Risk aversion seems to have eased a bit today, with recoveries seen in European markets and US futures. Yen and Dollar have both turned into sideway consolidations. But no clear support is seen in Aussie and New Zealand, as both remain under pressured. Meanwhile, Swiss Franc and Canadian Dollar are taking the lead and strengthen broadly. But overall, traders are rather cautious as a wave of central bank announcements will start tomorrow.

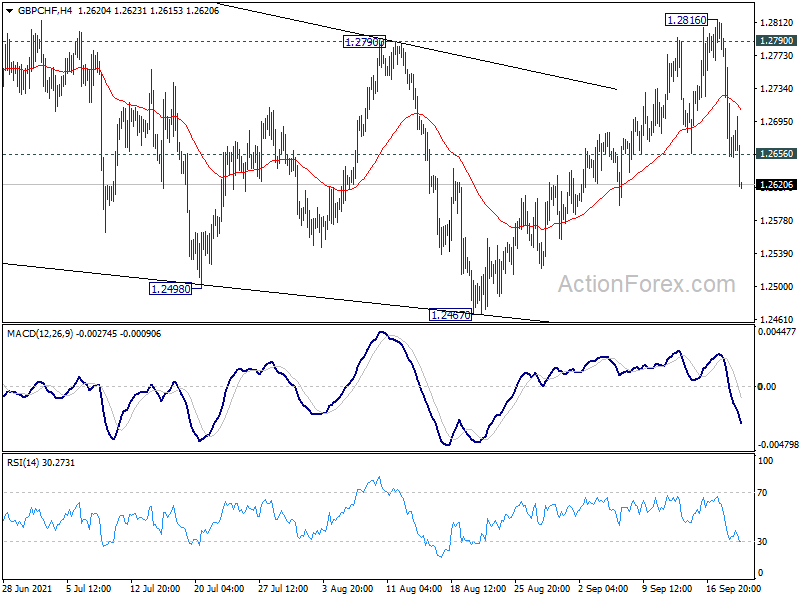

Technically, GBP/CHF finally takes out 1.2656 support firmly today, which indicates completion of the rebound from 1.2467. The rejection by 1.2790 resistance retains near term bearishness and GBP/CHF would now be targeting 1.2467 low. Meanwhile, EUR/CHF is also pressing 1.0837 support and firm break there will align the outlook that rebound from 1.0694 has completed. EUR/CHF could then target a retest on 1.0694 low.

In Europe, at the time of writing, FTSE is up 1.13%. DAX is up 1.44%. CAC is up 1.39%. Germany 10-year yield is down -0.017 to -0.335. Earlier in Asia, Nikkei dropped -2.17%. Hong Kong HSI rose 0.51%. Singapore Strait Times rose 0.71%. Japan 10-year JGB yield dropped -0.0101 to 0.040. China was on holiday.

