European majors are trading generally higher today, with help from strong improvement in Germany economic sentiment as well as solid UK job data. Commodity currencies are turning softer, with Canadian Dollar shrugging off CPI data. Dollar is mixed despite sharp decline in New York State manufacturing data. Yen is so far the weakest for today, continuing to digest recent gains, awaiting tomorrow’s BoJ policy decision, which could bomb the market with surprises.

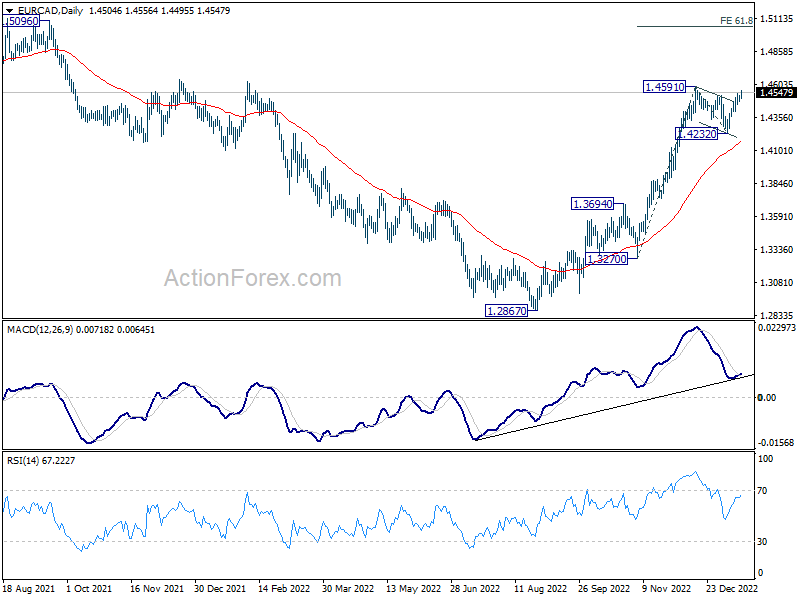

Technically, following up on GBP/CAD, breach of 1.6433 minor resistance argues that pull back from 1.6846 might have completed at 1.6099 already. Further rise should be seen to retest 1.6846 high. Firm break there will resume larger rally from 1.4069. At the same time, EUR/CAD might even lead the way by breaking through 1.4591 resistance. In that case, rise from 1.2867 should be resuming for 61.8% projection of 1.3270 to 1.4591 from 1.4232 at 1.5048.

In Europe, at the time of writing, FTSE is down -0.14%. DAX is down -0.04%. CAC is up 0.09%. Germany 10-year yield is down -0.0088 at 2.167. Earlier in Asia, Nikkei rose 1.23%. Hong Kong HSI dropped -0.78%. China Shanghai SSE dropped -0.10%. Singapore Strait Times dropped -0.09%. Japan 10-year JGB yield dropped -0.0105 to 0.504.

Canada CPI slowed to 6.3% yoy, core down to 5.3% yoy

Canada CPI slowed from 6.8% yoy to 6.3% yoy in December, matched expectations. Excluding food and energy, CPI Core slowed from 5.4% yoy to 5.3% yoy.

CPI median dropped from 5.1% yoy to 5.0% yoy, above expectation of 4.9% yoy. CPI trimmed dropped from 5.4% yoy to 5.3% yoy, above expectation of 5.2% yoy. CPI common dropped from 6.8% yoy to 6.6% yoy, matched expectations.

On a monthly basis, CPI dropped -0.6% mom, largest monthly decline since April 2020. The fall was mostly driven by gasoline prices, which also posted their largest monthly decline since April 2020.

Germany ZEW jumped to 16.9, positive again after a year

Germany ZEW Economic Sentiment jumped sharply from -23.3 to 16.9 in January, well above expectation of -15.5. That’s also the first positive reading in a year since February 2022. Current Situation improved from -61.4 to -58.6, below expectation of -57.0.

