Sterling opened the week broadly lower after Brexit trade negotiations missed yet another deadline. Additionally, European countries rushed to ban travel from UK as coronavirus infections worsened. Aussie and Kiwi are trailing as the next weakest on mild risk aversion. On the other hand, Dollar, Yen and Swiss Franc are the stronger ones. The economic calendar is very light in a holiday shortened week. Though, volatility might spike in thin markets.

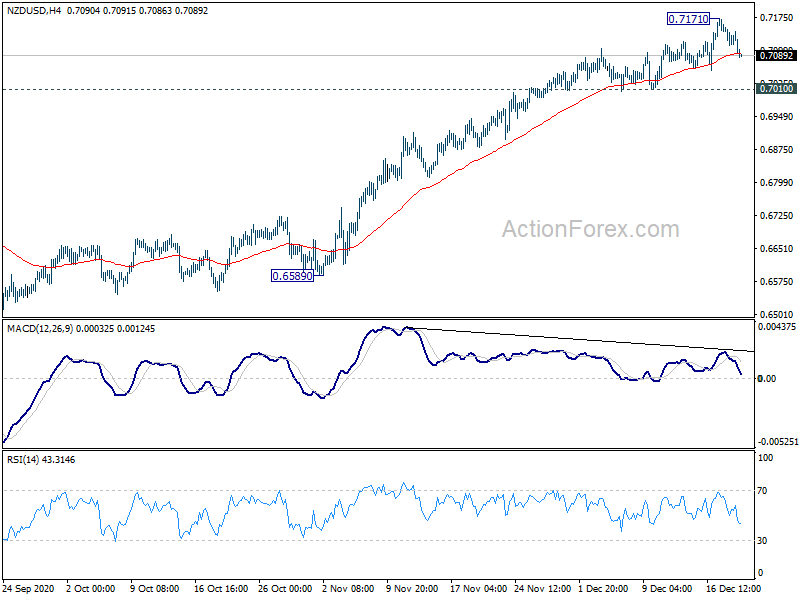

Technically, Dollar’s rebound today set up divergence conditions in 4 hour MACD in many pairs. There is prospect of more sustainable rebound. Yet, some key near term levels need to be taken out first. Those levels include 1.2058 support in EUR/USD, 0.7507 support in AUD/USD, and 1.2928 resistance in USD/CAD. Technically, NZD/USD needs to break 0.7010 support to confirm short term topping too.

In Asia, Nikkei closed down -0.18%. Hong Kong HSI is down -0.28%. China Shanghai SSE is up 0.54%. Singapore Strait Times is up 0.09%. Japan 10-year JGB yield is down -0.0008 at 0.012.

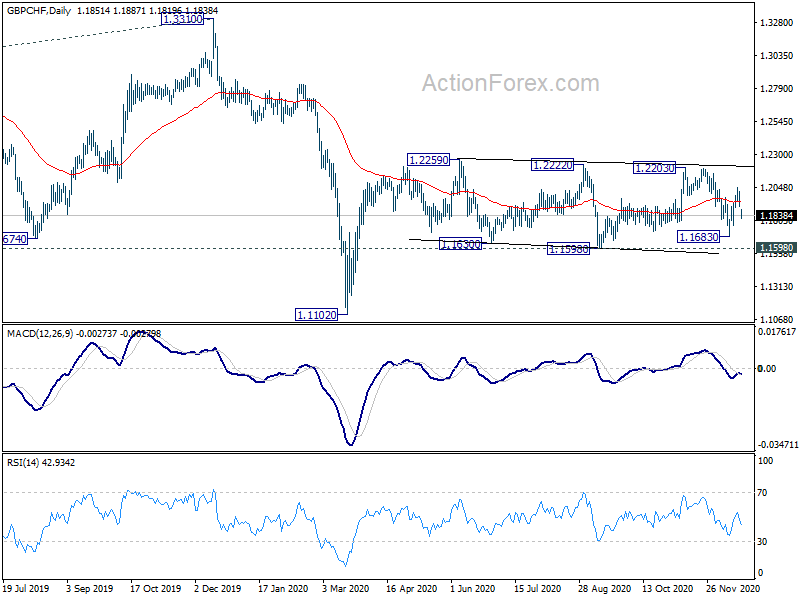

GBP/CHF gapped down as Brexit trade negotiation missed another deadline

Sterling gaps lower as Brexit trade negotiation missed yet another deadline. European Parliament wouldn’t have time to scrutinize and approve the texts even if a deal could be reached in the next few days. Both sides have to make preparations for a “no-deal period” at least, as the end of the transition looms.

Additionally, a new variant of the coronavirus virus has plunged south-east England into a tier-4 lockdown. Countries including France, Germany, Italy, Ireland and the Netherlands introduced bans on arrivals from the UK.

While GBP/CHF gapped down today and stayed pressured through the Asian session, it’s still comfortably trading around the mid-point of recently established range. No special technical development was made as traders are, understandably, refusing to commit to a direction.