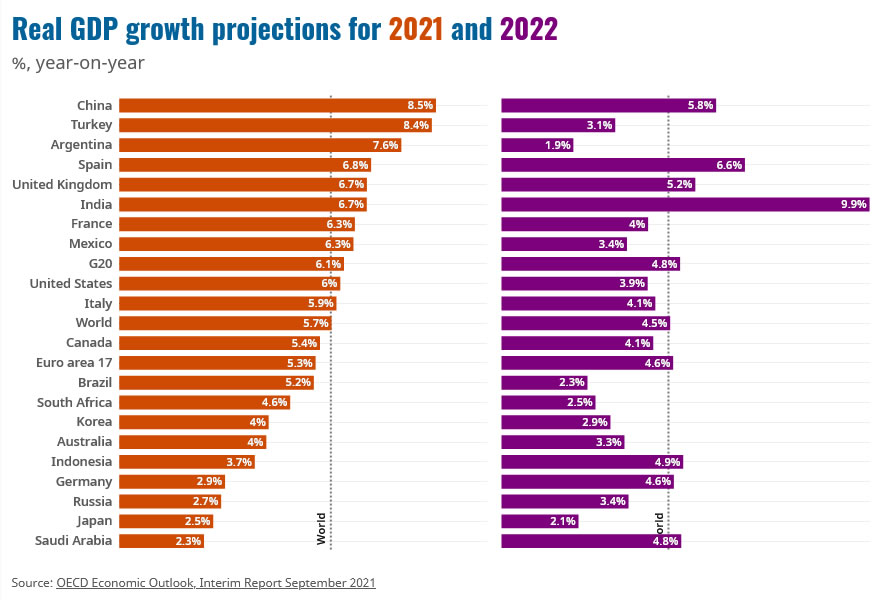

OECD lowers 2021 global growth forecast slightly to 5.7%

OECD lowered 2021 global growth forecast slightly to 5.7%, down from May’s projection of 5.8%. 2022 global growth was revised slightly higher to 4.5%, up from 4.4%. It added, “the global economy is growing far more strongly than anticipated a year ago but the recovery remains uneven, exposing both advanced and emerging markets to a range of risks”.

It also said there is a “marked variation in the outlook for inflation”. But the inflationary pressures “should eventually fade”. “Consumer price inflation in the G20 countries is projected to peak towards the end of 2021 and slow throughout 2022. Wage growth remains broadly moderate and medium-term inflation expectations remain contained.”

Chief Economist Laurence Boone said: “Policies have been efficient in buffering the shock and ensuring a strong recovery; planning for more efficient public finances, shifted towards investment in physical and human capital is necessary and will help monetary policy to normalise smoothly once the recovery is firmly established.”

US housing starts rose to 1.62m, building permits rose to 1.73m

US housing starts rose 3.9% mom to1615k in August, above expectation of 1550k. Building permits rose 6.0% mom to 1728k, above expectation of 1600k. Also released, current account deficit came in at USD -190B in Q2, versus expectation of USD -187B.

Also released, Canada housing starts rose 0.7% mom in August, below expectation of 0.8% mom.

RBA Minutes: Economy expected to bounce back as vaccination rates increase and restrictions are eased

In the minutes of the September 7 RBA meeting, it’s noted, “the outbreak of the Delta variant had delayed, but not derailed, the recovery.” The economy was “expected to bounce back as vaccination rates increase and restrictions are eased” but “there was considerable uncertainty about the timing and pace of the recovery, which was likely to be slower than experienced earlier in 2021”. In the central scenario, growth will return in Q4 and its “pre-Delta path in the second half of 2022”.

As a result of the delay in recovery and uncertainty about the future, “progress towards the Bank’s goals was likely to take longer and was less assured”. But at the same time, fiscal policy is “more appropriate” in dealing with a “temporary and sharp reduction in private sector incomes”. Hence, RBA decided to taper purchases to AUD 4B per week, but extend the period to mid February 2022.

RBA also reiterated its commitment to “maintaining highly supportive monetary conditions to achieve a return to full employment in Australia and inflation consistent with the target.” And it will not raise interest rate until 2024.

RBNZ Hawkesby: Employment at maximum sustainable level, price pressures to feed through

RBNZ Assistant Governor Christian Hawkesby said in a speech, “while the demand side of the economy has been more resilient than expected when COVID-19 arrived, the disruption to the supply side of the economy has also been more prolonged than anticipated.” Also, the developments combined are “likely to have reduced the level of maximum sustainable employment”.

He reiterated that in the latest Monetary Policy Statement, it’s noted RBNZ had “more confidence that employment was already at its maximum sustainable level and that pressures on capacity would feed through into more persistent inflation pressures over the medium-term”.

Thus, the “least regrets policy stance” was to “further reduce the level of monetary stimulus so as to anchor inflation expectations and continue to contribute to maximum sustainable employment.” Also, ” whether or not a monetary policy response would be required in response to future health related lockdowns would depend on whether there was a more enduring impact on inflation and employment”.

