Risk-aversion dominates Asian markets today as new coronavirus variant sinks investor sentiment. Australian Dollar is leading other commodity currencies lower. Yen and Swiss Franc surge sharply, followed by Euro and Dollar. Overall, it’s flight to safety. The question now is, whether Aussie or Kiwi would eventually end as the worst performing one for the week, and whether Dollar would be overtaken by Yen and Swiss Franc.

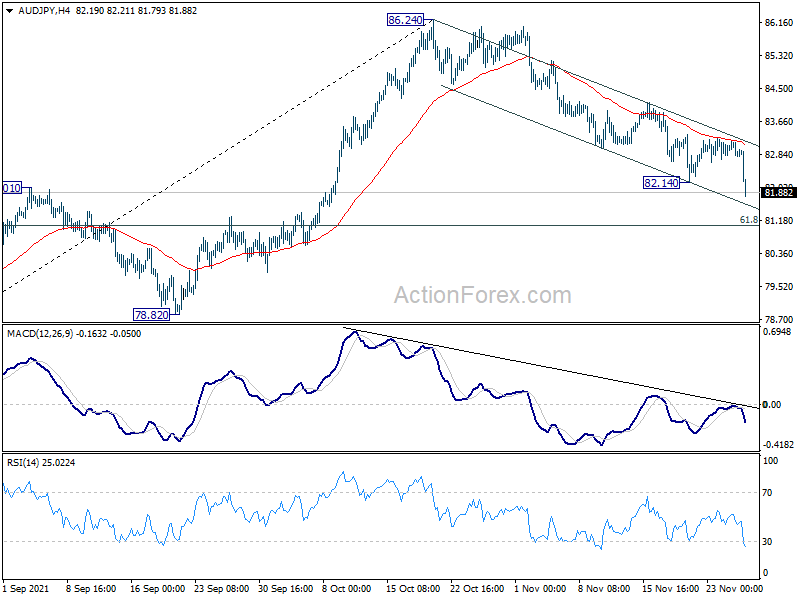

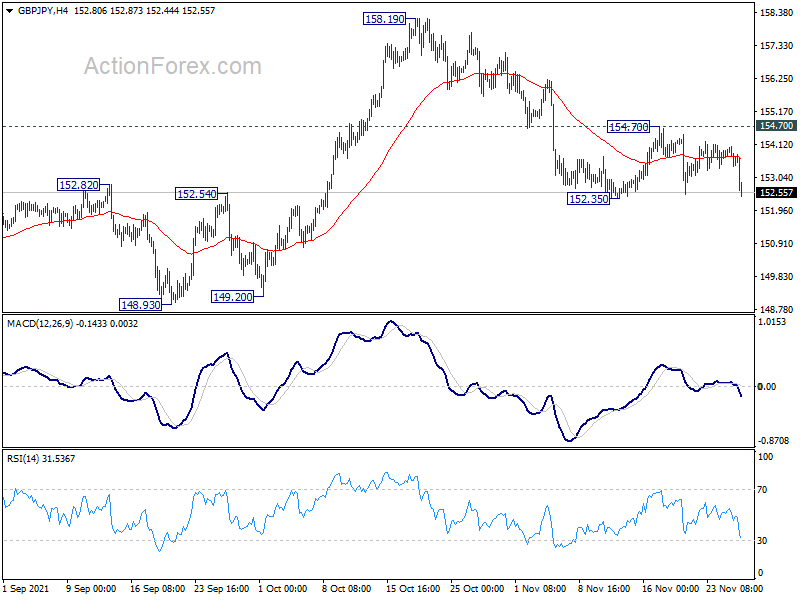

Technically, Yen crosses could take the spotlights today. AUD/JPY has taken the lead in breaking 82.14 support to resume the fall from 86.24. GBP/JPY could break through 152.35 support to resume the fall from 158.19 soon. CAD/JPY might then follow and break through 86.69 support to resume the decline from 93.00 too. But most importantly, the question is whether USD/JPY would break through 113.57 support to complete the case of a broad based turn around in Yen.

In Asia, at the time of writing, Nikkei is down -2.82%. Hong Kong HSI is down -2.24%. China Shanghai SSE is down -0.57%. Singapore Strait Times is down -1.44%. Japan 10-year JGB yield is down -0.0094 at 0.076.

