Euro is staying under selling pressure as Russia is continuing its invasion while Ukrainians are holding on defending their country. But selloff in Sterling has eased a little bit. Australia Dollar is extending recent rally as the best performer for the week. Canadian Dollar is following closely with help from BoC’s rate hike overnight, and persistent rally in oil prices. Dollar and Yen are mixed while Swiss Franc upside momentum diminished slightly.

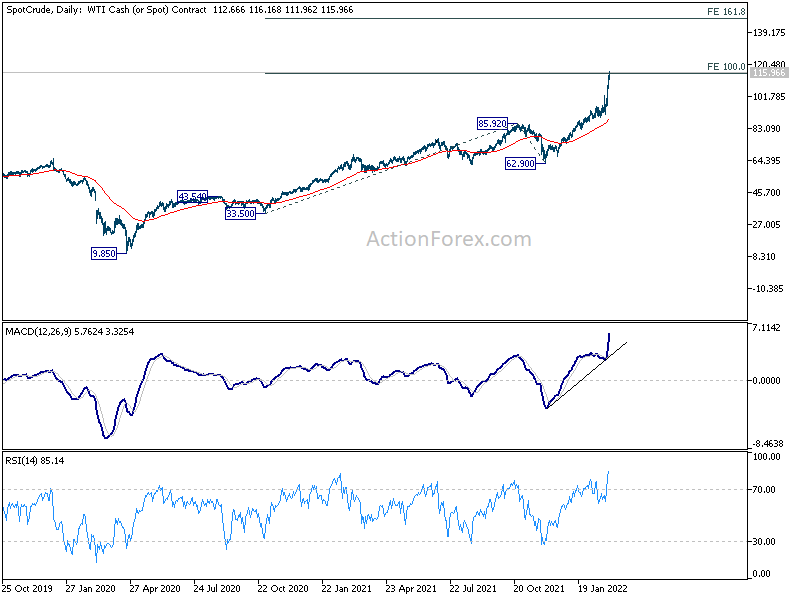

Technically, WTI crude oil has met first medium term target of 100% projection of 33.50 to 85.92 from 62.90 at 115.32 already and there is no sign of stopping yet. It should be noted again that fear-driven moves in commodity markets could be extremely powerful. A clear example was the negative oil price at the start of the pandemic less than two years ago. Sustained break above 115.32 could prompt even more upside acceleration to 161.8% projection at 147.71, in rather quick manner. The implication on inflation, monetary policy, stocks, yields and FX would be rather complicated.

In Asia, at the time of writing, Nikkei is up 0.79%. Hong Kong HSI is up 0.46%. China Shanghai SSE is down -0.20%. Singapore Strait Times is up 0.80%. Japan 10-year JGB yield is up 0.0343 at 0.168. Overnight, DOW rose 1.79%. S&P 500 rose 1.86%. NASDAQ rose 1.62%. 10-year yield rose 0.158 to 1.865.

Fed Powell to Congress: Appropriate to raise interest rate later this month

In the semiannual testimony to Congress yesterday, Fed Chair Jerome Powell said,”with inflation well above 2 percent and a strong labor market, we expect it will be appropriate to raise the target range for the federal funds rate at our meeting later this month.”

He reiterated that “federal funds rate is our primary means of adjusting the stance of monetary policy”. And, “reducing our balance sheet will commence after the process of raising interest rates has begun, and will proceed in a predictable manner primarily through adjustments to reinvestments.

Powell also said, “the near-term effects on the U.S. economy of the invasion of Ukraine, the ongoing war, the sanctions, and of events to come, remain highly uncertain. Making appropriate monetary policy in this environment requires a recognition that the economy evolves in unexpected ways. We will need to be nimble in responding to incoming data and the evolving outlook.”

BoE Tenreyro: Russia invasion will intensify trade shock and inflation

Referring to Russia invasion of Ukraine, BoE MPC member Silvana Tenreyro said yesterday, “recent developments will intensify the terms of trade shock that we were already experiencing, so will push up inflation and have a negative impact on activity. How exactly? That’s the job we will start next week.”

Tenreyro added that she had been surprised by the scale of wages growth. However, “when you are talking about spirals, you are talking about explosive dynamics which we haven’t seen yet. If anything, we are just starting the first round, so how can you talk about second round (effects)” she said.

