While US stocks staged a strong rally overnight, Asian markets turned mixed. Investors are holding their bets ahead of US CPI data. Australian Dollar remains the strongest one for the week, followed by Kiwi. Loonie also regained some ground with help from the stabilization in oil prices. On the other hand, Yen is currently the worst performing one, followed by Euro and then Dollar.

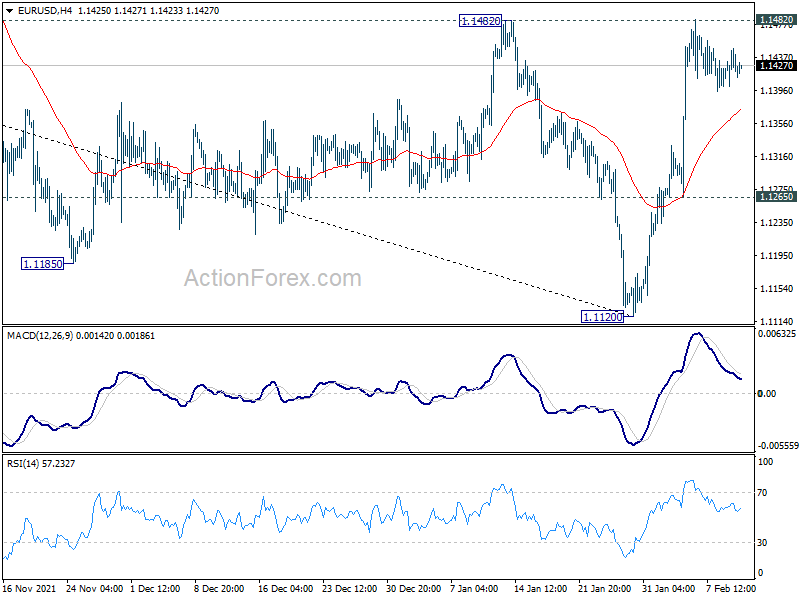

Technically, major focus remains on 1.1482 resistance in EUR/USD. Firm break there will add to the case of bullish trend reversal. At the same time, if that happens, attention will be paid on whether it’s more of a return to strength in Euro, or weakness in Dollar. Sterling could be used as a gauge. Break of 1.3627 resistance in GBP/USD will be a sign of Dollar weakness. Break of 0.8476 resistance in EUR/GBP will be a sign of Euro strength. But of course, both could happen at the same time.

In Asia, Nikkei closed up 0.30%. Hong Kong HSI is down -0.33%. China Shanghai SSE is down -0.36%. Singapore Strait Times is down -0.02%. Japan 10-year JGB yield is up 0.0185 at 0.227. Overnight, DOW rose 0.86%. S&P 500 rose 1.45%. NASDAQ rose 2.08%. 10-year yield dropped -0.025 to 1.929.

Fed Mester: No compelling case to start with 50bps hike

Cleveland Fed President Loretta Mester “each meeting is going to be in play” regarding interest rate decisions. She added, “we’re going to assess conditions, we’re going to assess how the economy’s evolving, we’re going to be looking at the risks, and we’re going to be removing accommodation.”

On the idea of a 50bps rate hike in March, Mester said “I don’t like taking anything off the table.” However, “I don’t think there’s any compelling case to start with a 50 basis point”.

“Again, we’ve got to be a little bit careful. Even though you can well telegraph what’s coming, when you take that first action, there’s going to be a reaction,” she added.

On the topic of balance sheet runoff, Mester said, “I would support selling some of our mortgage-backed securities at some point during the reduction period to speed the conversion of our portfolio’s composition to primarily Treasuries.”

BoC Macklem: We signalled with unusual clarity a rising path for interest rates

In a speech, BoC Governor Tiff Macklem said current inflation, close to 5%, is “too high”. But that is “not the result of generalized excess demand in the Canadian economy”. Inflation “largely reflects global supply problems, most of which stem from the pandemic”. As the pandemic recedes, “conditions around the world should normalize, taking pressure off global goods prices.”. BoC expects inflation to “come down relatively quickly” in H2 2022 to 3% by the end of the year.

Macklem added, “to get inflation the rest of the way back to its 2% target, we need a significant shift in monetary policy”. The economy will need “higher interest rates to moderate growth in spending and bring demand in line with supply”, and “keep inflation expectations well anchored”. And, “we signalled with unusual clarity that Canadians should expect a rising path for interest rates.”

