Risk aversion is currently in driving seat in the markets today. In the US, hope of fresh fiscal stimulus fades for now, most likely not until after elections. In Europe, countries are going back into lockdowns as coronavirus cases hit records. Negative sentiment drive global stock indices lower and pushed bonds higher. In particular, Germany 10-year yield is back below -0.6 handle while US 10-year yield is struggling around 0.7 and these are signs of nervousness in the markets. In the currency markets Dollar is currently the strongest one, followed by Yen. Australian is the worst performing, followed by New Zealand Dollar.

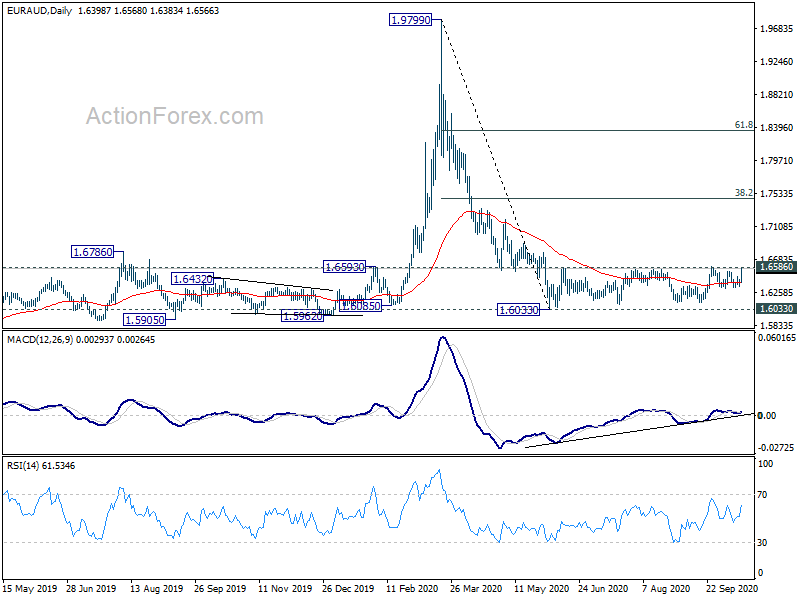

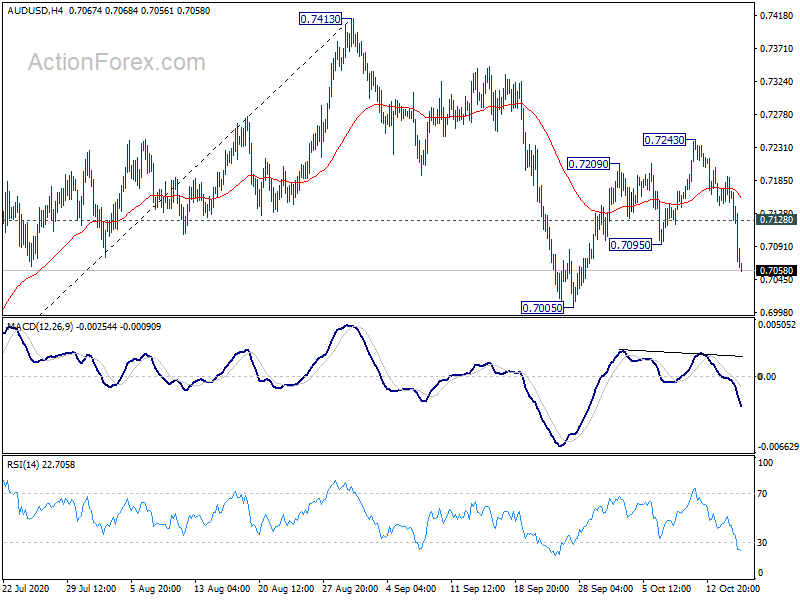

Technically, breakouts are starting to happen with EUR/CHF through 1.0721 support, which should bring deeper fall back to 1.0602 in the near term. AUD/USD’s break of 0.7095 support also suggests that fall from 0.7413 is resuming through 0.7005 low. GBP/USD is holding above 1.2845 support, GBP/JPY above 135.66 support too. USD/CHF is also held well below 0.9197 resistance. We’d like to see these levels taken out firmly to confirm full return of risk-off markets. Meanwhile, a big one to watch is 1.6586 resistance in EUR/AUD, and a break there would be a strong indication of underlying near term bearishness in Aussie.

In Europe, FTSE is currently down -2.35%. DAX is down -3.14%. CAC is down -2.68%. German 10-year yield is down -0.0560 at -0.635. Earlier in Asia, Nikkei dropped -0.51%. Hong Kong HSI dropped -2.06%. China Shanghai SSE dropped -0.26%. Singapore Strait Times dropped -1.25%. Japan 10-year JGB yield dropped -0.0079 to 0.023.

US initial jobless claims rose to 898k, continuing claims dropped to 10m

US initial jobless claims rose 53k to 898k in the week ending October 10, above expectation of 810k. Four-week-moving average of initial close rose 8k to 866k.

Continuing claims dropped -1165k to 10018k in the week ending October 3. Four-week moving average of continuing claims dropped -682k to 11482.

Empire State manufacturing dropped to 10.5, but Philly Fed survey surged to 32.3

US Empire State Manufacturing index dropped to 10.5 in October, down from 17.0, missed expectation of 16.5. Six months ahead expectation also dropped -7.5 to 32.8.

Philly Fed Manufacturing index, on the other hand, rose sharply to 32.3, up form 15.0, well above expectation of 15.5. it’s the fifth consecutive positive reading after reaching long-term lows in April and May.

