Euro’s broad based decline continues today, dragging down the Swiss Franc, and to a lesser extent Sterling too. Italy bench yield jumps sharply on increasing risk of fresh elections in the summer. On the other hand, commodity currencies continue to be strong, as supported by overall solid risk sentiments. Global equities are clearly just taking a breather this week, in consolidations. Dollar and Yen are mixed for now, with the greenback holding a slight upper hand.

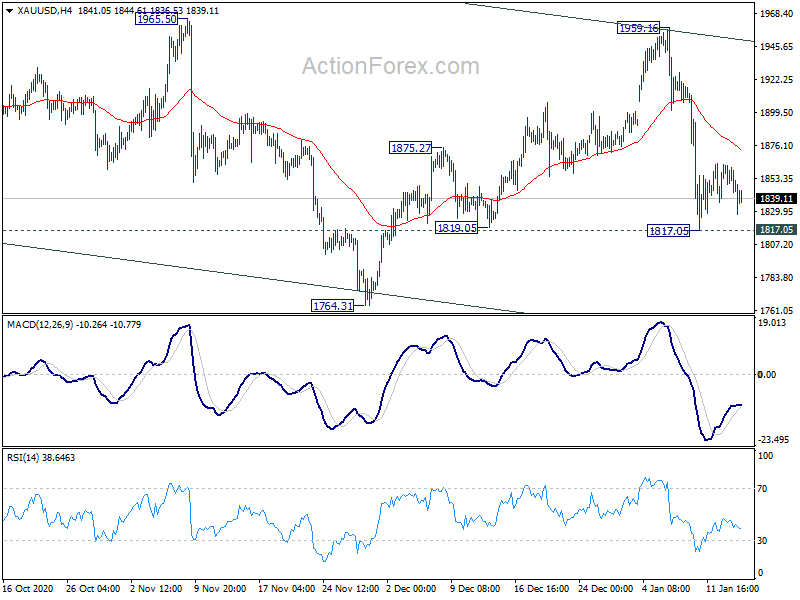

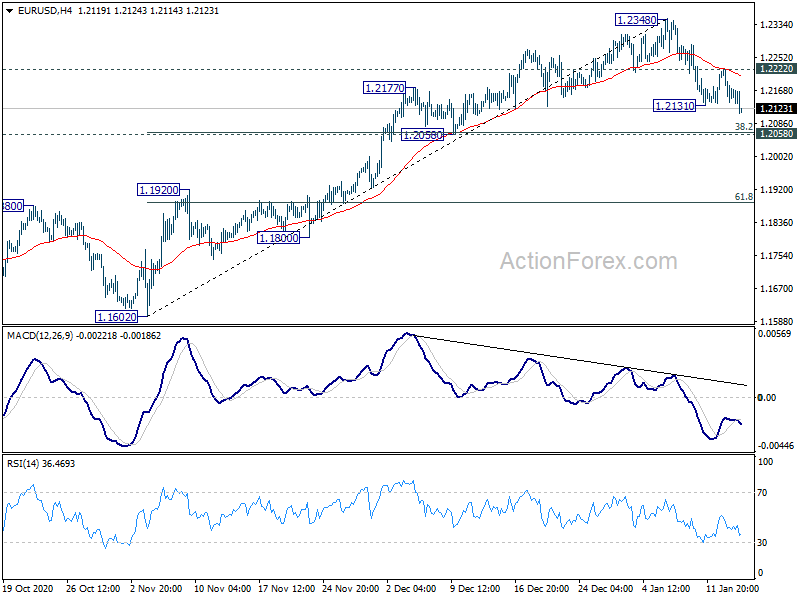

Technically, EUR/USD’s break of 1.2131 suggests that correction from 1.2348 has resumed. While deeper pull back could be seen, we’re looking at strong support from 1.2058 to contain downside. But we’ll see. USD/CHF is also back pressing 0.8918 resistance. Decisive break there should bring even stronger rebound back to 0.8998 support turned resistance. A focus today would be on whether the decline in Euro could help push Gold through 1817.05 temporary low, which is turn helps Dollar rebound elsewhere.

In Europe, currently, FTSE is up 0.44%. DAX is up 0.19%. CAC is up 0.11%. German 10-year yield is down -0.0323 at -0.550. Italy 10-year yield is up 0.072 at 0.663. Earlier in Asia, Nikkei rose 0.85%. Hong Kong HSI rose 0.93%. China Shanghai SSE dropped -0.91%. Singapore Strait Times rose 0.76%. Japan 10-year JGB yield rose 0.0017 to 0.033.

