The markets are relatively quiet in Asia today. Yen is steady after BoJ stands pat as widely expected. Yet, there is some upside prospect for Yen if global benchmark yields continue to correct lower. Dollar remains the worst performer and today’s PCE inflation data is unlikely to save it. Traders would more likely look beyond the data to next week’s FOMC decision and guidance. There is so far no extended selloff in Euro after the post-ECB dip. Commodity currencies are firmer but lack follow through buying too.

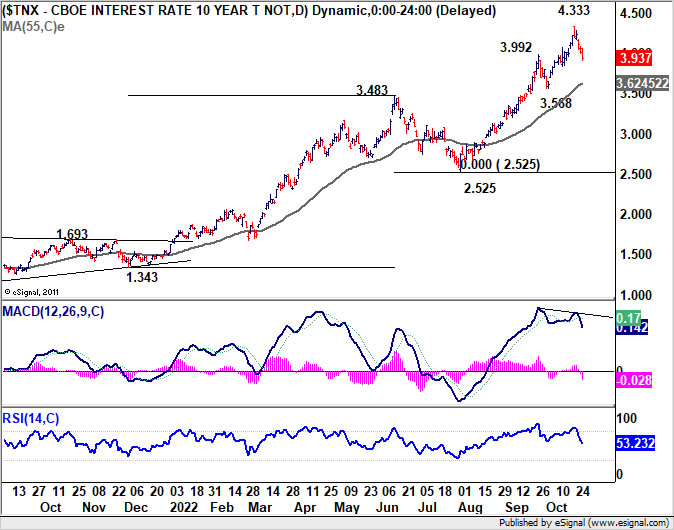

Technically, US 10-year yield’s close below 3.992 resistance turned support argues that it’s already correcting the rise from 2.525 to 4.333. There is prospect of deeper pull back towards 55 day EMA (now at 3.624). If happens, that could help drag down Yen pairs, in particular USD/JPY towards 55 day EMA (now at 143.52).

In Asia, at the time of writing, Nikkei is down -0.77%. Hong Kong HSI is down -2.73%. China Shanghai SSE is down -1.25%. Singapore Strait Times is up 1.64%. Japan 10-year JGB yield is down -0.0116 at 0.242. Overnight, DOW rose 0.61%. S&P 500 dropped -0.61%. NASDAQ dropped -1.63%. 10-year yield dropped -0.078 to 3.937.

BoJ stands pat, maintains yield cap at 0.25%

BoJ left monetary policy unchanged as widely expected. Under the yield curve control framework, short-term policy interest rate is held at -0.10%. 10-year JGB yield is kept at around 0%, with bond purchases without upper limit. 0.25% fixed rate purchase operation will continue to be held to cap 10-year JGB yield. The decision was unanimous.

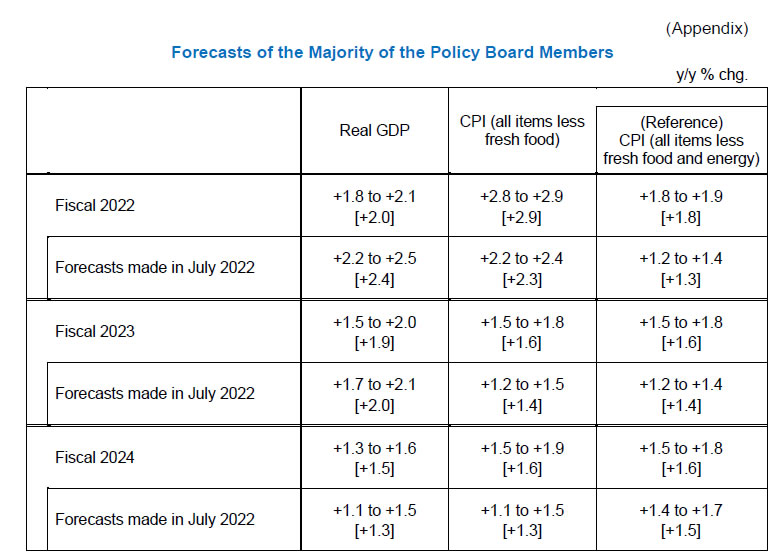

In the new economic projections:

- Fiscal 2022 GDP growth forecast was downgraded from 2.4% to 2.0%.