UK: A negotiated Brexit outcome is still our preference

According to his spokesman, UK Prime Minister Boris Johnson was updated by chief Brexit negotiator David Frost that negotiations were still stuck over fisheries and level playing field competition guarantees. But the spokesman reiterated, “we look forward to hearing the outcome of the European Council and would reflect on that before setting out the UK’s next steps. We’ve always been clear that a negotiated outcome is our preference.”

On the other, according to a draft of the EU summit conclusion, “the European Council invites the Union’s chief negotiator to continue negotiations in the coming weeks, and calls on the UK to make the necessary moves to make an agreement possible”.

RBA Lowe hints at more easing in November

RBA Governor Philip Lowe hinted in a speech that the central bank is ready for deliver more monetary easing in the upcoming meeting in November. He noted that “as the economy opens up, though, it is reasonable to expect that further monetary easing would get more traction than was the case earlier.”

Lowe also noted that that financial stability considerations “have changed somewhat”. To the extent that an easing of monetary policy helps people get jobs it will help private sector balance sheets and lessen the number of problem loans. In so doing, it can reduce financial stability risks.”

Also, while RBA’s balance sheet has “increased considerably” since March, “large increases have occurred in other countries. RBA is “considering the implications os this as we work through out own options”.

Lowe’s comments are in line with market expectations of another cut in cash rate to 0.10%, with expansion of asset purchases to longer maturities.

Australia employment dropped -29.5k in Sep, unemployment rate rose to 6.9%

Australia employment dropped -29.5k in September, better than expectation of -50k. Full-time jobs dropped -20.1k while part-time jobs decreased by -9.4k. Unemployment rate rose 0.1% to 6.9%, below expectation of 7.1%. But at the same time, participation rate dropped -0.1% to 64.8%.

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.7146; (P) 0.7169; (R1) 0.7184; More…

AUD/USD’s strong break of 0.7095 suggests that recovery from 0.7005 has completed at 0.7243. Correction fall form 0.7413 should be ready to resume. Intraday bias is back on the downside for 0.7005 first. Break will target 38.2% retracement of 0.5506 to 0.7413 at 0.6685. On the upside, above 0.7128 minor resistance will dampen this bearish case and turn bias neutral first.

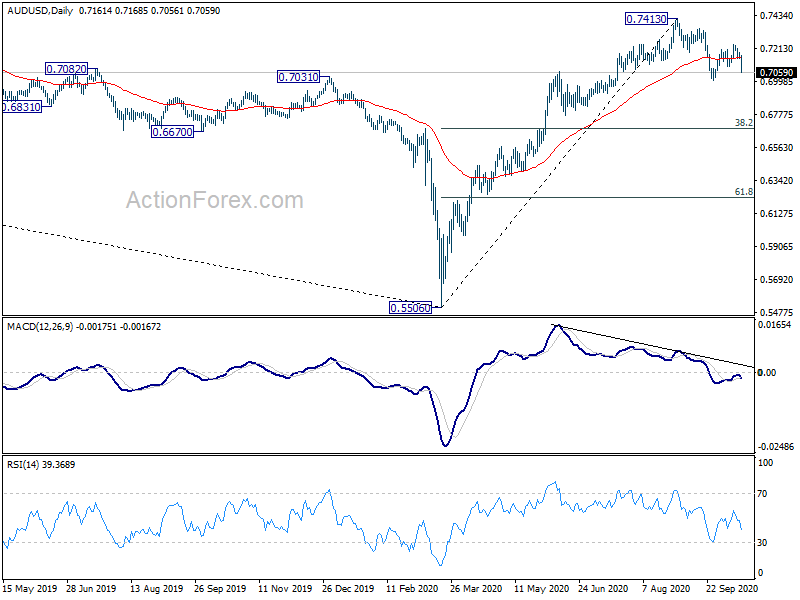

In the bigger picture, while rebound from 0.5506 was strong, there is not enough evidence to confirm bullish trend reversal yet. That is, it could be just a corrective inside the long term up trend. Sustained trading back below 55 week EMA (now at 0.6915) will favor the bearish case and argue that the rebound has completed. Focus will be turned back to 0.5506 low. On the upside, break of 0.7413 will extend the rise from 0.5506 to 38.2% retracement of 1.1079 (2011 high) to 0.5506 (2020 low) at 0.7635.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:00 | AUD | Consumer Inflation Expectations Oct | 3.40% | 3.10% | ||

| 00:30 | AUD | Employment Change Sep | -29.5K | -50K | 111K | 129.1K |

| 00:30 | AUD | Unemployment Rate Sep | 6.90% | 7.10% | 6.80% | |

| 01:30 | CNY | CPI Y/Y Sep | 1.70% | 1.90% | 2.40% | |

| 01:30 | CNY | PPI Y/Y Sep | -2.10% | -2.00% | -2.00% | |

| 04:30 | JPY | Tertiary Industry Index M/M Aug | 0.80% | -0.30% | -0.50% | -0.10% |

| 06:30 | CHF | Producer and Import Prices M/M Sep | 0.10% | 0.20% | -0.40% | |

| 06:30 | CHF | Producer and Import Prices Y/Y Sep | -3.10% | -3.50% | ||

| 12:30 | CAD | ADP Employment Change Sep | -240.8K | -205.4K | -770.6K | |

| 12:30 | USD | Empire State Manufacturing Index Oct | 10.5 | 16.5 | 17 | |

| 12:30 | USD | Philadelphia Fed Survey Oct | 32.3 | 15.5 | 15 | |

| 12:30 | USD | Initial Jobless Claims (Oct 9) | 898K | 810K | 840K | 845K |

| 12:30 | USD | Import Price Index M/M Sep | 0.30% | 0.40% | 0.90% | |

| 14:30 | USD | Natural Gas Storage | 58B | 75B | ||

| 15:00 | USD | Crude Oil Inventories | -2.1M | 0.5M |

{kind=link}