Major Asia indexes trade mildly higher today but the forex markets are quiet. Trading will likely be subdued ahead with Swiss, France and Germany on bank holiday, while the US economic calendar is empty. But an eventful week will kick start with RBA rate decision tomorrow, followed by ECB on Thursday. Then the week would likely end on a strong note, in terms of volatility, with US CPI and Canada employment on Friday.

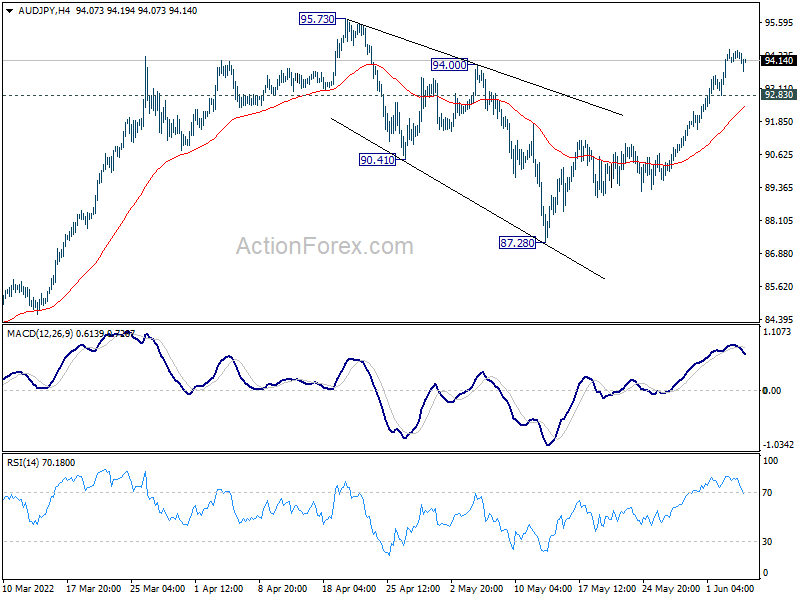

Technically, AUD/JPY is a pair to watch for the next 24-hours. Currently, considering broad based weakness in Yen, the favored view is that correction from 95.73 has completed with three waves down to 87.28. Medium term up trend should be ready resume. Further rise is expected as long as 92.83 minor support holds and break of 95.73 high will confirm this bullish case. However, should RBA disappoint by delivering less than a 40bps hike, AUD/JPY could break through 92.83 to extend the corrective pattern from 95.73 with another falling leg.

In Asia, at the time of writing, Nikkei is up 0.75%. Hong Kong HSI is up 1.32%. Chinas Shanghai SSE is up 0.89%. Singapore Strait Times is down -0.18%. Japan 10-year JGB yield is up 0.0054 at 0.242.

Kuroda: BoJ takes a strong stance on continuing with monetary easing

BoJ Governor Haruhiko Kuroda said in a speech that the economy is “still on its way to recovery from the pandemic and has been under downward pressure from the income side due to rising commodity prices”. In this situation, “monetary tightening is not at all a suitable measure”.

He added that the top priority is to “persistently continue with the current aggressive monetary easing centered on yield curve control”. And, unlike other central banks, BoJ has noted faced the “the trade-off between economic stability and price stability”. Hence, it’s “certainly possible for the Bank to continue stimulating aggregate demand from the financial side.”

He concluded that BoJ “will take a strong stance on continuing with monetary easing, in that it will provide a macroeconomic environment where wages are likely to increase so that the rise in inflation expectations and changes in the tolerance of price rises — which have started to be seen recently — will lead to sustained inflation.”

China Caixin PMI services rose to 41.4 in May, composite rose to 42.2

China Caixin PMI Services rose form 36.2 to 41.4 in May, but missed expectation of 47.3. Caixin said services activity fell at softer, but still sharp rate amid COVID-19 restrictions. Drop in overall new work moderated. Input cost inflation eased to nine-month low. PMI Composite rose from 37.2 to 42.2.

Wang Zhe, Senior Economist at Caixin Insight Group said: “Overall, in May, local Covid outbreaks continued and manufacturing and services activity improved slightly, but continued to contract, with services hit harder. Demand was slightly stronger than supply. The fallout from the epidemic on market supply and demand has been transmitted to the labor market, which is deteriorating at a faster pace in both the manufacturing and services sectors. Disrupted supply chains and longer logistics delivery times have yet to improve. Businesses remained under great cost pressure.”

RBA to hike again, ECB to end net asset purchases

Two central banks will meet this week. RBA is expected to raise the target by 40bps to 0.75%. But a small increase of 25bps cannot be ruled, and it would be a disappointment to Aussie bulls should that happen. Additional, RBA would maintain hawkish bias and indicates that more tightening is underway.

ECB officials, including President Christine Lagarde, have set up market expectations for a July rate hike. To do that, it should announce the end of the asset purchase program at the upcoming meeting. There is no consensus on the size of hike in July, with some preferring 50bps and some not. The post meeting press conference will be scrutinized for hints on the hawk/dove balance in the Governing Council.

On the data front, US CPI will be the biggest event. Still there are other data to watch including Eurozone Sentix, China trade balance, as well as Canada employment. Here are some highlights for the week:

- Monday: Australia MI inflation gauge; China Caixin PMI services.

