Dollar rebounds mildly entering into US session, as supported by surprisingly good jobless claims report. Risk-on rallies in the stock markets also losing some momentum, helps lift Yen mildly. As for the week so far, Aussie remains the best performer, followed by other commodity currencies. Swiss Franc and Yen are the worst ones. There’s still enough time to change the picture before weekly close tomorrow.

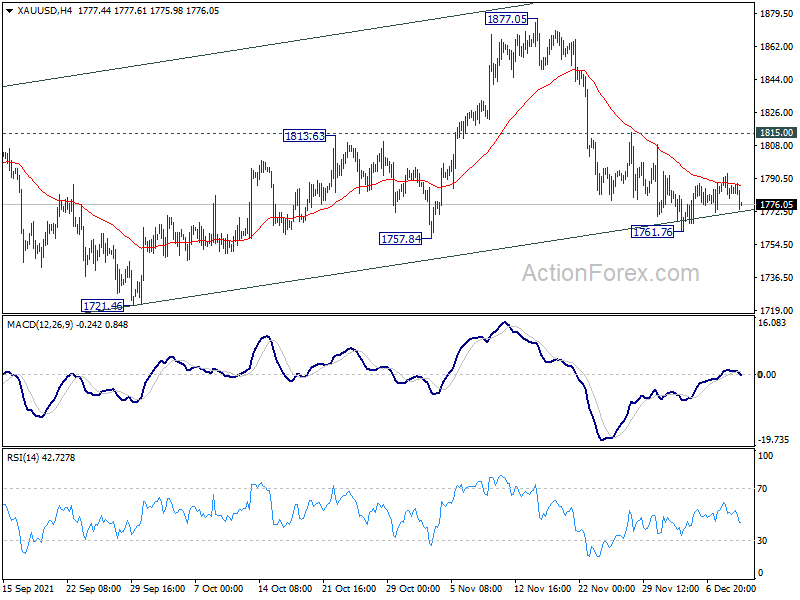

Technically, it could be about time Gold completes the consolidation pattern from 1761.76 temporary low, after touching 4 hour 55 EMA. Break of 1716.76 will resume the decline form 1877.05 to 1721.46 support next. Such development, if happens, could be accompanied by a near term comeback in Dollar.

In Europe, at the time of writing, FTSE is down -0.36%. DAX is down -0.39%. CAC is down -0.31%. Germany 10-year yield is down -0.042 at -0.353. Earlier in Asia, Nikkei dropped -0.47%. Hong Kong HSI rose 1.08%. China Shanghai SSE rose 0.98%. Singapore Strait Times rose 0.41%. Japan 10-year JGB yield rose 0.0008 to 0.050.

US initial jobless claims dropped to 184k, lowest since 1969

US initial jobless claims dropped -43k to 184k in the week ending December 4, much better than expectation of 225k. That’s also the lowest level since September 6, 1969. Four-week moving average of initial claims dropped -21k to 219k, lowest since March 7, 2020.

Continuing claims rose 38k to 1992k in the week ending November 27. Four-week moving average of continuing claims dropped -54k to 2028k, lowest since March 14, 2020.

Swiss SECO expects significant slowdown in winter period, lowers 2022 GDP growth forecast

SECO lowered Swiss GDP growth forecast for 2022 from 3.4% to 3.0%. GDP growth is projected to slow further to 2.0% in 2023, as the economy normalizes. 2021 GDP growth forecast is revised up slightly from 3.2% to 3.3%.

It said that “international supply and capacity bottlenecks are putting pressure on the industrial sector and causing sharp price increases globally”. Also, “uncertainty surrounding the pandemic has recently become strongly accentuated and several countries have stepped up their containment measures.”

SECO expects a “significant slowdown in economic growth globally and in Switzerland in the 2021/22 winter period”. But economy recovery is “not, however, expected to come to standstill in the medium term”.

Germany export rose 4.1% mom in Oct, imports rose 5.0% mom

In calendar and seasonally adjusted term, Germany export rose 4.1% mom to EUR 121.3B. Imports rose 5.0% mom to EUR 108.5B. Trade surplus narrowed to EUR 12.5B, down from EUR 13.2B, below expectation of EUR 12.9B. Over the year, exports rose 8.1% yoy, while imports rose 17.3% yoy.

In calendar and seasonally adjusted term, exports were 3.8% higher than pre-pandemic level in February 2020. Imports were 13.5% higher.

Japan business conditions improved sharply as led by non-manufacturers

According to the Japanese government’s Business Outlook Survey, conditions for all large corporations improved notably from 3.3 to 9.6 in Q4. That’s the second quarter of positive reading. Conditions for large non-manufacturing jumped sharply from 1.5 to 10.4. Meanwhile, conditions for large manufacturers improved slightly from 7.0 to 7.9.

Conditions for mid-sized companies also rose sharply from 0.2 to 10.7. Conditions for small companies rose from -18.0 to -3.0, but stayed negative for the 31st successive quarter.

“With the severe situation caused by the impact of virus infections gradually easing, the survey results showed that (the economy) has been picking up, although some fields remain weak,” a government official told reporters.

