Yen and Swiss Franc are currently the strongest ones for the week and remain generally firm. Falling global benchmark treasury yields seem to be supporting both “safe-haven” currencies. Germany 10-year bund yield is back below -0.22, UK 10-year gilt yield is below 0.95 while Japan 10-year JGB yield is back at 0.07. Aussie is worst performing one for the week, followed by Sterling, as selloff continued after their respective central bank meeting. Dollar is firm but needs guidance from non-farm payroll report for taking up a more committed direction.

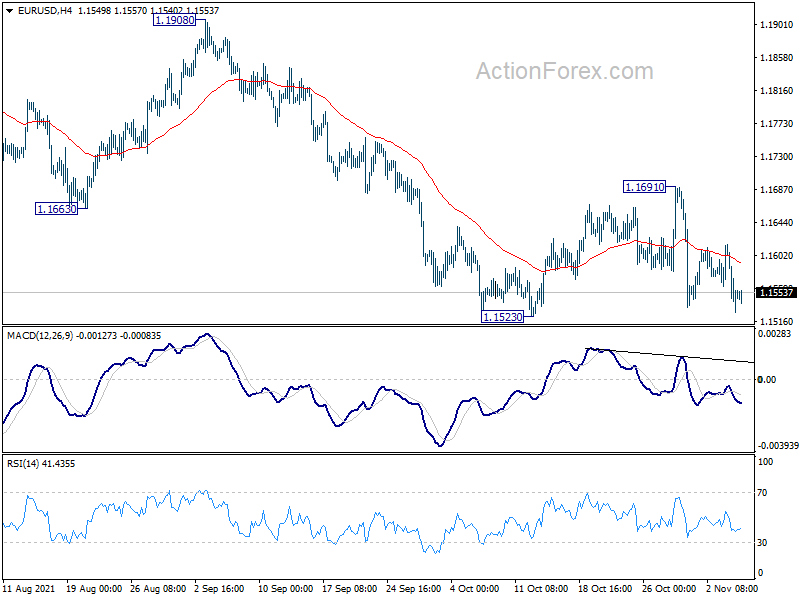

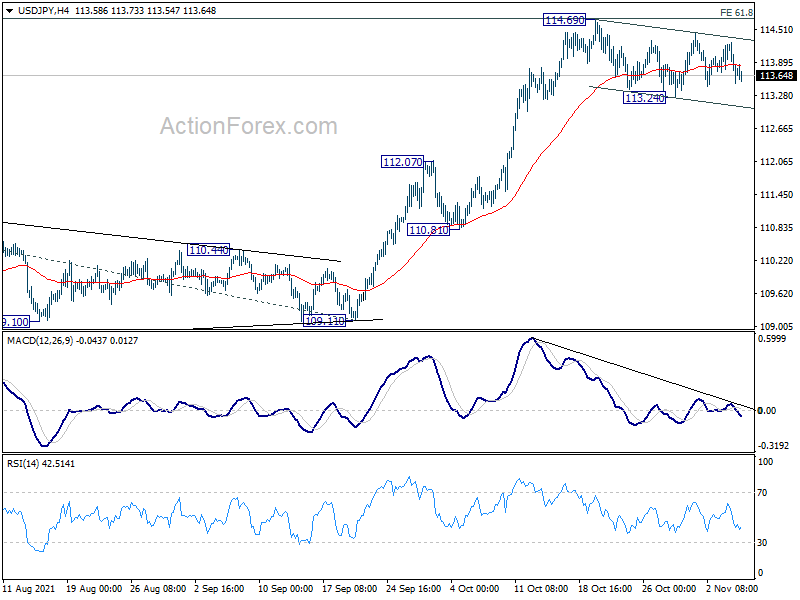

Technically, we’d pay special attention to EUR/USD and USD/JPY today. EUR/USD is now stuck in range of 1.1523/1691. USD/JPY is also bounded inside 113.24/114.69. For now, upside breakout in Dollar is in favor in both pairs. But we’ll have to see if NFP supports that.

