Asian markets traded on a positive note as sentiment was lifted by better-than-expected economic data from China. The strong performance of Hong Kong stocks was a clear indication of the positive outlook Commodity currencies staged a remarkable rebound, as led by New Zealand Dollar. In contrast, the Yen and the Dollar experienced mild weakness during the session. European majors, we showed a mixed performance with the Swiss Franc lagging behind as the relatively weaker one for the week.

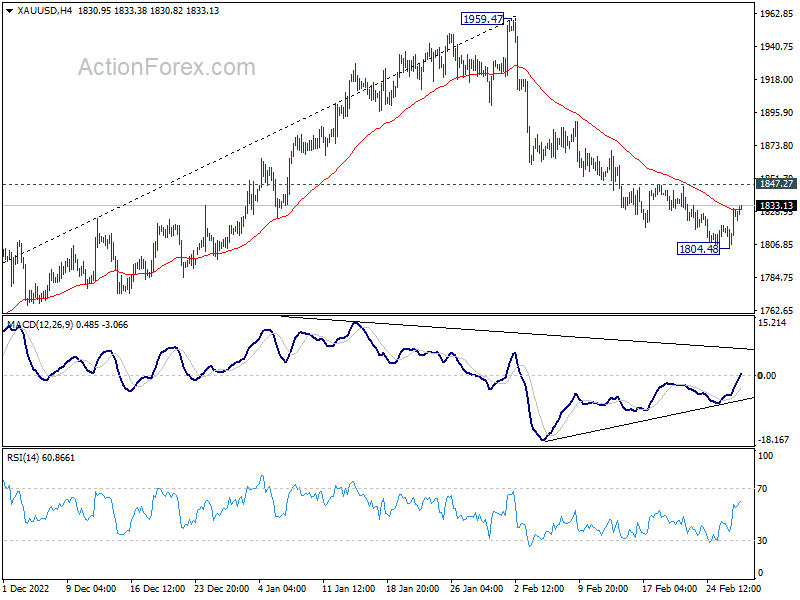

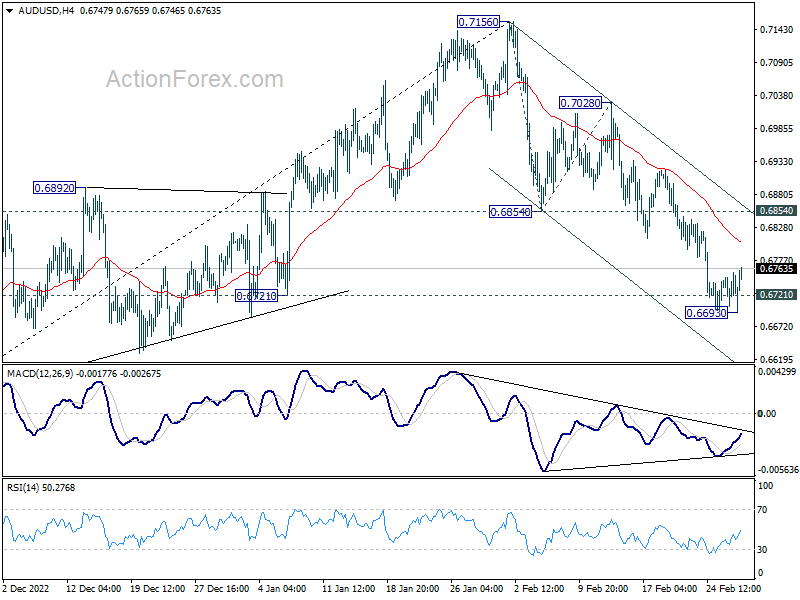

Technically, Dollar’s retreat is so far shallow, with EUR/USD holding below 1.0068 support turned resistance, GBP/USD below 1.2146 resistance, and AUD/USD well below 0.6854 support turned resistance. USD/CHF is indeed pressing 0.9428 temporary top while USD/JPY and USD/CAD are trading well above 134.04 and 1.3474 support levels respectively. Similarly, while Gold recovered after hitting 1804.48, upside is limited below 1847.27 resistance. Fall from 1959.47 is still in favor to continue. Nevertheless, break of 1847.27 will indicate short term bottoming in Gold, and possibly short term topping in Dollar too.

