135 support now suggests that it’s correcting the whole rise from 0.5506. Intraday bias is back on the downside as fall from 0.7413 would target o 38.2% retracement of 0.5506 to 0.7413 at 0.6685. On the upside, break of 0.7234 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 0.7413 resistance holds, in case of rebound.

In the bigger picture, rebound from 0.5506 medium term bottom is seen as correcting whole long term down trend from 1.1079 (2011 high). Further rise could be seen to 38.2% retracement of 1.1079 (2011 high) to 0.5506 (2020 low) at 0.7635 next. On the downside, break of 0.6776 support is needed to be the first sign of completion of the rebound. Otherwise, outlook will stay bullish in case of pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:00 | AUD | CBA Manufacturing PMI Sep P | 55.5 | 53.6 | ||

| 23:00 | AUD | CBA Services PMI Sep P | 50 | 49 | ||

| 0:30 | JPY | Manufacturing PMI Sep P | 47.3 | 47.3 | 47.2 | |

| 2:00 | NZD | RBNZ Rate Decision | 0.25% | 0.25% | 0.25% | |

| 4:30 | JPY | All Industry Activity Index M/M Jul | 1.3% | 1.30% | 6.10% | 6.8% |

| 6:00 | EUR | Germany Gfk Consumer Confidence Oct | -1 | -1.8 | ||

| 7:15 | EUR | France Manufacturing PMI Sep P | 50.6 | 49.8 | ||

| 7:15 | EUR | France Services PMI Sep P | 51.7 | 51.5 | ||

| 7:30 | EUR | Germany Manufacturing PMI Sep P | 52.5 | 52.2 | ||

| 7:30 | EUR | Germany Services PMI Sep P | 53 | 52.5 | ||

| 8:00 | EUR | Eurozone Manufacturing PMI Sep P | 51.9 | 51.7 | ||

| 8:00 | EUR | Eurozone Services PMI Sep P | 50.5 | 50.5 | ||

| 8:30 | GBP | Manufacturing PMI Sep P | 54 | 55.2 | ||

| 8:30 | GBP | Services PMI Sep P | 56 | 58.8 | ||

| 13:00 | USD | Housing Price Index M/M Jul | 0.50% | 0.90% | ||

| 13:45 | USD | Manufacturing PMI Sep P | 53.1 | 53.1 | ||

| 13:45 | USD | Services PMI Sep P | 54.7 | 55 | ||

| 14:00 | USD | Fed’s Chair Powell testifies | ||||

| 14:00 | USD | Crude Oil Inventories |

{kind=link}