- Fiscal 2023 GDP growth forecast was downgraded from 2.0% to 1.9%.

- Fiscal 2024 GDP growth forecast was upgraded from 1.3% to 1.5%.

- Fiscal 2022 CPI core forecast was upgraded from 2.3% to 2.9%.

- Fiscal 2023 CPI core forecast was upgraded from 1.4% to 1.6%.

- Fiscal 2024 CPI core forecast was upgraded from 1.3% to 1.6%.

- Fiscal 2022 CPI core-core forecast was upgraded from 1.3% to 1.8%.

- Fiscal 2023 CPI core-core forecast was upgraded from 1.4% to 1.6%.

- Fiscal 2024 CPI core-core forecast was upgraded from 1.5% to 1.6%.

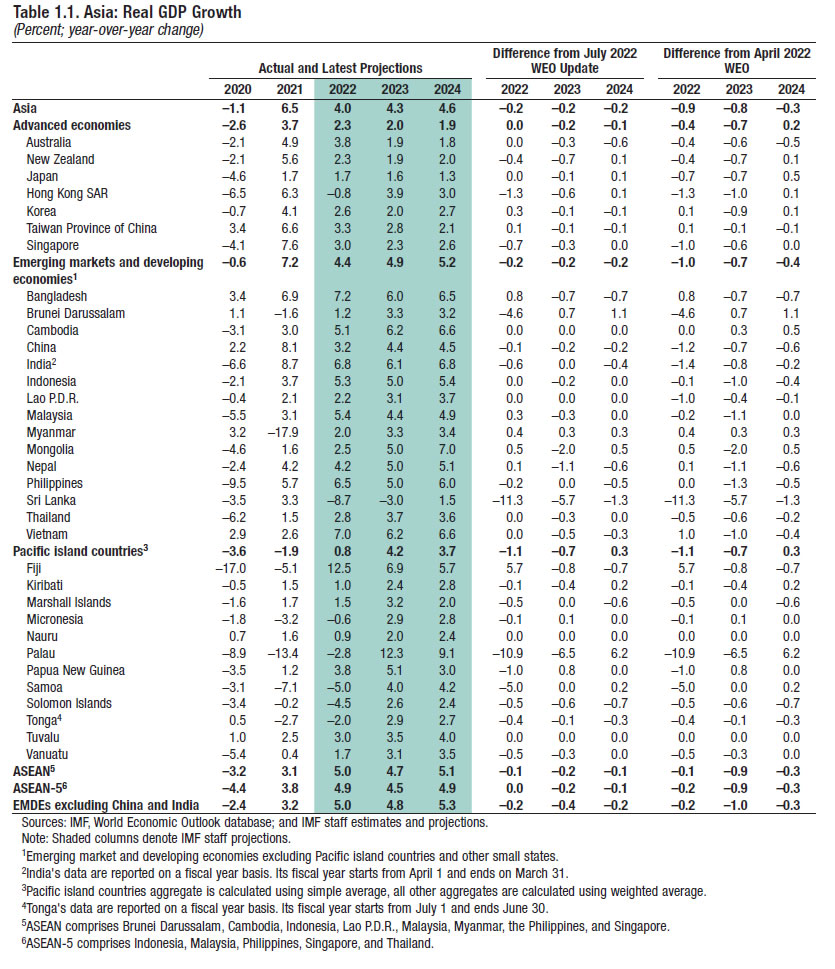

IMF cut Asia growth forecasts to 4% in 2022, 4.3% in 2023

IMF lowered Asia’s growth forecast in to 4.0% in 2022, 4.3% in 2023, and 4.6% in 2024. Japan’s growth forecast was held unchanged at 1.7% in 2022, downgraded slightly to 1.6% in 2023, and raised to 1.3% in 2024. For China, growth forecasts was downgraded to 3.2% in 2022, 4.4% in 2023, and 4.5% in 2024.

