Markets continue to reverse some of last week’s move, as seen in the rebound in European and Asian equities. Dollar, Yen and Swiss Franc all turned weaker while commodity currencies strengthened. PMIs from Eurozone and UK are all solid, despite mild pull back. Yet, both are outshone by commodity currencies. Sterling is currently having a slight upper hand against Euro.

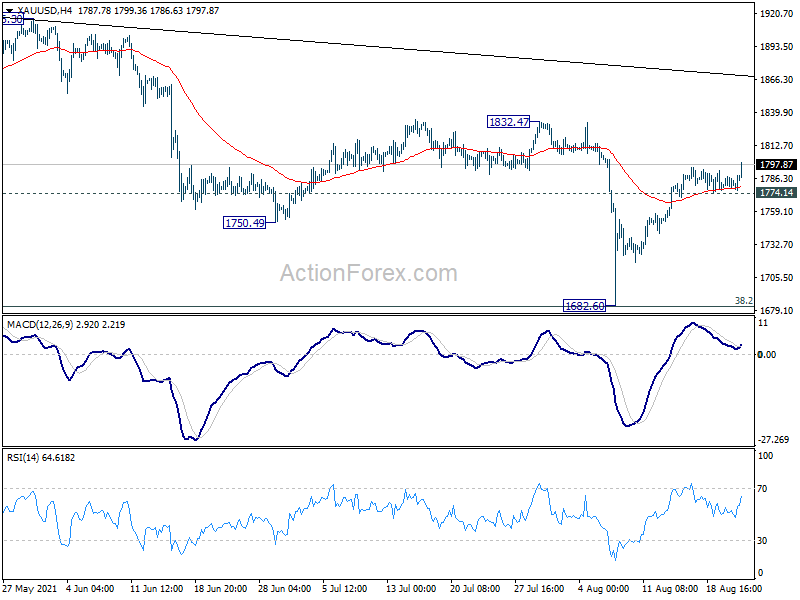

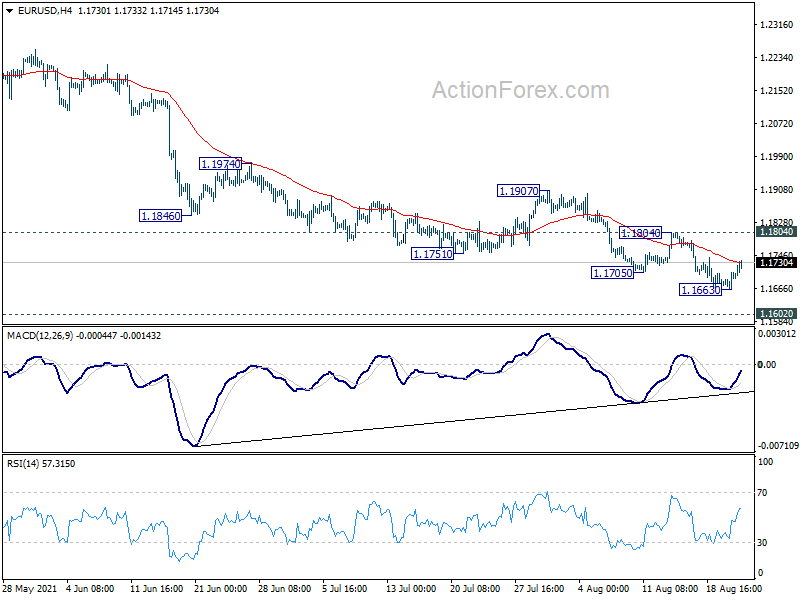

Technically, however, there is no clear sign of reversal for Dollar, Yen and Franc yet. Though, Gold’s break of 1795.42 resistance now suggests resumption of rebound from 1682.60. Reaction to 1800 handle will be watched, and sustained trading above would pave the way to retest 1832.47 resistance that. We’d see if EUR/USD would follow and break through 1.1084 resistance too.

In Europe, at the time of writing, FTSE is up 0.36%. DAX is up 0.23%. CAC is up 0.89%. Germany 10-year yield is up 0.021 at -0.473. Earlier in Asia, Nikkei rose 1.78%. Hong Kong HSI rose 1.05%. China Shanghai SSE rose 1.45%. Singapore Strait Times dropped -0.49%. Japan 10-year JGB yield rose 0.0070 to 0.019.

UK PMI manufacturing dropped to 60.1, services tumbled to 55.5

UK PMI Manufacturing dropped from 60.4 to 60.1 in August, above expectation of 59.5. PMI Services dropped notably from 59.6 to 55.5, below expectation of 59.0. PMI Composite dropped from 59.2 to 55.3.

