The markets are overall staying in directionless mode for now. Dollar’s selloff overnight didn’t last, as risk rally faded quickly. The greenback in actually the strongest one in Asian session, while Aussie and Kiwi are the weakest, indicating some risk aversion. As for the week, Sterling is so far the best performer, followed by Swiss Franc while Euro is the worst, followed by Canadian. Risk sentiment will continue to be the main driver overall, if investors could made up their mind.

GBP/CAD is a pair to watch today given that UK GDP and Canada employment data are featured. Technically, it’s possible that the corrective pattern from 1.6846 has completed with three waves to 1.6075. Sustained trading above 4 hour 55 EMA (now at 1.6294) will affirm this case and bring stronger rise back to 1.6690/6846 resistance first. Nevertheless, rejection by 4 hour 55 EMA will open up another fall to 1.6075 and below, before the corrective pattern completes.

In Asia, at the time of writing, Nikkei is up 0.23%. Hong Kong HSI is down -2.01%. China Shanghai SSE is down -0.56%. Singapore Strait Times is down -0.23%. Japan 10-year JGB yield is up 0.001 at 0.499. Overnight, DOW dropped -0.73%. S&P 500 dropped -0.88%. NASDAQ dropped -1.02%. 10-year yield rose 0.030 to 3.683.

Japan PPI slowed to 9.5% yoy in Jan, CGPI staying at record high

Japan PPI slowed from 10.5% yoy to 9.5% yoy in January, below expectation of 11.2% yoy. Sitting at 119.8 and unchanged from prior month, corporate goods price index matched the record high made in December.

On Yen basis, export price index slowed further to 9.0% yoy, comparing to the peak of 20.1% yoy made in September. Import price index also slowed to 17.8% yoy, comparing to the peak of 49.2% made in July. For the month, export price index declined for the third month, by -1.9% mom. Import price index dropped for the fourth month, by -3.9% mom.

Japan FM Suzuki will discuss joint statement with BoJ with new governor

Japan Finance Minister Shunichi Suzuki said that the goals as mentioned in the joint statement with BoJ signed back in 2013 “remains important policy challenges”. He mentioned that targets like “the need to pull Japan out of deflation and achieve stable economic growth.”

But he also mentioned the possibility of revising the join statement with new BoJ Governor. “What to do with the statement is something the government must discuss with the new governor,” Suzuki told parliament. Nevertheless, it’s premature to decide whether it’s necessary for the revision as the government has yet to nominate the new BoJ head.

Separately, Tsuyoshi Takagi, the ruling Liberal Democratic Party’s parliament affairs chief for the lower house, said that the government will present its nomination for the new BoJ Governor and the two deputies on February 13. Jun Azumi, an executive of the opposition Constitutional Democratic Party of Japan said hearings would be held at the lower house on February 24.

