The currency markets are generally quiet, without committed directions. Dollar is recovering broadly, ahead of near term support against European majors. Commodity currencies are softening while Yen is mixed. Some focuses be on US mid-term elections, as well as a Bundesbank symposium. But overall trading activities might remain subdued until US CPI release on Thursday.

Technically, for now, Dollar-Europeans are staying in range. That is, EUR/USD is trading inside 0.9729/1.0092, GBP/USD inside 1.1145/1.1644, USD/CHF 0.9840/1.0146. Any movements inside these ranges are seen as near term volatility only. Concurrent breakouts in these pairs are needed to confirm the next direction of the greenback.

In Asia, at the time of writing, Nikkei is up 1.31%. Hong Kong HSI is down -0.70%. China Shanghai SSE is down -0.69%. Singapore Strait Times is up 0.21%. Japan 10-year JGB yield is down -0.0078% 0.251. Overnight, DOW rose 1.31%. S&P 500 rose 0.96%. NASDAQ rose 0.85%. 10-year yield rose 0.058 to 4.214.

BoJ opinions: Undesirable to make premature changes to monetary policy

In the Summary of Opinions at BoJ’s October 27-28 meeting, it’s noted that it’s wages increase in a “sustainable and stable manner” to achieve the inflation target. Inflation could “deviate upward” form the baseline scenario but it’s still “uncertain” whether the rises in prices will be “sustainable”. It is “undesirable” to “make premature changes” to monetary policy for the “risk of disrupting the formation of a virtuous cycle between prices and wages.”

Nevertheless, on member noted, “it is necessary to examine the impact of high prices on household behavior and wages humbly and without any preconceptions while paying attention to the side effects of monetary easing.

Another member noted, “it is also important to continue to examine how future exit strategies will affect the market and whether market participants will be well prepared for them.”

Australia NAB business confidence dropped to 0, conditions dropped to 22

Australia NAB Business Confidence dropped from 5 to 0 in October. Business Conditions dropped slightly from 23 to 22. Trading conditions dropped from 37 to 31. Profitability conditions rose from 21 to 22. Employment conditions dropped from 17 to 14.

NAB Chief Economist Alan Oster said, “Conditions remained strong in October with demand still very elevated and profitability holding up… Despite the strength in conditions, confidence has been falling for several months as headwinds have weighed on the outlook for the global economy and Australia.”

Australia Westpac consumer sentiment dropped to 78, just slightly above pandemic low

Australia Westpac Consumer Sentiment dropped -6.9% to 78.0 in November. The reading was below the low point of the Global Financial Crisis in 2008, and was just slightly higher than pandemic low at 75.6.

Westpac said that inflation and interest rates are weighing heavily on family finances. Nearly 40% of consumers, a record high, look to cut Christmas spending. Confidence in house prices is heading towards 2018.19 lows.

Regarding RBA policy, Westpac expects it to hike by a further 25bps on December 6. Westpac also expects RBA to hike by an additional 0.75% out to May next year.

Australia AiG services dropped to 47.7, second month of contraction

Australia AiG Performance of Services Index dropped slightly from 48.0 to 47.7 in October, staying in contraction for a second month. Looking at some details, sales dropped -0.5 to 41.3. Employment rose 1.3 to 53.9. New orders rose 4.3 to 54.5. Input prices rose 4.2 to 77.6. Selling prices rose 3.9 to 62.2. Average wages dropped -1.1 to 64.8.

Innes Willox, Chief Executive of Ai Group, said: “Australia’s service sector faces weakening conditions. Chronic labour shortages have dragged on the supply-side of the sector for most of this year. And now the effects of cumulative interest rate rises are weakening demand conditions as well. Conditions particularly deteriorated for retail & hospitality and business & property, which are most exposed to consumer sentiment.”

RBNZ 2-yr inflation expectations rose to 3.62%

In RBNZ’s Survey of Expectations, businesses expect interest rate to rise 65bps to 4.15% a quarter ahead. In a year’s time, they saw interest rates rose further to 4.67%.