Chris Williamson, Chief Business Economist at IHS Markit, said: “Although the PMI indicates that the economy continues to expand at a pace slightly above the pre-pandemic average, there are clear signs of the recovery losing momentum in the third quarter after a buoyant second quarter… rising virus case numbers are deterring many forms of spending… Supplier delays have risen to a degree exceeded only once before… Prices have risen sharply again, albeit with the rate of inflation moving below July’s record high.

“More positively, business expectations for the year ahead perked up in August, encouraging a record jump in employment as furloughed workers were brought back to the workplace. However, demand and supply availability need to improve further for this rise in employment to be sustained in coming months”.

Bundesbank: Output to rise sharply in summer

In the monthly report, Bundesbank said German economic output is “likely to rise sharply in summer 2021”, more strongly than in Spring. Industry was unable to take advantage of the growth in Q2 due to increased delivery bottlenecks. But there are initial signs that these delivery bottlenecks are “at least not worsening”. It remains to be seen if GDP could reach pre-crisis level in Summer or not until Autumn.

Inflation is expected to continue to rise in Germany, but then “decrease noticeably again at the beginning of 2022”, as the base effect will then no longer apply. Though, inflation could still be over 2% until mid-2022.

Eurozone PMI composite ticked down to 59.5, recovery retained impressive momentum

Eurozone PMI Manufacturing dropped from 62.8 to 61.5 in August, below expectation of 62.0. PMI Services dropped from 59.8 to 59.7, below expectation of 59.8. PMI Composite dropped from 60.2 to 59.5.

Chris Williamson, Chief Business Economist at IHS Markit said: “The eurozone’s economic recovery retained impressive momentum in August, with the PMI dipping only slightly from July’s recent high to put its average in the third quarter so far at the highest for 21 years… Firms benefited from virus containment measures easing to the lowest since the pandemic began…

“Supply chain delays continue to wreak havoc… combined with surging demand, led to another near-record increase in average selling prices for goods and services, though there are some welcome signs that these inflationary pressures may have peaked for now. Encouragement comes from a second month of job creation at the strongest for 21 years… some upward movement on wage growth… which could feed through to higher inflation”.

Germany PMI composite dropped to 60.0, still firmly inside growth territory

Germany PMI Manufacturing dropped from 65.9 to 52.7 in August, below expectation of 65.0. PMI Services dropped from 61.8 to 61.5, above expectation of 61.0. PMI Composite dropped from 62.4 to 60.6.

Phil Smith, Associate Director at IHS Markit said: “With August’s flash PMI still firmly inside growth territory, the recovery of the German private sector looks to be continuing at a healthy pace. Although growth has slowed down since July, the data are still pointing to a stronger economic expansion in the third quarter than the provisional 1.5% increase in GDP seen in the three months to June.”

France PMI composite dropped to 55.9, another strong month of growth

France PMI Manufacturing dropped from 58.0 to 57.3 in July, matched expectations. PMI Services dropped from 56.8 to 56.4, below expectation of 57.0. PMI Composite dropped form 56.6 to 55.9.

Joe Hayes, Senior Economist at IHS Markit said: “Another strong month of growth across France was signalled by the flash PMI figure for August. Despite some of the challenges businesses are facing on the supply side, it’s encouraging to see PMI data consistently signalling robust expansion. Furthermore, given we’re now midway through the third quarter, the survey data up to this point suggest we could see another decent out turn in the corresponding GDP figure.”

Japan PMI composite dropped to 45.9 in Aug, weaker demand and sustained supply chain pressures

Japan PMI Manufacturing dropped from 53.0 to 52.4 in August, below expectation of 53.4. PMI services dropped sharply from 47.4 to 43.5, worst in 15 months. PMI Composite dropped from 48.8 to 45.9, worst since August 2020.

Usamah Bhatti, Economist at IHS Markit, said: “The Japanese private sector economy saw business conditions deteriorate further midway through the third quarter of the year, with flash PMI data signalling a quicker decline in business activity in August. The latest contraction was the quickest recorded since August 2020, while incoming business was reduced at the sharpest pace for seven months. Survey respondents commonly attributed weaker demand to ongoing COVID-19 restrictions, coupled with sustained supply chain pressures.”

Australia PMI composite dropped to 15-month low, heavily impacted by restrictions

Australia PMI Manufacturing dropped from 56.9 to 51.7 in August, hitting a 14-month low. PMI Services dropped from 44.2 to 43.3, a 15-month low. PMI Composite dropped from 45.2 to 43.5, also a 15-month low.