- Tuesday: Australia AiG Services, RBA rate decision; Japan average cash earnings, household spending, leading indicators; Germany factory orders; Swiss foreign currency reserves; Eurozone Sentix investor confidence; UK PMI services final; Canada trade balance, Ivey PMI; US trade balance.

- Wednesday: Japan GDP final, current account, bank lending; Swiss unemployment rate; Germany industrial production; France trade balance; Italy retail sales; UK PMI construction; Eurozone GDP revision; US wholesale inventories final.

- Thursday: UK RICS house price balance; Japan M2, machine tool orders; China trade balance; ECB rate decision; US jobless claims.

- Friday: Japan PPI; China CPI, PPI; Italy industrial production; Canada employment ; US CPI, U of Michigan consumer sentiment.

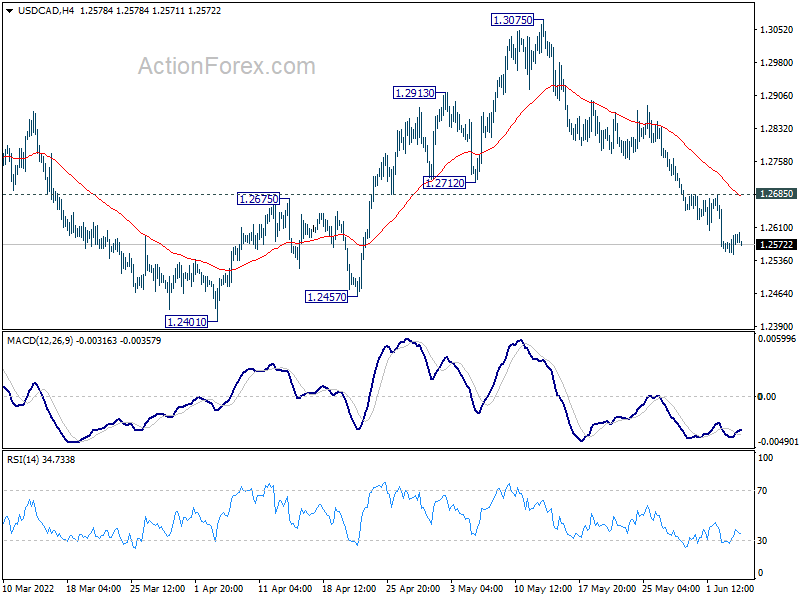

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2563; (P) 1.2584; (R1) 1.2616; More…

USD/CAD is losing some downside momentum again as seen in 4 hour MACD. But further fall is expected with 1.2685 resistance intact, towards 1.2401 support. Decisive break there will argue that whole rebound from 1.2005 has completed, after rejection by 1.3022 fibonacci resistance. Deeper fall would then be seen to retest this low. On the upside, above 1.2685 minor resistance will mix up the near term outlook and turn intraday bias neutral first.

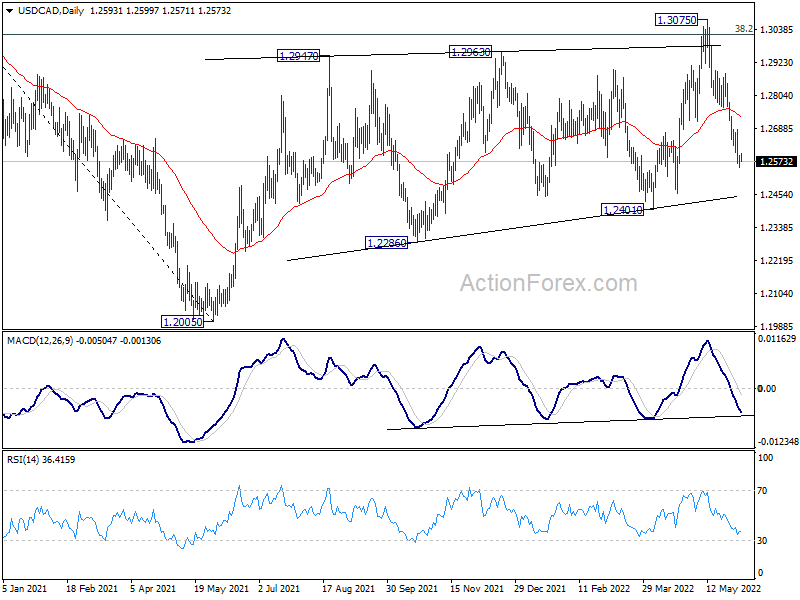

In the bigger picture, focus stays on 38.2% retracement of 1.4667 (2020 high) to 1.2005 (2021 low) at 1.3022. Sustained break there should confirm that the down trend from 1.4667 has completed after defending 1.2061 long term cluster support. Further rise would then be seen towards 61.8% retracement at 1.3650. However, rejection by 1.3022 will maintain medium term bearishness. Break of 1.2005 will resume the down trend from 1.4667 and that carries larger bearish implications too.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:00 | AUD | TD Securities Inflation M/M May | 1.10% | -0.10% | ||

| 01:45 | CNY | Caixin Services PMI May | 41.4 | 47.3 | 36.2 |

{kind=link}