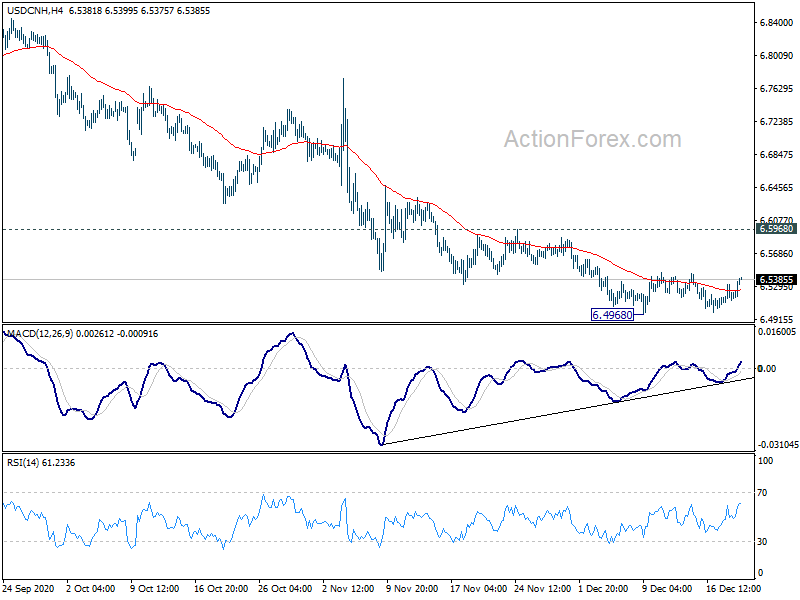

PBoC left 1-yr LPR unchanged at 3.85%, USD/CNH recovers in consolidation

China’s PBoC left the one-year loan prime rate (LPR) unchanged at 3.85% today. The five-year LPR was held at 4.65%. These benchmark lending rates for corporate and household loans were kept unchanged for the eight straight months. Some economists saw that with the economic recovery on the right track, PBoC policy focus would gradually shift away from supporting growth. Keeping LPRs unchanged would provide the base for the central bank to hike its policy rates next year.

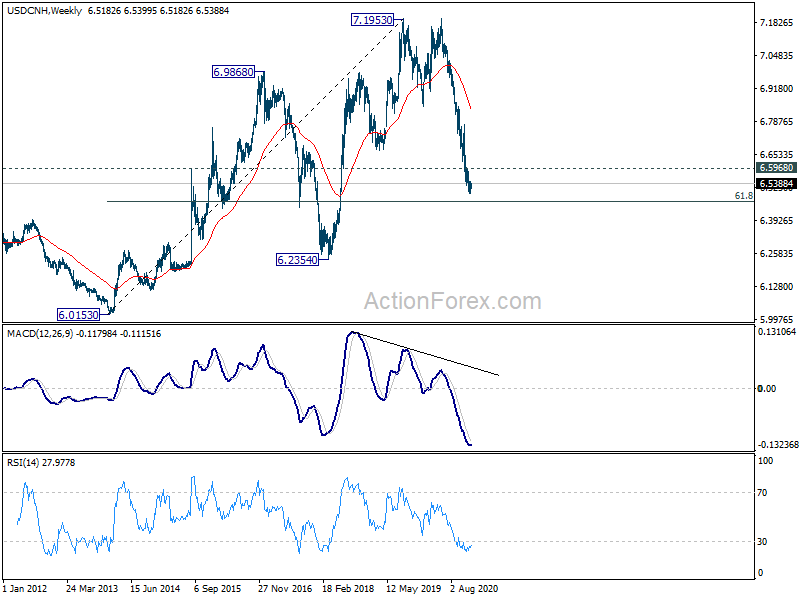

Offshore Yuan trades a little weaker today, mainly as dollar recovers. USD/CNH continues to consolidate above 6.4968 temporary low. Near term outlook stays bearish, with another fall expected, as long as 6.5968 resistance holds. USD/CNH could have a take on 61.8% retracement of 6.0153 to 7.1953 at 6.4661 before forming a bottom.

Japan Cabinet approves record budget for fiscal 2021

Japan’s Cabinet approved today a record JPY 106.61T draft budget for fiscal 2021. New bond issuances would soar JPY 11.04T from the current JPY 43.60T finance the budget. That’s the first year-on-year rise on an initial basis since fiscal 2010.

“Amid the coronavirus spread, the hardest part was that we had to strike a balance among preventing infections from spreading, revitalizing the economy and restoring fiscal health,” Finance Minister Taro Aso said. He added that it’s “regrettable” that bond dependency ratio would rise again.

US data to be watched in a light week

The economic calendar is understandably light in this holiday shortened week. Main focuses will be on data from the US, including consumer confidence, durable goods orders and personal income and spending. But most attention would be on the trend of jobless claims. Other than that, Canada GDP will also be watched. Here are some highlights for the week:

- Monday: Canada new housing price index; Eurozone consumer confidence.