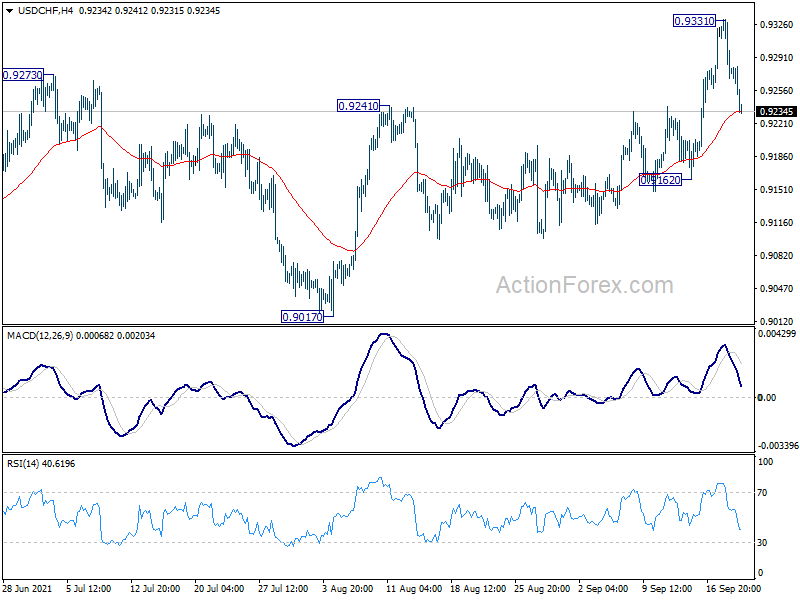

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9254; (P) 0.9294; (R1) 0.9316; More….

USD/CHF’s fall from 0.9331 extends lower today but stays above 0.9162 support. Intraday bias remains neutral first and another rise is still in favor. Rise from 0.8925 is in progress and break of 0.9331 will target 0.9471 key resistance. Sustained break there will carry larger bullish implications. However,m break of 0.9162 will turn bias back to the downside for 0.9017 support instead.

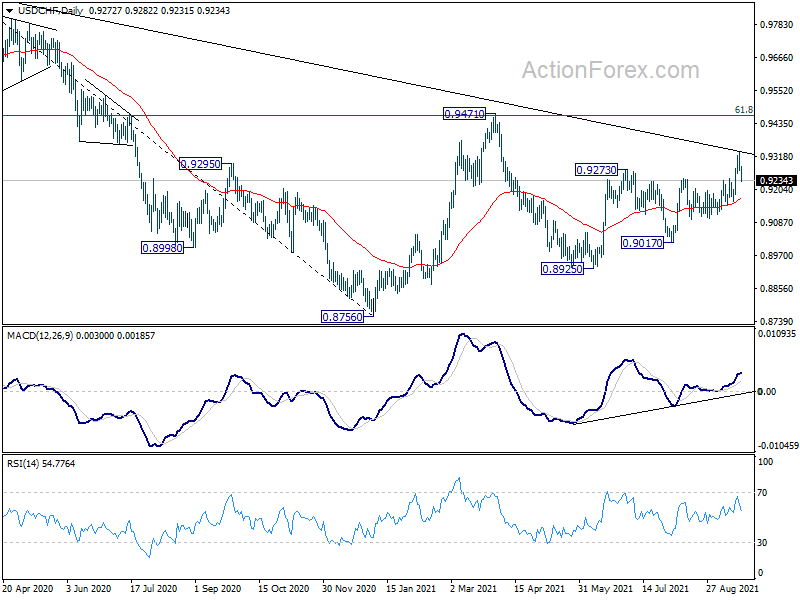

In the bigger picture, the strong rally above 55 week EMA (now at 0.9182) now tilts favor to the case of bullish trend reversal. That is, decline from 1.3042 (2016 high) is probably completed at 0.8756 already. Sustained break of 0.9471 resistance should confirm this case and pave the way to retest 1.0342 ahead. However, rejection by 0.9471 will mix up the outlook again and retain some medium term bearishness.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:00 | NZD | Westpac Consumer Survey Q3 | 102.7 | 107.1 | ||

| 01:30 | AUD | RBA Meeting Minutes | ||||

| 06:00 | CHF | Trade Balance (CHF) Aug | 5.10B | 4.50B | 5.25B | |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Aug | 19.8B | 14.5B | 9.6B | |

| 12:30 | CAD | New Housing Price Index M/M Aug | 0.70% | 0.80% | 0.40% | |

| 12:30 | USD | Building Permits Aug | 1.73M | 1.60M | 1.63M | |

| 12:30 | USD | Housing Starts Aug | 1.615M | 1.55M | 1.53M | |

| 12:30 | USD | Current Account (USD) Q2 | -190B | -187B | -196B |

{kind=link}