China CPI rose to 2.3% yoy in Nov, PPI slowed from 26-yr high to 12.6% yoy

China CPI accelerated to 2.3% yoy in November, up from 1.5% yoy, but below expectation of 2.5% yoy. That’s nonethless the highest level since August 2020. PPI slowed to 12.9% yoy, down from October’s 26-year high of 13.5% yoy, above expectation of 12.6%.

“As policies to stabilise prices and ensure supply have stepped up, the rapid surge in coal, metal and other energy and raw material prices has been initially contained, leading to a slowdown in PPI,” NBS senior statistician Dong Lijuan said in a statement accompanying the release.

New Zealand manufacturing sales dropped -2.2% qoq in Q3

New Zealand Manufacturing sales dropped -2.2% qoq, or NZD 674m in Q3. When adjusted for seasonal effects, 10 of the 13 manufacturing industries had lower volumes of sales in the quarter.

The largest industry movements were: metal products (-17%), petroleum and coal products (-13%), transport equipment, machinery, and equipment (-8.8%).

“Despite sales falls in several construction related manufacturing industries, increased prices for meat and dairy cushioned the blow for total manufacturing values,” business statistics manager Evie Rolinson-Purchase said.

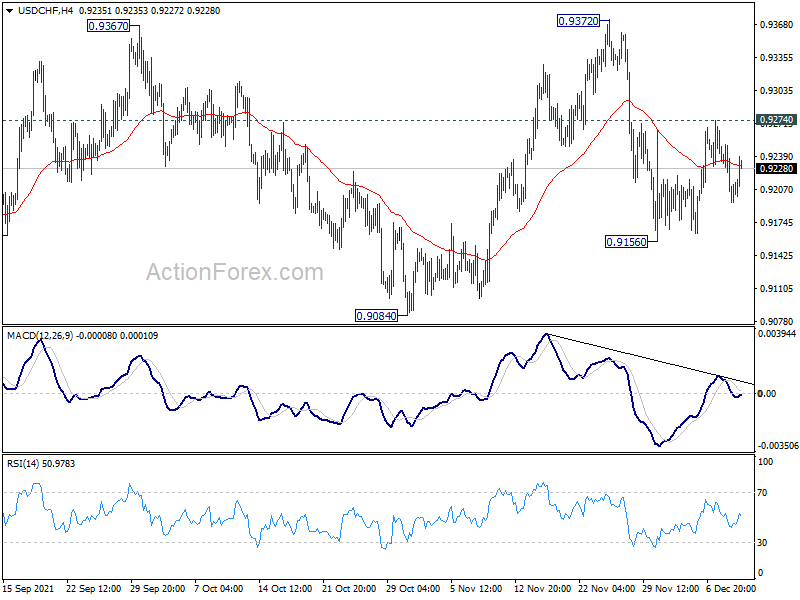

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9228; (P) 0.9251; (R1) 0.9272; More….

USD/CHF recovers mildly but stays below 0.9274 minor resistance. Intraday bias remains neutral first. On the upside, break of 0.9274 will suggest that the pull back from 0.9372 is finished. Intraday bias will be turned back to the upside for 0.9372. On the downside, below 0.9156 will target 0.9084 support. Firm break there should confirm that choppy rise from 0.8925 has completed, and suggests that fall from 0.9471 is resuming. Deeper decline would be seen through 0.8925.

In the bigger picture, the corrective structure of the rebound from 0.8925 argues that fall from 0.9471 is not complete yet. It could either be the second leg of pattern from 0.8756 (2021 low), or resuming larger down trend from 1.0237 (2018 high). We’d pay attention to the downside momentum and assess the odds later. But for now, medium term outlook will be neutral at best as long as 0.9471 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Manufacturing Sales Q3 | -2.20% | 4.20% | 3.90% | 3.70% |

| 23:50 | JPY | BSI Large Manufacturing Q3 | 7.9 | 5.3 | 7 | |

| 23:50 | JPY | Money Supply M2+CD Y/Y Nov | 4.00% | 4.40% | 4.20% | |

| 00:01 | GBP | RICS Housing Price Balance Nov | 71% | 72% | 70% | 71% |

| 00:30 | AUD | RBA Bulletin Q3 | ||||

| 01:30 | CNY | CPI Y/Y Nov | 2.30% | 2.50% | 1.50% | |

| 01:30 | CNY | PPI Y/Y Nov | 12.90% | 12.60% | 13.50% | |

| 06:00 | JPY | Machine Tool Orders Y/Y Nov | 64.00% | 81.50% | ||

| 07:00 | EUR | Germany Trade Balance (EUR)Oct | 12.5B | 12.9B | 13.2B | |

| 08:00 | CHF | SECO Economic Forecasts | ||||

| 13:30 | USD | Initial Jobless Claims (Dec 3) | 184K | 225K | 222K | 227K |

| 15:00 | USD | Wholesale Inventories Oct F | 2.20% | 2.20% | ||

| 15:30 | USD | Natural Gas Storage | -60B | -59B |

{kind=link}