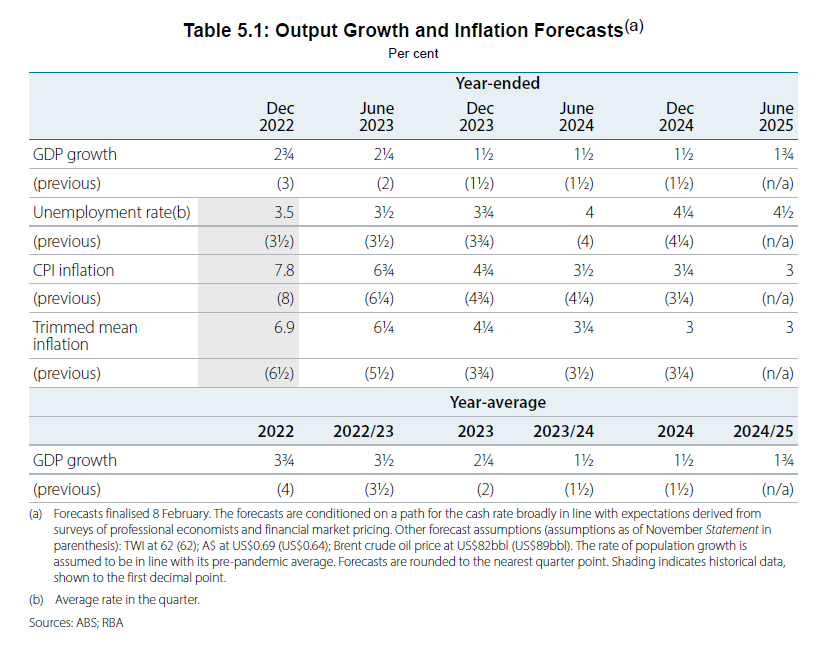

RBA SoMP: No GDP contraction, trimmed mean inflation to stay higher and longer

In the Statement on Monetary Policy, RBA reiterated that “further increases in interest rates will be needed to ensure that the current period of high inflation is only temporary.”

“In assessing how much further interest rates need to increase, the Board will be paying close attention to developments in the global economy, trends in household spending and the outlook for inflation and the labour market.”

The economy is not forecast to contract within the projection horizon. Meanwhile, trimmed mean inflation is projected to stay higher and longer till mid 2024.

Year-average GDP growth forecast to be (from 3.75% in 2022):

- 2.25% in 2023 (unchanged from prior forecast).

- 1.50% in 2024 (unchanged).

- 1.75% in 2024/25 year (new).

Headline CPI (7.8% in December 2022) is projected to slow to:

- 6.75% in June 2023 (unchanged).

- 4.75% in December 2023 (unchanged).

- 3.50% in June 2024 (down from 4.25%).

- 3.25% in December 2024 (unchanged).

- 3.00% in June 2025 (new).

Trimmed mean CPI (6.9% in December 22) is projected to slow to:

- 6.25% in June 2023 (up from 5.50%).

- 4.25% in December 2024 (up from 3.75%).

- 3.25% in June 2024 (down from 3.50%).

- 3.00% in December 2024 (down from 3.25%).

- 3.00% in June 2025 (new).

Looking ahead

UK GDP, production, goods trade balance will be released in European session. Italy will release industrial output. Later in the day, Canada employment will be a major focus, but don’t forget US U of Michigan consumer sentiment too.

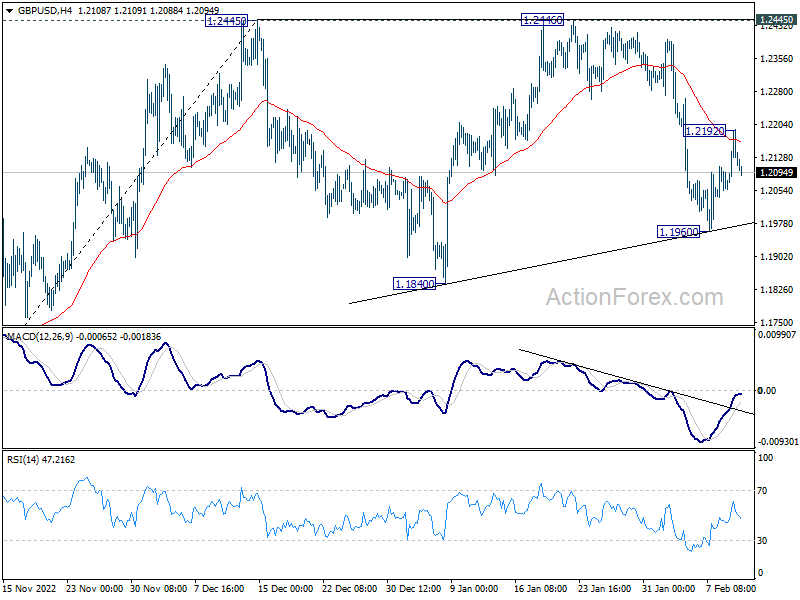

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2052; (P) 1.2123; (R1) 1.2189; More…

Despite recovering to 1.2192, GBP/USD failed to sustain above 4 hour 55 EMA and retreated. Intraday bias is turned neutral again. On the upside, break of 1.2192 will affirm the case that corrective pattern from 1.2445 has completed with three waves to 1.1960. Further rise would be seen back to 1.2445/6. Decisive break there will resume larger rise from 1.0351. On the downside, through break of 1.1960 will extend the corrective pattern with another fall to 1.1840 support and possibly below.