In Asia, Nikkei closed up 0.26%. Hong Kong HSI is up 3.79%. China Shanghai SSE is up 0.80%. Singapore Strait Times is up 0.03%. Japan 10-year JGB yield is up 0.0017 at 0.505. Overnight DOW dropped -0.71%. S&P 500 dropped -0.30%. NASDAQ dropped -0.10%. 10-year yield dropped -0.006 to 3.916

China PMI manufacturing rose to 52.6, highest since 2012

China official PMI Manufacturing rose from 50.1 to 52.6, above expectation of 50.7. That’s also the highest reading since April 2012. PMI Non-Manufacturing rose from 54.4 to 56.3, highest since March 2021. PMI Composite rose from 52.9 to 56.4.

“In February, the economic stabilisation policy measures further took effect, coupled with the epidemic’s impact receding and other favourable factors, the speed of enterprises to resume production accelerated, meaning China’s economic prosperity level continued to rebound,” said senior NBS statistician Zhao Qinghe.

Also released, Caixin PMI Manufacturing rose from 49.2 to 51.6 in February, slightly above expectation of 51.3. That the first expansion reading in 7 months, and the second-highest since May 2021. Caixin added there were renewed increases in output, new orders and employment. Suppliers’ delivery times improved at the quickest rate for eight years. Business confidence also strengthened to near two-year high.

Japan PMI manufacturing finalized at 47.7 in Feb, continually deteriorating activity

Japan PMI Manufacturing was finalized at 47.7 in February, down from January’s 48.9. That’s also the worst reading since September 2020. S&P Global also noted that backlogs of work decreased at quickest pace for 29 months. Input prices had the slowest rise for a year-and-a-half.

Usamah Bhatti, Economist at S&P Global Market Intelligence, said: “Latest data pointed to continually deteriorating activity in the Japanese manufacturing sector midway through the first quarter of 2023. Both new orders and production levels, which make up 55% of the headline PMI figure, fell at the fastest pace since July 2020 as weak domestic demand and a global economic slowdown hindered sales and output volumes.

“Moreover, the dip is likely to be sustained in the near-term as the absence of new orders amid dampened client confidence lifted capacity pressure on manufacturers further and led to the sharpest reduction in outstanding business in nearly two-and- a-half years.”

Australia CPI slowed to 7.4% yoy in Jan, ex-volatile items down to 7.2% yoy

Australia monthly CPI indicator slowed from 8.4% yoy to 7.4% yoy in January, below expectation of 8.1% yoy. CPI excluding volatile items (i.e. excludes Fruit and vegetables and Automotive fuel) slowed from 8.1% yoy to 7.2% yoy.

The most significant contributors to the annual increase in the January monthly CPI indicator were Housing (9.8%), Food and non-alcoholic beverages (8.2%) and recreation and culture (10.2%).

Australia GDP grew 0.5% qoq in Q4, domestic prices grew fastest since 1990

Australia GDP grew 0.5% qoq in Q4, below expectation of 0.8% qoq. Through the year, GDP grew 2.7% yoy. GDP Implicit price deflator (IPD) rose 1.6% qoq and 9.1% yoy. Domestic prices grew 1.4% qoq and 6.6 yoy, highest annual growth since 1990.

Katherine Keenan, ABS head of National Accounts, said, “the 0.4 per cent rise in total consumption and 1.1 per cent rise in exports were the primary contributors to GDP growth in the December quarter…

“Continued growth in household and government spending drove the rise in consumption, while increased exports of travel services and continued overseas demand for coal and mineral ores drove exports.”

Looking ahead

Swiss retail sales and manufacturing PMI will be released in European session. Germany will release CPI and unemployment. Eurozone will release PMI manufacturing final. UK will release PMI manufacturing final today too. Later in the day, Canada will release PMI manufacturing. US will release ISM manufacturing and construction spending.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6703; (P) 0.6730; (R1) 0.6757; More…

AUD/USD recovered after hitting 0.6693 and intraday bias is turned neutral first. Deeper decline is expected as long as 0.6854 support turned resistance holds. Break of 0.6693 will resume the fall from 0.7156 to 161.8% projection of of 0.6854 to 0.7028 from 0.6854 at 0.6539. Nevertheless, firm break of 0.6854 will argue that such decline is finished, and revive near term bullishness.