Eurozone ZEW Economic Sentiment surged from-23.6 to 16.7, well above expectation of -14.3. Current Situation rose 2.6 pts to -54.8.

ZEW President Professor Achim Wambach said: “The ZEW Indicator of Economic Sentiment signals a positive outlook again in January. For the first time since February 2022, the month in which the war in Ukraine began, the indicator points to a noticeable improvement in the economic situation over the next six months.

“The more favourable situation on the energy markets and the German government’s energy price caps have contributed to this in particular. In addition, export conditions for the German economy are improving due to China’s lifting of Covid-restrictions.

“Accordingly, the earnings expectations of the export-oriented and energy-intensive sectors have gone up significantly. The prospect that the inflation rate will continue to fall has brightened expectations for the consumer-related sectors.”

ECB Lane: Interest rates have to be higher under vast majority of scenarios

ECB Chief Economist Philip Lane said in an FT interview published today, “we’re not yet at the level of interest rates needed to bring inflation back to 2 per cent in a timely manner”, and “it still requires work”.

Under the “vast majority” of the scenarios, “interest rates do have to be higher than they are now”. “Risks are not yet two-sided, and under a wide range of scenarios, it’s still safe to bring interest rates above where they are now,” he said.

“The question is how do you get from mid-threes at the end of 2023 to the 2% target in a timely manner,” Lane said. “That’s where interest rate policy is going to be important… to make sure that the last kilometer of returning to target is delivered.”

Lane also noted, the self-reinforcing low inflation environment in Eurozone was gotten rid of as a “byproduct” of the inflation shock. He added, “the chronic low-inflation equilibrium we had before the pandemic will return.”

ECB Centeno: The economy surprises quarter after quarter

ECB Governing Council member Mario Centeno said, at a panel at the World Economic Forum, the a recession is not a foregone conclusion.

The Eurozone economy “has been surprising us quarter after quarter,” he said. “The fourth quarter in Europe will be most likely still positive. Maybe we’ll be surprised also in the first half of the year.”

Meanwhile, Centeno pledged that ECB will continue to fight inflation.

UK payrolled employment rose 28k in Dec, unemployment rate unchanged at 3.7% in Nov

In December, UK payrolled employment rose 28k or 0.1% mom to 29.9m. That’s a rise of 2.3% yoy or 676k over the 12-month period. ONS also noted that the number employees were rising in line with pre-pandemic trends. Median monthly pay rose 7.7% yoy to GBP 2194. Claimant count rose 19.7k.

In the three months November, unemployment rate was at 3.7%, 0.2% points higher than the previous three-month period, but 0.3% below pre-pandemic levels. Employment rate was unchanged at 75.6%. Economic inactivity rate was down -0.1% to 21.5%. Both average earnings including bonus and excluding bonus rose 6.4% 3moy.

China GDP growth slowed to 2.9% yoy in Q4, but beat expectations

China’s GDP growth slowed to 2.9% yoy in Q4, down from Q3’s 3.9% yoy but beat expectation of 1.8% yoy. For 2022 as a whole, GDP grew 3.0%, sharply lower than 2021’s 8.4%, but was better than 2020’s 2.2%. That’s still the second worst on record nonetheless.

In December, industrial production rose 1.3% yoy, above expectation of 0.3% yoy. Retail sales declined -1.8% yoy, much better than expectation of -9.5% yoy. Fixed asset investment grew 5.1% ytd yoy, above expectation of 5.1%.

“The foundation of domestic economic recovery is not solid as the international situation is still complicated and severe while the domestic triple pressure of demand contraction, supply shock and weakening expectations is still looming,” NBS said in a release.

Also released, China’s population decreased by -850k in 2022, the first contraction in more than six decades. Birthrate was at 6.77 births per 1000 people, sharply down from 2021’s 7.52 births, and marked the lowest level on record. Death rate rose from 7.18 to 7.37 per 1000 people, highest since 1976.