BoE Cunliffe: Recent events led to abrupt shift in expectations

BoE Deputy Governor Jon Cunliffe said yesterday, “the events of the last few days have led to an abrupt shift in our expectations of the future and an increase in uncertainty.”

“The heightened perception of geopolitical risks, and the potential impacts on growth and inflation, can only increase risks around the adjustment away from riskier assets that is already underway,” he said.

Cunliffe added, “Russia is a relatively small part of the world economy, accounting for around 2% of world GDP. It accounts however for a much larger share of the world supply of energy and other commodities.”

BoJ Nakagawa: Core inflation may briefly hit 2% on energy, food and industrial goods

BoJ board member Junko Nakagawa said “for the time being, inflationary pressure will remain strong, mainly for energy, food and industrial goods.” Core consumer prices may “briefly rise close to 2%.”

However, “even if that happens, what’s important is to scrutinise the factors and whether Japan’s economic fundamentals are strong enough to make such price rises sustainable,” she said.

“Global financial markets remain jittery due to escalating tensions in Ukraine. We’re monitoring changes in developments carefully,” she added.

China Caixin PMI composite unchanged at 50.1, still under triple pressure

China Caixin PMI Services dropped from 51.4 to 50.2 in February. PMI Composite was unchanged at 50.1.

Wang Zhe, Senior Economist at Caixin Insight Group said: “Overall, the manufacturing PMI rose in February, while the services PMI fell, but both remained in positive territory. Demand in the manufacturing sector improved, while demand in the services sector was greatly affected by the epidemic….

“Under the “triple pressure” of demand contraction, supply shocks and weakening expectations, the economy’s recovery is still not robust. Stabilizing economic growth remains an important focus of the government.”

Elsewhere

Australia AiG Performance of Construction rose from 45.9 to 53.4 in February. Building permits dropped -27.9% mom in January, versus expectation of -3.0% mom. Trade surplus widened to AUD 12.89B, above expectation of AUD 9.1B.

Looking ahead, ECB will publish monetary policy meeting accounts. Eurozone will release PMI services final, unemployment rate and PPI. UK will release PMI services final. Swiss will release CPI.

Later in the day, US will release jobless claims, ISM services and factory orders.

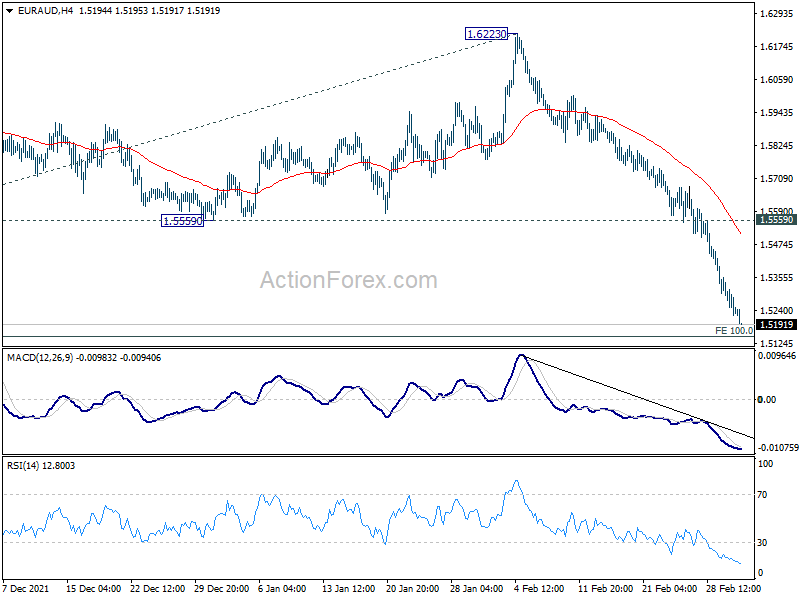

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5201; (P) 1.5272; (R1) 1.5317; More…

EUR/AUD’s fall continues today and break of 1.5250 low indicates resumption of larger down trend from 1.9799. Intraday bias stays on the downside for 100% projection of 1.6343 to 1.5354 from 1.6223 at 1.5143. Sustained break there will pave the way to 161.8% projection at 1.4476. On the upside, break of 1.5559 support turned resistance is needed to indicate short term bottoming. Otherwise, outlook stays bearish in case of recovery.