- Tuesday: Australia retail sales; Germany Gfk consumer climate; UK GDP final, current account, public sector net borrowing; US GDP final, consumer confidence, existing home sales.

- Wednesday: BoJ minutes; Germany import prices; Canada GDP; US durable goods orders, personal income and spending, jobless claims, new home sales.

- Thursday: Japan corporate services prices; Canada building permits.

- Friday: Japan Tokyo CPI core, unemployment rate, retail sales, housing starts.

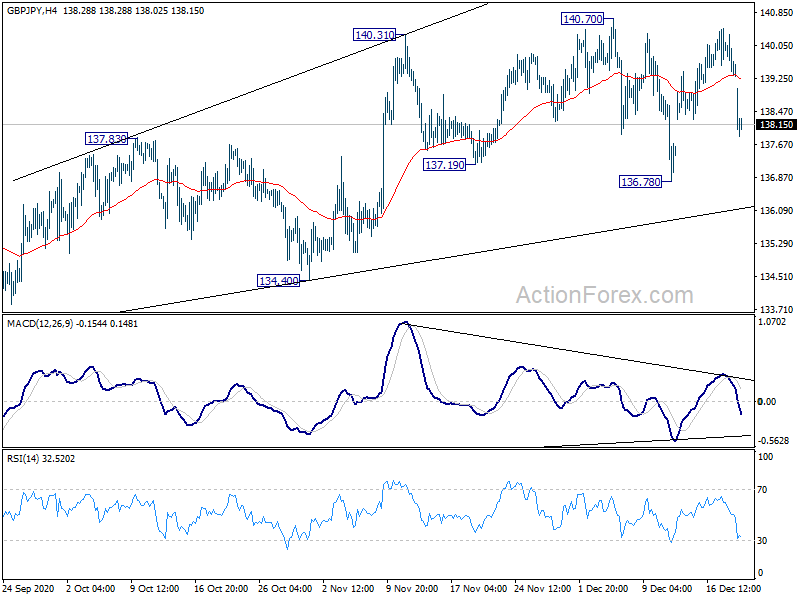

GBP/JPY Daily Outlook

Daily Pivots: (S1) 139.09; (P) 139.70; (R1) 140.09; More…

GBP/JPY drops sharply today but stays in range of 136.78/140.70. Intraday bias remains neutral first. On the upside, firm break of 140.70 will resume the choppy rebound from 133.03 for retesting 141.71 high. On the downside, though, break of 136.78 will turn bias to the downside for 134.40 support first.

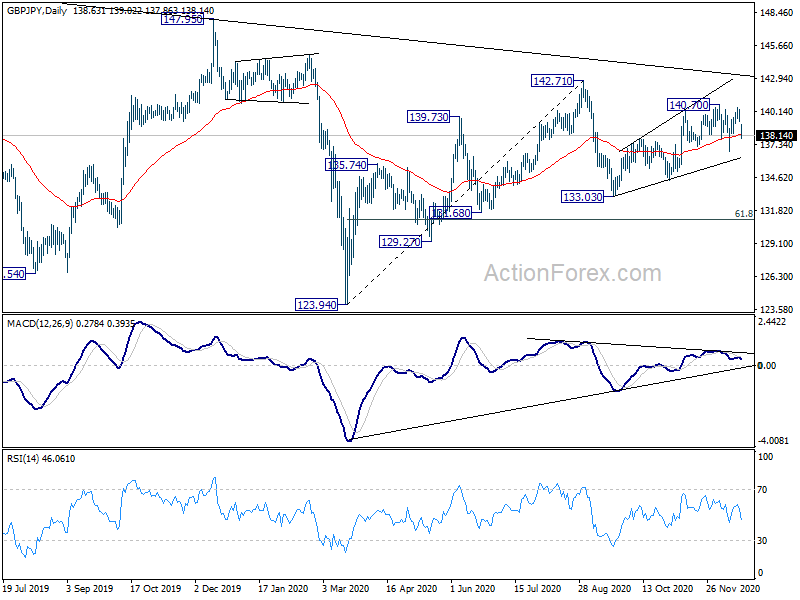

In the bigger picture, rise from 123.94 is seen as a rising leg of the sideway consolidation pattern from 122.75 (2016 low). As long as 147.95 resistance holds, an eventual downside breakout remains in favor. However, firm break of 147.95 will raise the chance of long term bullish reversal. Focus will then be turned to 156.59 resistance for confirmation.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 2:00 | NZD | Credit Card Spending Y/Y Nov | -5.60% | -6.30% | -6.00% | |

| 13:30 | CAD | New Housing Price Index M/M Nov | 0.90% | 0.80% | ||

| 15:00 | EUR | Eurozone Consumer Confidence Dec P | -18 | -18 |

{kind=link}