“As the effects of the pandemic wane, the region faces new headwinds from global financial tightening and an expected slowdown of external demand,” the report said.

As for China, “with a growing number of property developers defaulting on their debt over the past year, the sector’s access to market financing has become increasingly challenging,” the report noted.”Risks to the banking system from the real estate sector are rising because of substantial exposure.”

Elsewhere

Japan Tokyo CPI core rose from 2.8% yoy to 3.4% yoy in October, above expectation of 3.2% yoy. Unemployment rate ticked up from 2.5% to 2.6% in September, above expectation of 2.5% yoy.

Australia PPI rose 1.9% qoq, 6.4% yoy in Q3, versus expectation of 1.5% qoq, 6.4% yoy.

Looking ahead, GDP from France, and GErmany will be the main focus in Euroepan session. Eurozone economic sentiment, Germany CPI flash and Swiss KOF will be featured too.

Later in the day, US personal income and spending, with PCE inflation will be the main feature.

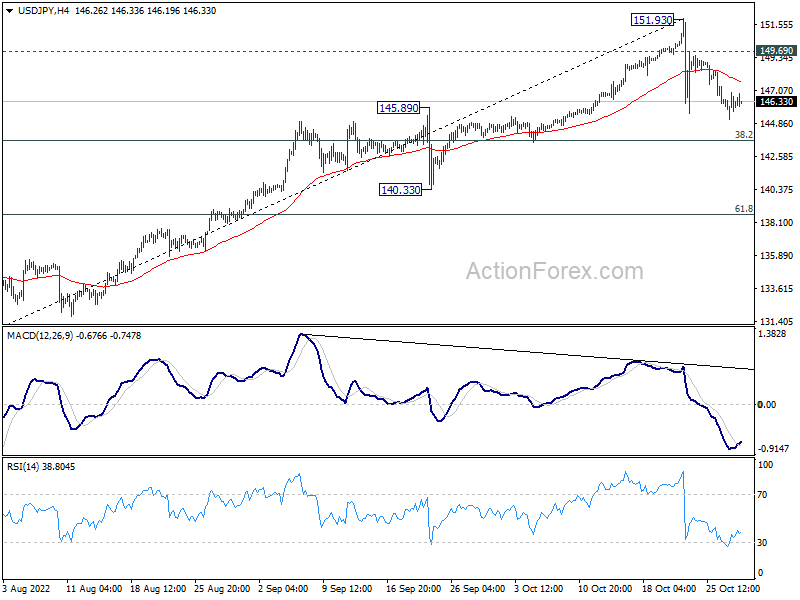

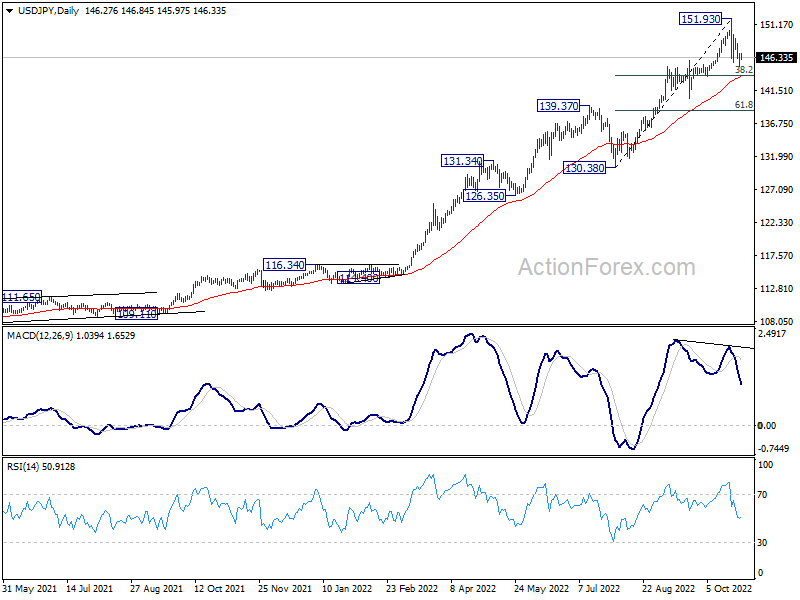

USD/JPY Daily Outlook

Daily Pivots: (S1) 145.62; (P) 147.01; (R1) 147.80; More…

USD/JPY is extending the consolidation pattern from 151.93 and intraday bias remains neutral. Deeper pull back could be seen, but downside is expected to be contained by 38.2% retracement of 130.38 to 151.93 at 143.69 to bring rebound. On the upside, above 149.69 minor resistance will bring stronger rebound back towards 151.93 high. But upside should be limited there to continue the corrective pattern.