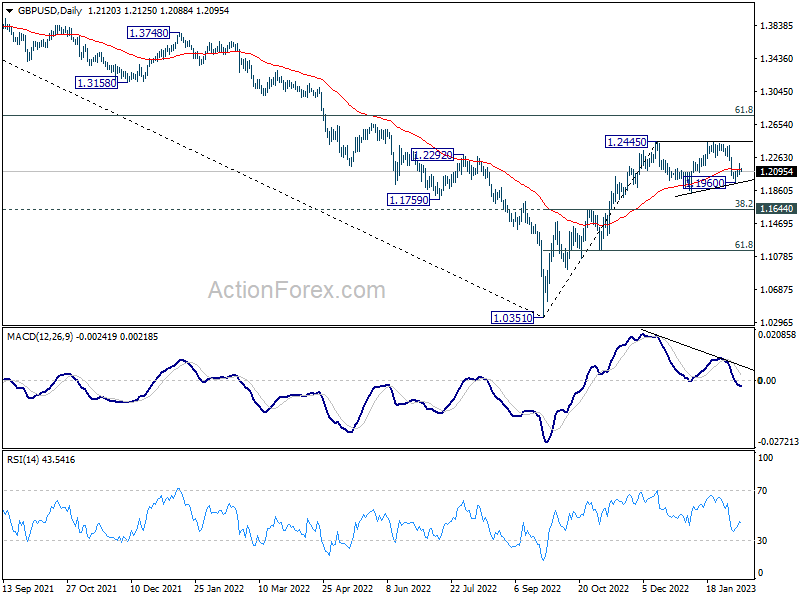

In the bigger picture, rise from 1.0351 medium term bottom is at least correcting whole down trend from 1.4248 (2021 high). Further rise is expected as long as 1.1644 resistance turned support holds. Next target is 61.8% retracement of 1.4248 to 1.0351 at 1.2759. Sustained break there will pave the way back to 1.4248.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | PPI Y/Y Jan | 9.50% | 11.20% | 10.20% | 10.50% |

| 00:30 | AUD | RBA Monetary Policy Statement | ||||

| 01:30 | CNY | CPI Y/Y Jan | 2.10% | 2.30% | 1.80% | |

| 01:30 | CNY | PPI Y/Y Jan | -0.80% | -0.50% | -0.70% | |

| 06:00 | JPY | Machine Tool Orders Y/Y Jan P | 1.00% | |||

| 07:00 | GBP | GDP M/M Dec | -0.30% | 0.10% | ||

| 07:00 | GBP | GDP Q/Q Q4 P | 0.00% | -0.30% | ||

| 07:00 | GBP | Industrial Production M/M Dec | -0.20% | -0.20% | ||

| 07:00 | GBP | Industrial Production Y/Y Dec | -5.30% | -5.10% | ||

| 07:00 | GBP | Manufacturing Production M/M Dec | -0.20% | -0.50% | ||

| 07:00 | GBP | Manufacturing Production Y/Y Dec | -6.10% | -5.90% | ||

| 07:00 | GBP | Goods Trade Balance (GBP) Dec | -17.2B | -15.6B | ||

| 09:00 | EUR | Italy Industrial Output M/M Dec | 0.10% | -0.30% | ||

| 12:00 | GBP | NIESR GDP Estimate (3M) Jan | 0.10% | |||

| 13:30 | CAD | Net Change in Employment Jan | 15.0K | 104K | ||

| 13:30 | CAD | Unemployment Rate Jan | 5.00% | 5.00% | ||

| 15:00 | USD | Michigan Consumer Sentiment Index Feb P | 65 | 64.9 |

{kind=link}