NZ NZIER business sentiment hit record low

New Zealand NZIER Quarterly Survey of Business Opinion showed, in Q4 on a seasonally adjusted basis, a net 73% of businesses expect general economic conditions to deteriorate over the coming months. That’s the worst level in the survey’s history.

A net 13% of businesses reported a decline in their own activity over the past quarter, worst since Q2 2020 during the full impact of the first pandemic lockdown. A net 33% expected decline in activity in the coming quarter.

“Firms have also reduced investment plans substantially, particularly when it comes to investment in buildings,” NZIER said. Retail businesses were feeling “very downbeat”, it found.

Australia Westpac consumer sentiment rose 5% in Jan

Australia Westpac Consumer Sentiment rose 5.0% mom to 84.3 in January, the largest monthly gain since April 2021. It’s also the second straight month of improvement, with combined rise of 8.1%. Current Conditions index rose 2.8% mom while Expectations Index rose 6.3% mom. Unemployment Expectations also improved 8.4% mom.

Westpac said: “One likely explanation for the lift in confidence is that January was the first month since April last year that did not see an increase in the RBA cash rate. While that was because there was no RBA Board meeting in the month rather than an explicit decision by the Bank to leave rates unchanged, the break in the tightening cycle looks to have provided some relief.”

Regarding RBA rate decision, Westpac expects another 25bps hike on February. It also expects clear message from RBA that the February increase will not be the last in the tightening cycle, because of a lift in annual inflation, strong retail sales growth and ongoing tight labor market.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2150; (P) 1.2219; (R1) 1.2267; More…

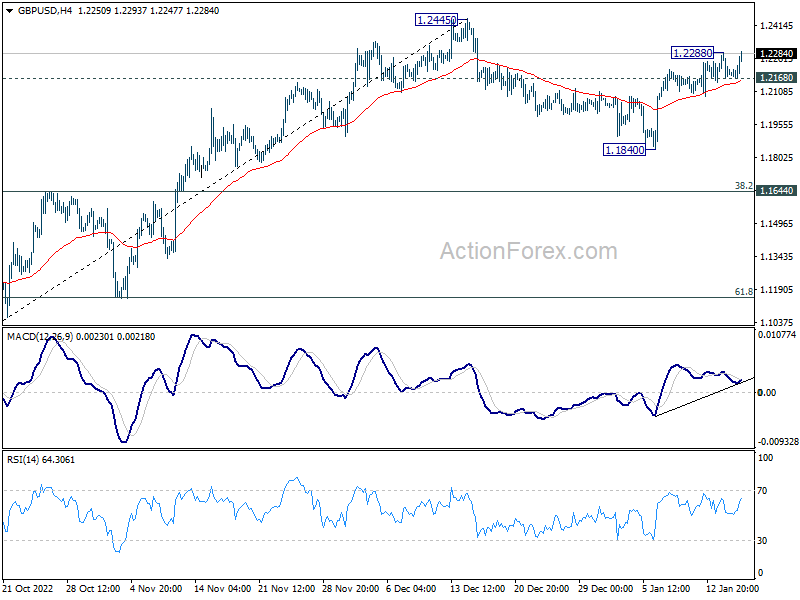

GBP/USD’s rise from 1.1840 resumed by breaking 1.2288 temporary top. Intraday bias is back on the upside for retesting 1.2445. Decisive break there will resume whole rally from 1.0351 to 1.2759 fibonacci level. On the downside, break of 1.2168 minor support will turn intraday bias neutral again.