In the bigger picture, up trend from 101.18 is still in progress, as part of the whole up trend from 75.56 (2011 low). 147.68 (1998 high) was already met and there is no clearly sign of topping yet. In any case, break of 140.33 support is needed to be the first sign of medium term topping. Otherwise, further rise is in favor to next target at 160.16 (1990 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y Oct | 3.40% | 3.20% | 2.80% | |

| 23:30 | JPY | Unemployment Rate Sep | 2.60% | 2.50% | 2.50% | |

| 00:30 | AUD | PPI Q/Q Q3 | 1.90% | 1.50% | 1.40% | |

| 00:30 | AUD | PPI Y/Y Q3 | 6.40% | 6.40% | 5.60% | |

| 03:00 | JPY | BoJ Interest Rate Decision | -0.10% | -0.10% | -0.10% | |

| 05:30 | EUR | France Consumer Spending M/M Sep | 1.20% | 1.20% | 0.00% | 0.10% |

| 05:30 | EUR | France GDP Q/Q Q3 P | 0.20% | 0.20% | 0.50% | |

| 07:00 | CHF | KOF Leading Indicator Oct | 93 | 93.8 | ||

| 08:00 | EUR | Germany GDP Q/Q Q3 P | -0.20% | 0.10% | ||

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Oct | 92.5 | 93.7 | ||

| 09:00 | EUR | Eurozone Services Sentiment Oct | 3.3 | 4.9 | ||

| 09:00 | EUR | Eurozone Industrial Confidence Oct | -2 | -0.4 | ||

| 09:00 | EUR | Eurozone Consumer Confidence Oct F | -27.6 | -27.6 | ||

| 12:00 | EUR | Germany CPI M/M Oct P | 0.60% | 1.90% | ||

| 12:00 | EUR | Germany CPI Y/Y Oct P | 10.10% | 10.00% | ||

| 12:30 | CAD | GDP M/M Aug | 0.00% | 0.10% | ||

| 12:30 | USD | Personal Income M/M Sep | 0.30% | 0.30% | ||

| 12:30 | USD | Personal Spending Sep | 0.40% | 0.40% | ||

| 12:30 | USD | PCE Price Index M/M Sep | 0.50% | 0.30% | ||

| 12:30 | USD | PCE Price Index Y/Y Sep | 5.80% | 6.20% | ||

| 12:30 | USD | Core PCE Price Index M/M Sep | 0.50% | 0.60% | ||

| 12:30 | USD | Core PCE Price Index Y/Y Sep | 5.20% | 4.90% | ||

| 12:30 | USD | Employment Cost Index Q3 | 1.30% | 1.30% | ||

| 14:00 | USD | Pending Home Sales M/M Sep | -5.30% | -2.00% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Oct F | 59.8 | 59.8 |

{kind=link}