In Asia, at the time of writing, Nikkei is down -0.70%. Hong Kong HSI is down -0.99%. China Shanghai SSE is down -0.32%. Singapore Strait Times is up 0.56%. Japan 10-year JGB yield is down -0.012 at 0.070. Overnight, DOW dropped -0.09%. S&P 500 rose 0.42%. NASDAQ rose 0.81%. 10-year yield dropped -0.0055 to 1.524.

RBA SoMP: Inflation forecasts upgraded across horizon

As seen in RBA’s Statement on Monetary Policy, 2021 year-average GDP growth forecasts was downgraded from 4.75% to 4.25%. 2022 GDP year-average GDP growth forecast was left unchanged at 5%. 2023 year-average growth forecast was upgraded from 2.75% to 3%.

Headline CPI inflation forecasts were raised across the horizon, with 2021 year-end increased from 2.5% to 3.25%, 2022 year-end increased from 1.75% to 2.25%, 2023 year-end increased from 2.25% to 2.5%. Trimmed mean inflation forecasts were also raised, with 2021 year-end increased from 1.75% to 2.25%, 2022 year-end from 1.75% to 2.25%, 2023 year-end from 2.25% to 2.5%.

2021 year-end unemployment rate forecast was lowered from 5% to 4.75%. 2022 year-end and 2023 year-end unemployment rate forecast was left unchanged at 4.25% and 4% respectively.

Australia AiG services rose to 47.6 in Oct, third month in contraction

Australia AiG Performance of Services rose 1.9 pts to 47.6 in October, marking a third month in contraction. Sales rose 13.8 to 55.2. Employment rose 4.8 to 56.8. New orders dropped -1.0 to 38.8. supplier deliveries dropped -7.5 to 39.5. Finished stocks dropped -13.7 to 39.8. Capacity utilization dropped -1.7 to 74.5. Input prices rose 9.1 to 73.6. Selling prices rose 7.8 to 61.7. Average wages rose 9.1 to 68.3.

Ai Group Chief Executive, Innes Willox, said: “The Australian services sector reported mixed fortunes in October… Across the services sector, sales and employment were higher in October while new orders were discouragingly low. A more robust recovery was inhibited by lingering activity restrictions, barriers to interstate movement and the same disruptions to the supply of inputs that are being felt in other parts of the economy… Services companies reported further strong rises in input prices and wages with selling prices also rising although not by enough to prevent additional pressure on margins.”

Dollar index awaits NFP to guide range breakout

US non-farm payroll employment is again a major focus. Markets are expecting 425k job growth in October. Unemployment rate is expected to tick down by 0.1% to 4.7%. Average hourly earnings are expected to grow 0.4% mom.

Looking at related data, ISM manufacturing employment rose from 50.2 to 52.0. But ISM services employment dropped from 53.0 to 51.6. ADP private jobs grew 571k, rose slightly from prior month’s 523k. Four-week moving average of initial jobless claims continued to trend down, notably, from 344k to 285k.

All in all, today’s NFP will likely be a solid one, affirming Fed’s tapering plan. The main question ahead is whether wage growth would continue in a strong trend, the pushes up inflation, and force Fed for an earlier hike. Strong wage growth could push Dollar index out of the near term range.

Dollar index is sitting in range below 94.56 short term top. The support from 55 day EMA is a bullish sign. Yet, it will have to break through key long term fibonacci resistance at 94.46 (38.2% retracement of 102.99 to 89.20) decisively to confirm medium term bullishness. In the case, we’d probably seen upside acceleration ahead to 61.8% retracement at 97.72. However, break of 93.27 support will suggest rejection by 94.46, and turn near term outlook bearish for deeper pull back.

Elsewhere

Japan overall household spending dropped -1.9% yoy in September, versus expectation of -3.9% yoy.