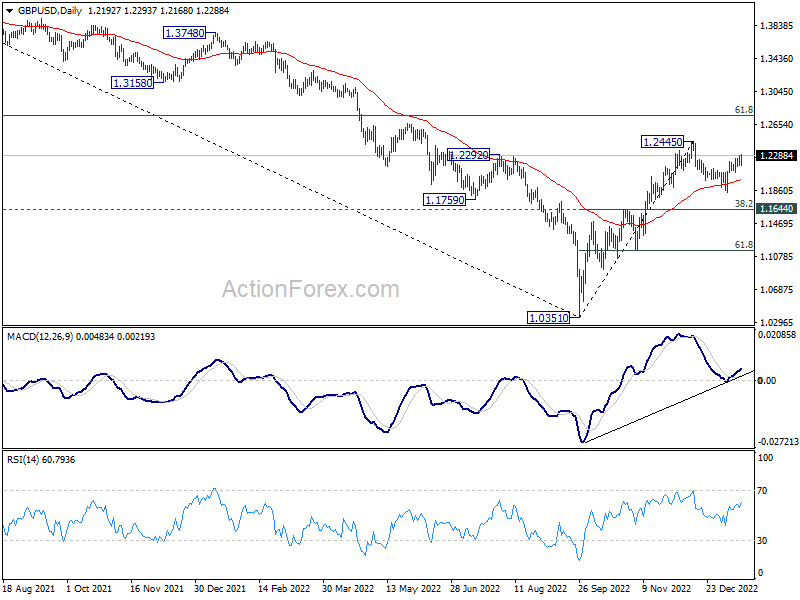

In the bigger picture, rise from 1.0351 medium term bottom is at least correcting whole down trend from 1.4248 (2021 high). Further rise is expected as long as 1.1644 resistance turned support holds. Next target is 61.8% retracement of 1.4248 to 1.0351 at 1.2759. Sustained break there will pave the way back to 1.4248.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:00 | NZD | NZIER Business Confidence Q4 | -70 | -42 | ||

| 23:30 | AUD | Westpac Consumer Confidence Jan | 5.00% | 3.00% | ||

| 02:00 | CNY | GDP Y/Y Q4 | 2.90% | 1.80% | 3.90% | |

| 02:00 | CNY | Industrial Production Y/Y Dec | 1.30% | 0.30% | 2.20% | |

| 02:00 | CNY | Retail Sales Y/Y Dec | -1.80% | -9.50% | -5.90% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Dec | 5.10% | 5.00% | 5.30% | |

| 04:30 | JPY | Tertiary Industry Index M/M Nov | -0.20% | 0.20% | 0.20% | 0.50% |

| 07:00 | GBP | Claimant Count Change Dec | 19.7K | 19.8K | 30.5K | |

| 07:00 | GBP | ILO Unemployment Rate (3M) Nov | 3.70% | 3.70% | 3.70% | |

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Nov | 6.40% | 6.10% | 6.10% | |

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Nov | 6.40% | 6.30% | 6.10% | |

| 07:00 | EUR | Germany CPI M/M Dec F | -0.80% | -0.80% | -0.80% | |

| 07:00 | EUR | Germany CPI Y/Y Dec F | 8.60% | 8.60% | 8.60% | |

| 10:00 | EUR | Germany ZEW Economic Sentiment Jan | 16.9 | -15.5 | -23.3 | |

| 10:00 | EUR | Germany ZEW Current Situation Jan | -58.6 | -57 | -61.4 | |

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Jan | 16.7 | -14.3 | -23.6 | |

| 13:15 | CAD | Housing Starts Y/Y Dec | 249K | 265K | 264K | 263K |

| 13:30 | CAD | CPI M/M Dec | -0.60% | -0.60% | 0.10% | |

| 13:30 | CAD | CPI Y/Y Dec | 6.30% | 6.30% | 6.80% | |

| 13:30 | CAD | CPI Median Y/Y Dec | 5.00% | 4.90% | 5.00% | 5.10% |

| 13:30 | CAD | CPI Trimmed Y/Y Dec | 5.30% | 5.20% | 5.30% | 5.40% |

| 13:30 | CAD | CPI Common Y/Y Dec | 6.60% | 6.60% | 6.70% | 6.80% |

| 13:30 | USD | Empire State Manufacturing Index Jan | -32.9 | -8.2 | -11.2 |

{kind=link}