Japan CGPI rose 8.6% yoy in Jan, index at highest since 1985

Japan corporate goods price index rose 8.6% yoy in January, slowed slightly from December’s 8.7% yoy, but beat expectation of 8.2% yoy. At 109.5, the index was at the highest level since September 1985.

Export prices jumped 12.5% yoy on Yen basis, 6.6% yoy on contract currency basis. Import prices surged a massive 37.5% yoy on Yen basis, and 28.0% yoy on contract currency basis.

However, consumer prices remained sluggish, with national CPI core at 0.5% yoy in December, which some economists expected to slow to 0.3% yoy in January.

BoJ officials, including Governor Haruhiko Kuroda, have indicated that it would be hard to see consumer inflation to sustainably reach 2% target without wages rise.

Elsewhere

Australia consumer inflation expectations rose further to 4.6% in February, up from 4.4%. UK RICS house price balance rose from 69 to 74, above expectation of 72.

Looking ahead, US CPI will be the major focus of the day. Jobless claims will be released as usual on a Tuesday.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1402; (P) 1.1425; (R1) 1.1447; More…

EUR/USD is still staying in consolidation in tight range and intraday bias remains neutral. As noted before, a medium term bottom could be in place at 1.1120, on bullish convergence condition in daily MACD. Break of 1.1482 resistance will target 38.2% retracement of 1.2348 to 1.1120 at 1.1589 next. Sustained break there will argue that whole fall from 1.2348 has completed too and target 61.8% retracement at 1.1879. On the down, however, break of 1.1265 support will dampen this bullish view and bring retest of 1.1120 low instead.

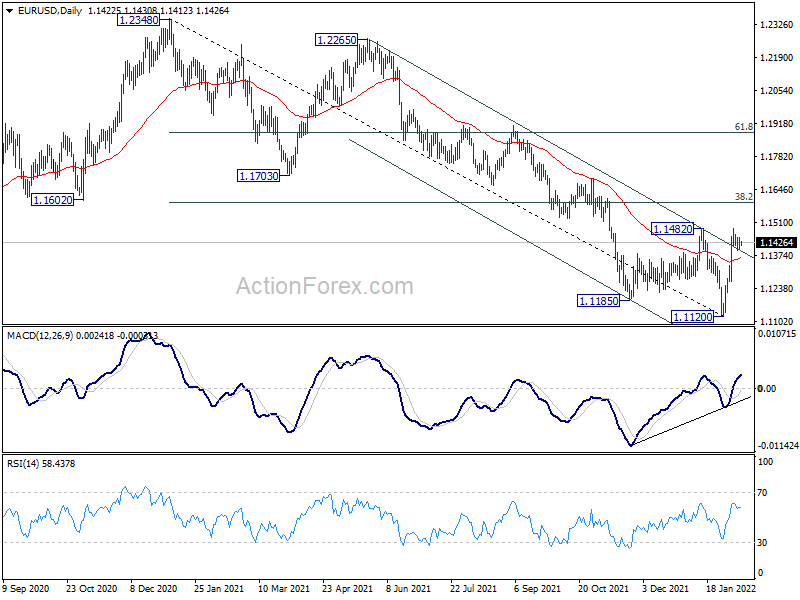

In the bigger picture, the decline from 1.2348 (2021 high) is seen as a leg inside the range pattern from 1.2555 (2018 high). Sustained trading above 55 week EMA (now at 1.1613) will argue that it has completed and stronger rise would be seen back towards top of the range between 1.2348 and 1.2555. However, firm break of 1.0635 (2020 low) will raise the chance of long term down trend resumption and target a retest on 1.0339 (2017 low) next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | PPI Y/Y Jan | 8.60% | 8.20% | 8.50% | 8.70% |

| 00:00 | AUD | Consumer Inflation Expectations Feb | 4.60% | 4.40% | ||

| 00:01 | GBP | RICS Housing Price Balance Jan | 74% | 72% | 69% | |

| 13:30 | USD | Initial Jobless Claims (Feb 4) | 230K | 238K | ||

| 13:30 | USD | CPI M/M Jan | 0.40% | 0.50% | ||

| 13:30 | USD | CPI Y/Y Jan | 7.30% | 7.00% | ||

| 13:30 | USD | CPI Core M/M Jan | 0.50% | 0.60% | ||

| 13:30 | USD | CPI Core Y/Y Jan | 5.90% | 5.50% |

{kind=link}