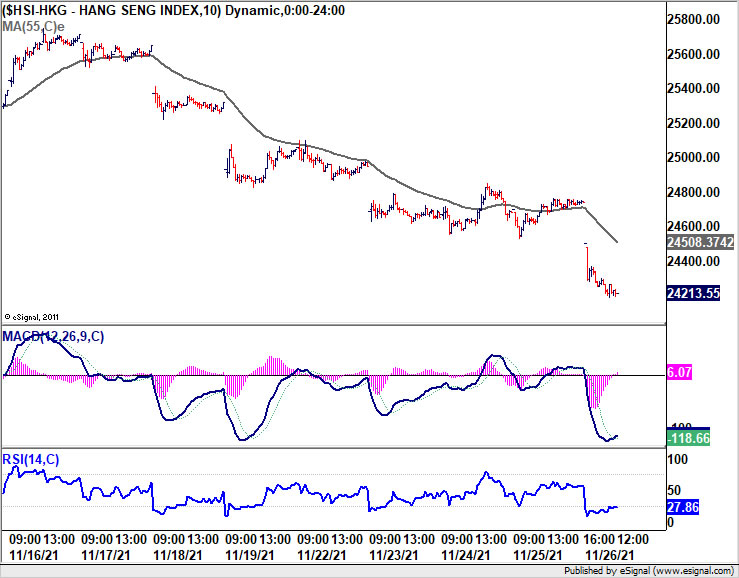

New coronavirus variant sends HK HSI sharply lower

Asian stocks tumble deeply today while US futures are trading sharply lower. The development reflects worries over a new coronavirus variant detected in South Africa. The country’s Health Minister Joe Phaahla warned that there has been “more of an exponential rise” in infections over the last four of five days.

UK is banning flights from South Africa and five other southern African countries. Health Secretary Sajid Javid said there were concerns the new variant “may be more transmissible” than the dominant delta strain, and “the vaccines that we currently have may be less effective” against it.

Hong Kong HSI tumbles sharply today in reaction to the new variant news. HSI is trading well inside medium-term falling channel from 31183.35 high. Rejection by 55 day EMA also keeps outlook bearish. We’re looking at deeper fall to 23681.43 first and then 61.8% projection of 29394.68 to 23681.43 from 26234.93 at 22704.14 next.

