Dollar is trading mixed in early US session after weaker than expected retail sales data. The greenback is extending recent rally against Canadian, but pulls back against Australian. European majors are mixed while Yen is also trading a touch weaker. Other markets are quite too with Gold’s selloff taking a breather at around 1770. Traders are holding their bets for now, awaiting FOMC decision on quickening the tapering pace, and new economic projections.

Technically, we’d monitor the actions in EUR/USD, GBP/USD, USD/CHF and USD/JPY together to confirm the moves of each other. To be specific, the ranges to breakout from are 1.1185/1.3820 in EUR/USD, 1.3158/1.3351 in GBP/USD, 0.9156/0.9372 in USD/CHF and 112.52/115.51 in USD/JPY.

In Europe, at the time of writing, FTSE is down -0.20%. DAX is up 0.39%. CAC is up 0.68%. Germany 10-year yield is up 0.0102 at -0.356. Earlier in Asia, Nikkei rose 0.10%. Hong Kong HSI dropped -0.91%. China Shanghai SSE dropped -0.38%. Japan 10-year JGB yield dropped -0.0010 to 0.049.

Some previews on FOMC:

- FOMC Preview – Fed to Double Size of QE Tapering

- Fed Meeting: Faster Taper Looms But What Will The Dot Plot Reveal?

- What To Expect From The Fed’s Final 2021 Meeting?

US retail sales rose 0.3% mom in Nov ex-auto sales up 0.3% mom

US retail sales rose 0.3% mom to USD 639.8B in November, below expectation of 0.8% mom. Ex-auto sales rose 0.3% mom, below expectation of 1.0% mom. Ex-gasoline sales rose 0.1% mom. Ex-auto, ex-gasoline sales rose 0.2% mom. Total sales for September through November period were up 16.2% yoy from the same period a year ago.

Also released, import price index rose 0.7% mom in November, matched expectations. Empire State Manufacturing index rose from 30.9 to 31.9 in December, above expectation of 27.0.

From Canada, CPI was unchanged at 4.7% yoy in November. CPI common rose from 1.8% Yoy to 1.9% yoy. CPI media dropped from 2.9% yoy to 2.8% yoy. CPI trimmed rose from 3.3% yoy to 3.4% yoy.

UK CPI rose to 5.1% yoy in Nov, highest since 2011

UK CPI accelerated further to 5.1% yoy in November, up from 4.2% yoy, above expectation of 4.7% yoy. That’s also the highest level since September 2011, when it stood at 5.2%. CPI core rose to 4.0% yoy, up from 3.4% yoy, above expectation of 3.8% yoy.

PPI input rose from 13.7% yoy to 14.3% yoy, above expectation of 11.0% yoy. PPI output rose from 8.6% yoy to 9.1% yoy, above expectation of 7.3% yoy. PPI core output also rose from 7.1% to 7.9%, above expectation of 7.1% yoy.

ONS Chief Economist Grant Fitzner said: “A wide range of price rises contributed to another steep rise in inflation, which now stands at its highest rate for over a decade. The price of fuel increased notably, pushing average petrol prices higher than we have seen before. Clothing costs – which increased after falling this time last year – along with prices for good, second-hand cars and increased tobacco duty all helped drive up inflation this month.”

“The costs of goods produced by factories and the price of raw materials have continued to increased significantly to their highest rate for at least twelve years.”

Australia Westpac consumer sentiment dropped to 104.3, different responses between states

Australia Westpac-Melbourne Institute consumer sentiment dropped -1.0% to 104.3 in December, staying in positive territory where optimists outnumber pessimists. Nevertheless, responses from states are rather different, with both NSW and Victoria posted significant falls (down 3.6% and 3.5% respectively) while sentiment was up in Queensland (3.4%), WA (3.2%) and SA (7.1%).

Westpac added that RBA’s meeting on February 1 will be a very important one with new economic forecasts. No action or commitment on interest rate is expected at the meeting yet. But RBA would lower the bond purchase pace from AUD 4B per week to AUD 2B per week.

BoJ Kuroda: Consumer inflation will approach target through various channels

BoJ Governor Haruhiko Kuroda told parliament today, “it’s true there’s a chance consumer inflation will approach 2% through various channels.”

“But what’s desirable is for the economy to recover steadily and push up corporate profits, thereby leading to higher wages and inflation,” he added. “We’ll patiently maintain ultra-easy policy to achieve this at the earliest date possible.”

Kuroda also said Japan is not in a state of “stagflation”.

China industrial production rose 3.8% yoy in Nov, retail sales rose 3.9% yoy

China industrial production rose 3.8% yoy in November, matched expectations. That’s a slightly faster growth rate than October’s 3.5% yoy. Retail sales rose 3.9% yoy, below expectation of 4.9% yoy, and slowed from prior month’s 4.9% yoy. Fixed asset investment rose 5.2% ytd yoy, slightly below expectation of 5.3%.

“Generally speaking, the national economy maintained the recovery momentum in November, and the major macro indicators stayed within a reasonable range,” the NBS said in its statement. “However, we must note that the international environment is increasingly complex and severe, and there are still many constraints on the domestic economic recovery.”