Mean one-year ahead GDP growth decreased from prior survey’s 1.49% to 1.27%. One year ahead inflation expectations rose from 4.86% in last quarter to 5.08%. Two year ahead inflation expectations rose sharply from 3.07% to 3.62%.

Looking ahead

France trade balance, Italy retail sales and Eurozone retail sales will be released in European session. US will release NFIB business optimism index.

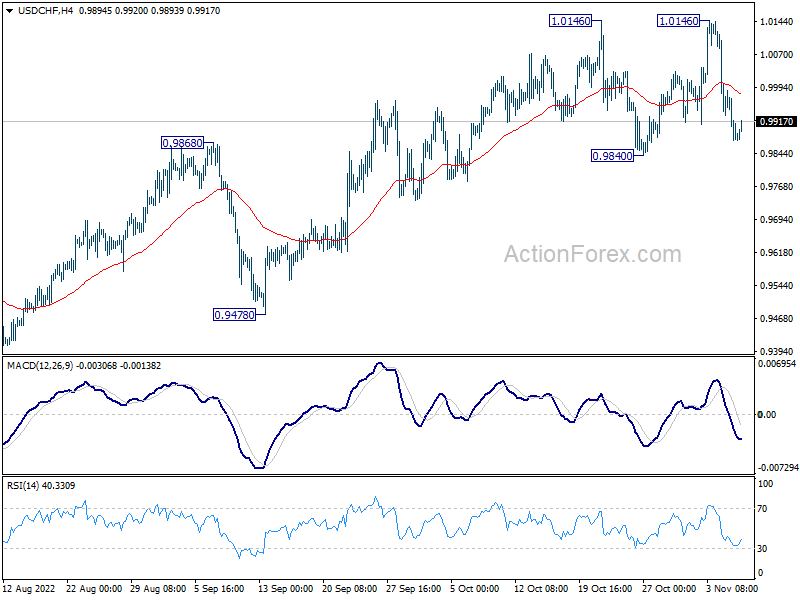

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9843; (P) 0.9916; (R1) 0.9957; More…

Intraday bias in USD/CHF remains neutral as range trading continues inside 0.9840/1.0146. Further rally is expected as long as 0.9840 support holds. Break of 1.0146 will resume larger up trend to 1.0283 projection level. However, sustained break of 0.9840 will now complete a double top pattern, and turn bias back to the downside for 0.9478 support instead.

In the bigger picture, up trend from 0.8756 (2021 low) is still in progress. Next target is 100% projection of 0.9149 to 1.0063 from 0.9369 at 1.0283, and then 1.0342 (2016 high). For now, this will remain the favored case as long as 0.9779 support holds, even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Services Index Oct | 47.7 | 48 | ||

| 23:30 | AUD | Westpac Consumer Confidence Nov | -6.90% | -0.90% | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Sep | 2.10% | 1.60% | 1.70% | |

| 23:30 | JPY | Overall Household Spending Y/Y Sep | 2.30% | 2.70% | 5.10% | |

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 00:01 | GBP | BRC Like-For-Like Retail Sales Y/Y Oct | 1.20% | 1.50% | 1.80% | |

| 00:30 | AUD | NAB Business Confidence Oct | 0 | 5 | ||

| 00:30 | AUD | NAB Business Conditions Oct | 22 | 25 | 23 | |

| 02:00 | NZD | RBNZ Inflation Expectations Q/Q Q4 | 3.62% | 3.07% | ||

| 05:00 | JPY | Leading Economic Index Sep P | 97.4 | 101.6 | 101.3 | |

| 07:45 | EUR | France Trade Balance (EUR) Sep | -14.0B | -15.3B | ||

| 09:00 | EUR | Italy Retail Sales M/M Sep | -0.10% | -0.40% | ||

| 10:00 | EUR | Eurozone Retail Sales M/M Sep | 0.00% | -0.30% | ||

| 11:00 | USD | NFIB Business Optimism Index Oct | 91.7 | 92.1 |

{kind=link}