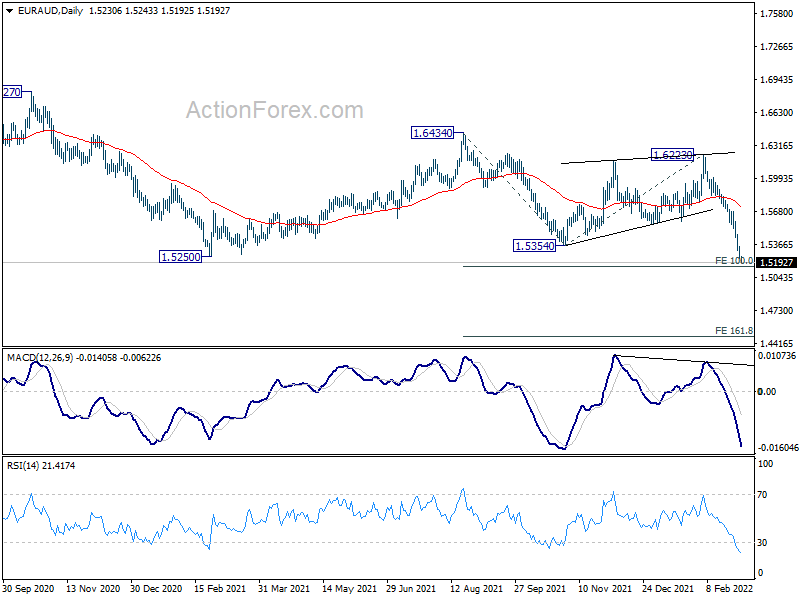

In the bigger picture, break of 1.5250 support indicates resumption of whole down trend from 1.9799 (2020 high). Next target is 61.8% retracement of 1.1602 (2012 low) to 1.9799 at 1.4733 and below. But we’d tentatively look for bottoming sign above 1.3624 long term support, for an interim rebound. Meanwhile, break of 1.6223 resistance is now needed to indicate medium term bottoming. Otherwise, outlook will remain bearish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Construction Index Feb | 53.4 | 45.9 | ||

| 00:30 | AUD | Building Permits M/M Jan | -27.90% | -3.00% | 8.20% | 9.80% |

| 00:30 | AUD | Trade Balance (AUD) Jan | 12.89B | 9.10B | 8.36B | 8.82B |

| 01:45 | CNY | Caixin Services PMI Feb | 50.2 | 50.9 | 51.4 | |

| 05:00 | JPY | Consumer Confidence Index Feb | 35.3 | 35 | 36.7 | |

| 07:30 | CHF | CPI M/M Feb | 0.30% | 0.20% | ||

| 07:30 | CHF | CPI Y/Y Feb | 1.80% | 1.60% | ||

| 08:45 | EUR | Italy Services PMI Feb | 48.9 | 48.5 | ||

| 08:50 | EUR | France Services PMI Feb F | 57.9 | 57.9 | ||

| 08:55 | EUR | Germany Services PMI Feb F | 56.6 | 56.6 | ||

| 09:00 | EUR | Eurozone Services PMI Feb F | 55.8 | 55.8 | ||

| 09:00 | EUR | Italy Unemployment Jan | 9.10% | 9.00% | ||

| 09:30 | GBP | Services PMI Feb F | 60.8 | 60.8 | ||

| 10:00 | EUR | Eurozone Unemployment Rate Jan | 6.90% | 7.00% | ||

| 10:00 | EUR | Eurozone PPI M/M Jan | 3.00% | 2.90% | ||

| 10:00 | EUR | Eurozone PPI Y/Y Jan | 26.90% | 26.20% | ||

| 12:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 12:30 | USD | Challenger Job Cuts Y/Y Feb | -76.00% | |||

| 13:30 | USD | Initial Jobless Claims (Feb 25) | 235K | 232K | ||

| 13:30 | USD | Unit Labor Costs Q4 | 0.40% | 0.30% | ||

| 13:30 | USD | Nonfarm Productivity Q4 | 6.50% | 6.60% | ||

| 14:45 | USD | Services PMI Feb F | 56.7 | 56.7 | ||

| 15:00 | USD | ISM Services PMI Feb | 60.5 | 59.9 | ||

| 15:00 | USD | ISM Services Prices Paid Feb | 82.3 | |||

| 15:00 | USD | ISM Services Employment Index Feb | 52.3 | |||

| 15:00 | USD | Factory Orders M/M Jan | 0.50% | -0.40% | ||

| 15:30 | USD | Natural Gas Storage | -138B | -129B |

{kind=link}