US initial jobless claims rose to 965k

US initial jobless claims rose 181k to 965k in the week ending January 9, well above expectation of 785k. Four-week moving average of initial claims rose 18.3k to 834.3k. Continuing claims rose 199k to 5271k in the week ending January 2. Four-week moving average of continuing claims dropped -59k to 5216k.

Also released, import price index rose 0.9% mom in December, versus expectation of 0.8% mom.

ECB accounts: Extension of PEPP and recalibration of TLTRO III most suitable tool

In the accounts of December 9-10 monetary policy meeting, ECB noted “market sentiment had improved notably following the news of the successful development of vaccines and on account of expected monetary policy measures.” But uncertainty “remained high” and concerns were voiced over exchange rate developments, and the “negative consequences for the inflation outlook.”

The resurgence of the pandemic, downward revision in inflation forecasts and risk of unanchoring inflation expectations, “additional monetary policy measures were necessary”. However, the “current environment warranted a recalibration of policy instruments… rather than the adoption of additional measures”.

“The expansion and extension of PEPP purchases and the recalibration of the TLTRO III conditions were widely seen as the most suitable tools to ensure that financing conditions remained favourable throughout the pandemic.”

BoJ Kuroda: Stand ready to take additional easing steps without hesitation if needed

BoJ Governor Haruhiko Kuroda told branch managers in a quarterly meeting, “domestic economic conditions remain severe due to the impact of coronavirus infections at home and abroad but we have seen a pickup.”

“Japan’s economy is likely to improve as a trend as the impact from the pandemic gradually subsides, although the pace will be moderate as caution over COVID-19 persists,” he added.

“The BOJ will scrutinise the impact of the pandemic for the time being and stand ready to take additional easing steps without hesitation if needed,” he said.

Released from Japan, PPI dropped -2.0% yoy in December, above expectation of -2.2% yoy. Machinery orders rose 1.5% mom in November, well above expectation of -6.2% mom decline.

China’s exports rose 18.1% yoy in Dec, imports rose 6.5% yoy

In USD terms, China’s exports rose 18.1% yoy to USD 281.9B in December. Imports rose 6.5% yoy to USD 203.8B. Total trade rose 12.9% yoy to USD 485.7B. Trade surplus came in at USD 78.2B, above expectation of USD 72.0B.

For the whole 2020, exports rose 3.6% to USD 2591B. Imports dropped -1.1% to USD 2056B. Total trade rose 1.5% to USD 4646B. Trade surplus was at USD 535.0B.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2124; (P) 1.2173; (R1) 1.2207; More…

EUR/USD’s correction from 1.2348 resumes by breaking through 1.2131. Intraday bias is back on the downside for further fall. But downside should be contained by 1.2058 cluster support (38.2% retracement of 1.1602 to 1.2348 at 1.2063) to bring rebound. Break of 1.2222 minor resistance will bring retest of 1.2348 high. However, firm break of 1.2058 will target 61.8% retracement at 1.1887.

In the bigger picture, rise from 1.0635 is seen as the third leg of the pattern from 1.0339 (2017 low). Further rally could be seen to cluster resistance at 1.2555 next, (38.2% retracement of 1.6039 to 1.0339 at 1.2516). This will remain the favored case as long as 1.1602 support holds. We’d be alerted to topping sign around 1.2516/55. But sustained break there will carry long term bullish implications.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | PPI Y/Y Dec | -2.00% | -2.20% | -2.20% | -2.30% |

| 23:50 | JPY | Machinery Orders M/M Nov | 1.50% | -6.20% | 17.10% | |

| 00:01 | GBP | RICS Housing Price Balance Dec | 65% | 61% | 66% | |

| 02:00 | CNY | Trade Balance (USD) Dec | 78.2B | 72.0B | 75.4B | |

| 02:00 | CNY | Imports (USD) Y/Y Dec | 6.50% | 4.50% | ||

| 02:00 | CNY | Exports (USD) Y/Y Dec | 18.10% | 21.10% | ||

| 02:00 | CNY | Trade Balance (CNY) Dec | 517B | 466B | 507B | |

| 02:00 | CNY | Imports (CNY) Y/Y Dec | -0.20% | -0.80% | ||

| 02:00 | CNY | Exports (CNY) Y/Y Dec | 10.90% | 14.90% | ||

| 12:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 13:30 | USD | Initial Jobless Claims (Jan 8) | 965 K | 785K | 787K | 784 K |

| 13:30 | USD | Import Price Index M/M Dec | 0.90% | 0.80% | 0.10% | 0.20% |

| 17:00 | USD | Natural Gas Storage | -129B | -130B |

{kind=link}