Jingyi Pan, Economics Associate Director at IHS Markit, said: “Australia’s private sector remained stuck in decline in August… as activity remained heavily impacted by current mobility restrictions brought about by the spread of the COVID-19 Delta variant. Not only were demand and business activity hit, employment conditions also deteriorated, with private sector staffing levels falling for the first time since October 2020… The one bright spot had been an improvement in the outlook amongst Australian private sector firms in August, with hopes of an improvement in the COVID-19 situation expected to spark an eventual rebound for the Australian economy.”

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1674; (P) 1.1690; (R1) 1.1715; More…

EUR/USD’s recovery from 1.1663 continues but stays below 1.1804 resistance. Intraday bias remains neutral first. In case of another fall, we’d continue to look for strong support from 1.1602/1703 key support zone to bring rebound. On the upside, above 1.1804 resistance will turn bias back to the upside for 1.1907 resistance first. However, sustained break of 1.1602/1703 will carry larger bearish implication and pave the way to 1.1289 fibonacci support.

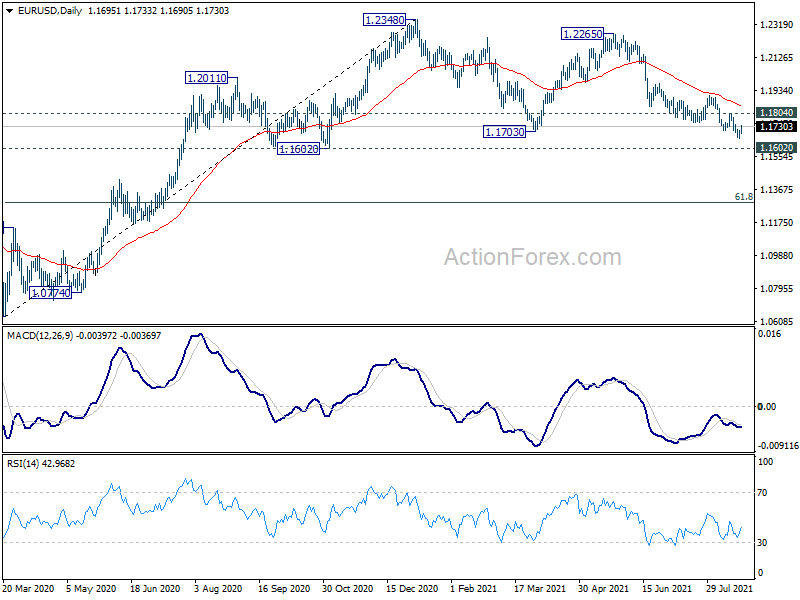

In the bigger picture, rise from 1.0635 is seen as the third leg of the pattern from 1.0339 (2017 low). Further rally remains in favors long as 1.1602 support holds, to cluster resistance at 1.2555 next, (38.2% retracement of 1.6039 to 1.0339 at 1.2516). However sustained break of 1.1602 will argue that the rise from 1.0635 is over, and turn medium term outlook bearish again. Deeper fall would be seen to 61.8% retracement of 1.0635 to 1.2348 at 1.1289 and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:00 | AUD | Manufacturing PMI Aug P | 51.7 | 56.9 | ||

| 23:00 | AUD | Services PMI Aug P | 43.3 | 44.2 | ||

| 0:30 | JPY | Manufacturing PMI Aug P | 52.4 | 53.4 | 53 | |

| 7:15 | EUR | France Manufacturing PMI Aug P | 57.3 | 57.3 | 58 | |

| 7:15 | EUR | France Services PMI Aug P | 56.4 | 57 | 56.8 | |

| 7:30 | EUR | Germany Manufacturing PMI Aug P | 62.7 | 65 | 65.9 | |

| 7:30 | EUR | Germany Services PMI Aug P | 61.5 | 61 | 61.8 | |

| 8:00 | EUR | Eurozone Manufacturing PMI Aug P | 61.5 | 62 | 62.8 | |

| 8:00 | EUR | Eurozone Services PMI Aug P | 59.7 | 59.8 | 59.8 | |

| 8:30 | GBP | Manufacturing PMI Aug P | 60.1 | 59.5 | 60.4 | |

| 8:30 | GBP | Services PMI Aug P | 55.5 | 59 | 59.6 | |

| 13:45 | USD | Manufacturing PMI Aug P | 63 | 63.4 | ||

| 13:45 | USD | Services PMI Aug P | 59.9 | 59.9 | ||

| 14:00 | USD | Existing Home Sales Jul | 5.83M | 5.86M | ||

| 14:00 | EUR | Eurozone Consumer Confidence Aug P | -5 | -4 |

{kind=link}