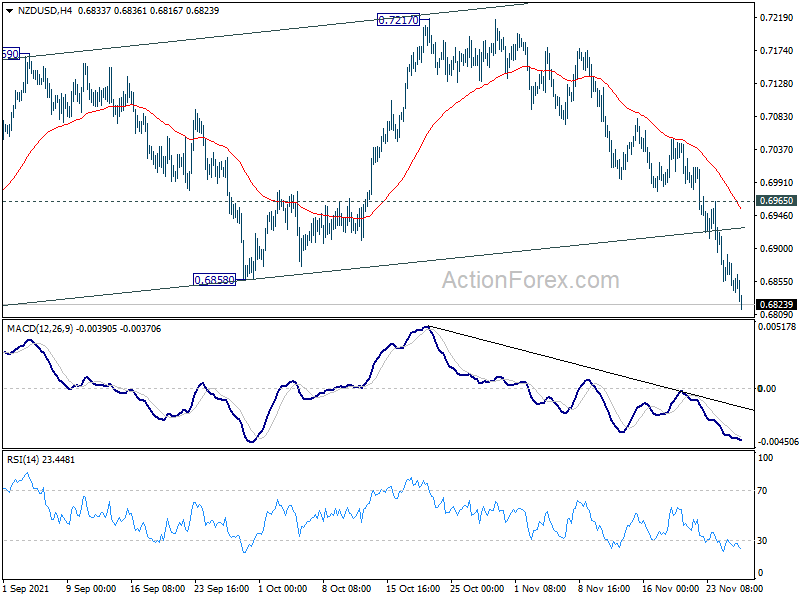

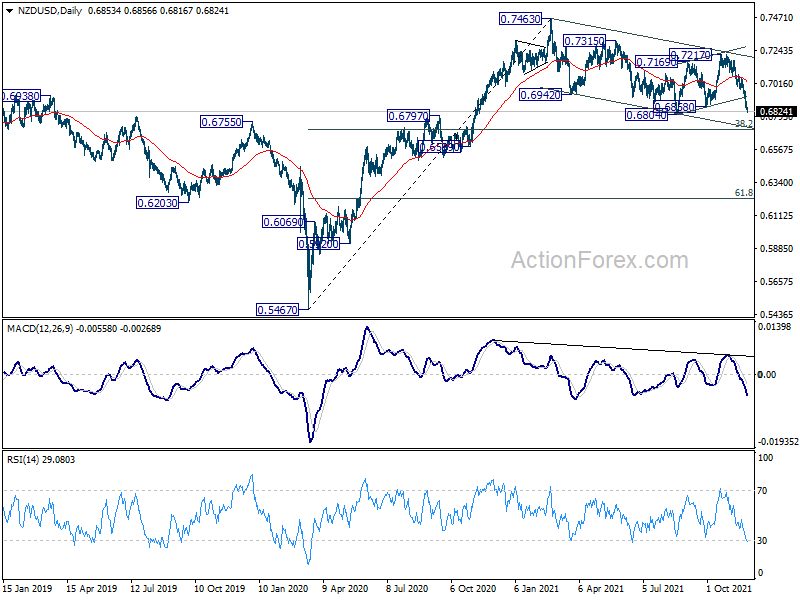

NZD/USD accelerates down to 0.68 and below

NZD/USD accelerates down to as low as 0.6816 so far today, on broad based risk aversion. The break of 0.6858 support should firstly confirmed that corrective rise from 0.6804 has completed with three waves up to 0.7217. More importantly, larger down trend form 0.7463 is now ready to resume.

Further fall is now expected as long as 0.6965 minor resistance holds. Break of 0.6804 will target 38.2% retracement of 38.2% retracement of 0.5467 to 0.7463 at 0.6731 next. We’d tentatively expect strong support from there to complete the fall from 0.7463. Hence, focus will be on bottoming signal as NZD/USD approaches 0.6731.

RBNZ Hawkesby: We need to continue this process of removing stimulus

RBNZ Assistant Governor Christian Hawkesby said in a Bloomberg TV interview, “in New Zealand we’ve had a very resilient economy, we’ve got core inflation running near the top of our 1-3% target range, we’ve got an employment market that’s through what we think it maximum sustainable employment.”

He said, “so we’re getting pretty clear signals that we need to continue this process of removing stimulus and getting interest rates back up towards neutral.”

“Inflation expectations are going to be absolutely key for us. There are things that could make us go faster, and I think inflation expectations is one, he said. “Five- to 10-year inflation expectations are very well anchored. Short-term inflation expectations have lifted with headline, but lifted in a way that we would anticipate, so I think that’s a really key thing to watch.”

“On the upside, the risks are that we’ve had a very strong economy, a big change in the starting point, inflation expectations, there’s a risk that they lift,” he said. “But on the other side, interest rates have moved a long way here in New Zealand, mortgage rates are nearly 2% up from their lows in January, and ahead of us we’re going to have to navigate having Covid in our community.”

Australia retail sales rose 3.9% mom in Oct, still short of pre-delta level

Australia retail sales rose 4.9% mom in October, above expectation of 2.5% mom. That’s the strongest rise since Victoria’s first lockdown bounce back in November 2020, with retail turnover rising to its highest level since June 2021.

“Retail performance continues to be tied to state lockdowns as this month’s recovery was driven by the end of lockdowns in New South Wales, Victoria and the Australian Capital Territory,” Ben James, Director of Quarterly Economy Wide Statistics said.

“With lockdown ending on October 11, New South Wales sales rose 13.3 per cent returning to the levels seen in the months immediately prior to the Delta outbreak, while Victoria and the Australian Capital Territory remain below pre-Delta levels.”

“Although sales have bounced back strongly following the end of lockdowns, it is important to note that overall retail turnover has not yet reached the level of May 2021, the month prior to the Delta outbreak.”

Looking ahead

Swiss will release Q3 GDP in European session while Eurozone will release M3 money supply.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 153.38; (P) 153.73; (R1) 154.03; More…

GBP/JPY is staying in range above 152.35 and intraday bias remains neutral first. With 154.70 resistance intact, further decline is expected . On the downside, break of 152.35 will resume the decline from 158.19 to 148.93 key support next. On the upside, however, break of 154.70 will turn bias back to the upside for retesting 158.19 high instead.

In the bigger picture, rise from 123.94 is seen as the third leg of the pattern from 122.75 (2016 low). Further rally is still expected as long as 148.93 support holds. However, firm break of 148.93 will argue that the medium term trend has reversed and bring deeper fall back to 142.71 resistance turned support first.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y Nov | 0.30% | 0.40% | 0.10% | |

| 0:30 | AUD | Retail Sales M/M Oct | 4.90% | 2.50% | 1.30% | |

| 8:00 | CHF | GDP Q/Q Q3 | 1.80% | 1.80% | ||

| 9:00 | EUR | Eurozone M3 Money Supply Y/Y Oct | 7.40% | 7.40% |

{kind=link}