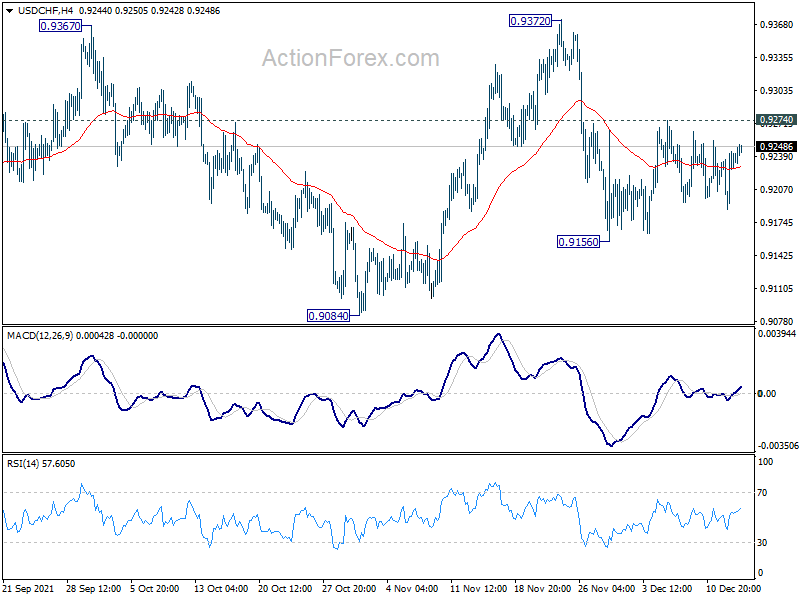

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9206; (P) 0.9225; (R1) 0.9262; More….

Outlook in USD/CHF remains unchanged as range trading continues. Intraday bias stays neutral. On the upside, break of 0.9274 will suggest that the pull back from 0.9372 is finished. Intraday bias will be turned back to the upside for 0.9372. On the downside, below 0.9156 will target 0.9084 support. Firm break there should confirm that choppy rise from 0.8925 has completed, and suggests that fall from 0.9471 is resuming. Deeper decline would be seen through 0.8925.

In the bigger picture, the corrective structure of the rebound from 0.8925 argues that fall from 0.9471 is not complete yet. It could either be the second leg of pattern from 0.8756 (2021 low), or resuming larger down trend from 1.0237 (2018 high). We’d pay attention to the downside momentum and assess the odds later. But for now, medium term outlook will be neutral at best as long as 0.9471 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Current Account (NZD) Q3 | -8.30B | -8.02B | -1.40B | -1.54B |

| 23:30 | AUD | Westpac Consumer Confidence Dec | -1.00% | 0.60% | ||

| 02:00 | CNY | Retail Sales Y/Y Nov | 3.90% | 4.90% | 4.90% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Nov | 5.20% | 5.30% | 6.10% | |

| 02:00 | CNY | Industrial Production Y/Y Nov | 3.80% | 3.80% | 3.50% | |

| 04:30 | JPY | Tertiary Industry Index M/M Oct | 1.50% | 1.20% | 0.50% | |

| 07:00 | GBP | CPI M/M Nov | 0.70% | 0.50% | 1.10% | |

| 07:00 | GBP | CPI Y/Y Nov | 5.10% | 4.70% | 4.20% | |

| 07:00 | GBP | Core CPI Y/Y Nov | 4.00% | 3.80% | 3.40% | |

| 07:00 | GBP | RPI M/M Nov | 0.70% | 0.30% | 1.10% | |

| 07:00 | GBP | RPI Y/Y Nov | 7.10% | 6.70% | 6.00% | |

| 07:00 | GBP | PPI Input M/M Nov | 1.00% | 1.10% | 1.40% | 1.60% |

| 07:00 | GBP | PPI Input Y/Y Nov | 14.30% | 11% | 13% | 13.70% |

| 07:00 | GBP | PPI Output M/M Nov | 0.90% | 0.80% | 1.10% | 1.50% |

| 07:00 | GBP | PPI Output Y/Y Nov | 9.10% | 7.30% | 8.00% | 8.60% |

| 07:00 | GBP | PPI Core Output M/M Nov | 0.80% | 0.40% | 0.70% | 1.20% |

| 07:00 | GBP | PPI Core Output Y/Y Nov | 7.90% | 7.10% | 6.50% | 7.10% |

| 13:15 | CAD | Housing Starts Y/Y Nov | 301K | 240.0K | 236.6K | 238K |

| 13:30 | CAD | Manufacturing Sales M/M Oct | 4.30% | 4.00% | -3.00% | |

| 13:30 | CAD | CPI M/M Nov | 0.30% | 0.20% | 0.70% | |

| 13:30 | CAD | CPI Y/Y Nov | 4.70% | 4.80% | 4.70% | |

| 13:30 | CAD | CPI Common Y/Y Nov | 2.00% | 1.90% | 1.80% | |

| 13:30 | CAD | CPI Median Y/Y Nov | 2.80% | 2.90% | 2.90% | |

| 13:30 | CAD | CPI Trimmed Y/Y Nov | 3.40% | 3.30% | 3.30% | |

| 13:30 | USD | Empire State Manufacturing Index Dec | 31.9 | 27 | 30.9 | |

| 13:30 | USD | Retail Sales M/M Nov | 0.30% | 0.80% | 1.70% | |

| 13:30 | USD | Retail Sales ex Autos M/M Nov | 0.30% | 1.00% | 1.70% | |

| 13:30 | USD | Import Price Index M/M Nov | 0.70% | 0.70% | 1.20% | |

| 15:00 | USD | Business Inventories Oct | 0.90% | 0.70% | ||

| 15:00 | USD | NAHB Housing Market Index Dec | 83 | 83 | ||

| 15:30 | USD | Crude Oil Inventories | -1.8M | -0.2M | ||

| 19:00 | USD | Fed Interest Rate Decision | 0.25% | 0.25% | ||

| 19:30 | USD | FOMC Press Conference |

{kind=link}