Germany industrial production, France industrial output, Italy retail sales, Eurozone retail sales and Swiss foreign currency reserves will be released in European session.

Later in the day, US will release non-farm payrolls and Canada will also release job data and Ivey PMI.

USD/JPY Daily Outlook

Daily Pivots: (S1) 113.42; (P) 113.85; (R1) 114.19; More…

Intraday bias in USD/JPY remains neutral and consolidation from 114.69 could continue. On the upside, firm break of 114.69 will resume the larger up trend to 100% projection of 102.58 to 111.65 from 109.11 at 118.18 next. Break of 113.24 will bring deeper pull back, but downside should be contained above 112.07 resistance turned support to bring rebound.

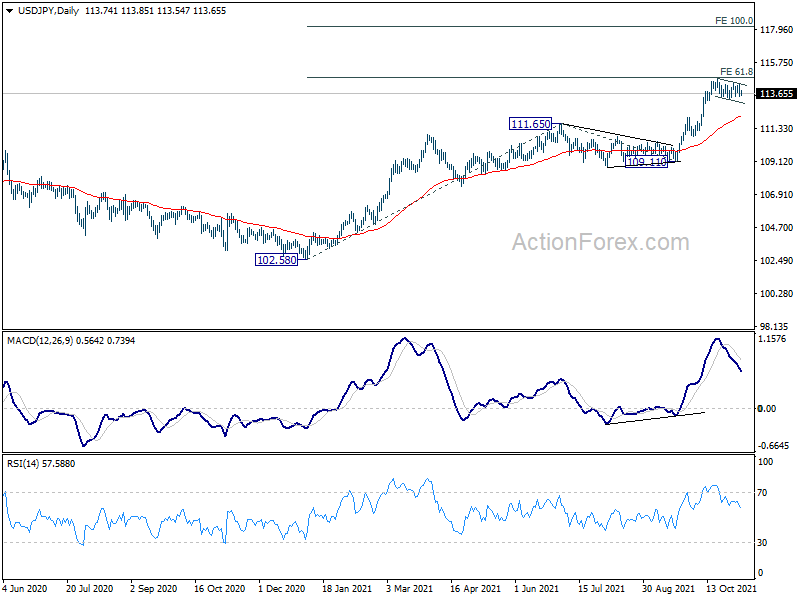

In the bigger picture, corrective decline from 118.65 (2016 high) should have completed at 101.18 already. Rise from the 102.58 is seen as the third leg of the up trend from 101.18. Next target is 114.54 resistance and then 118.65 high. This will now be the preferred case as long as 109.11 support hold, even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Services Index Oct | 47.6 | 45.7 | ||

| 23:30 | JPY | Overall Household Spending Y/Y Sep | -1.90% | -3.90% | -3.00% | |

| 0:30 | AUD | RBA Monetary Policy Statement | ||||

| 7:00 | EUR | Germany Industrial Production M/M Sep | 1.10% | -4.00% | ||

| 7:45 | EUR | France Industrial Output M/M Sep | 0.40% | 1.00% | ||

| 8:00 | CHF | Foreign Currency Reserves (CHF) Oct | 939B | |||

| 9:00 | EUR | Italy Retail Sales M/M Sep | 0.70% | 0.40% | ||

| 10:00 | EUR | Eurozone Retail Sales M/M Sep | 0.20% | 0.30% | ||

| 12:30 | USD | Nonfarm Payrolls Oct | 425K | 194K | ||

| 12:30 | USD | Unemployment Rate Oct | 4.70% | 4.80% | ||

| 12:30 | USD | Average Hourly Earnings M/M Oct | 0.40% | 0.60% | ||

| 12:30 | CAD | Net Change in Employment Oct | 19.3K | 157.1K | ||

| 12:30 | CAD | Unemployment Rate Oct | 6.90% | 6.90% | ||

| 14:00 | CAD | Ivey PMI Oct | 71.2 | 70.4 |

{kind=link}