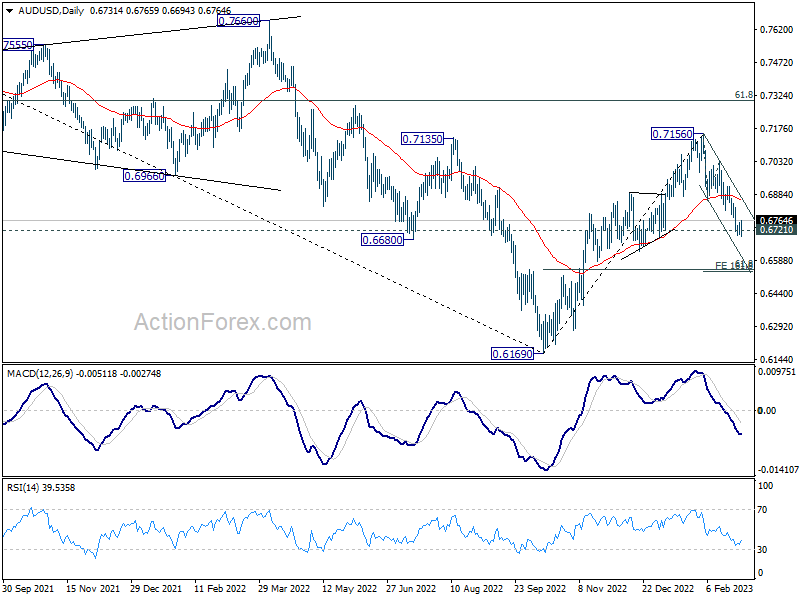

In the bigger picture, focus is now on 0.6721 structural support. Sustained break there will argue that whole rise from 0.6169 (2022 low) has completed at 0.7156, after rejection by 55 month EMA (now at 0.7179). Deeper decline would then be see back to 61.8% retracement of 0.6169 to 0.7156 at 0.6546, even as a corrective fall. Nevertheless, strong rebound from current level will retain medium term bullishness for another rise through 0.7156 later.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Jan | -1.50% | -7.20% | ||

| 00:30 | AUD | GDP Q/Q Q4 | 0.50% | 0.80% | 0.60% | 0.70% |

| 00:30 | AUD | Monthly CPI Y/Y Jan | 7.40% | 8.10% | 8.40% | |

| 00:30 | JPY | Manufacturing PMI Feb F | 47.7 | 47.4 | 47.4 | |

| 01:00 | CNY | NBS Manufacturing PMI Jan | 52.6 | 50.7 | 50.1 | |

| 01:00 | CNY | Non-Manufacturing PMI Jan | 56.3 | 55.0 | 54.4 | |

| 01:45 | CNY | Caixin Manufacturing PMI Feb | 51.6 | 51.3 | 49.2 | |

| 07:30 | CHF | Real Retail Sales Y/Y Jan | -2.20% | -2.80% | ||

| 08:30 | CHF | Manufacturing PMI Feb | 50.4 | 49.3 | ||

| 08:45 | EUR | Italy Manufacturing PMI Feb | 50.9 | 50.4 | ||

| 08:50 | EUR | France Manufacturing PMI Feb F | 47.9 | 47.9 | ||

| 08:55 | EUR | Germany Manufacturing PMI Feb F | 46.5 | 46.5 | ||

| 08:55 | EUR | Germany Unemployment Change Jan | 9K | -22K | ||

| 08:55 | EUR | Germany Unemployment Rate Jan | 5.50% | |||

| 09:00 | EUR | Eurozone Manufacturing PMI Feb F | 48.5 | 48.5 | ||

| 09:30 | GBP | Mortgage Approvals Jan | 36K | 36K | ||

| 09:30 | GBP | M4 Money Supply M/M Jan | -0.90% | -0.80% | ||

| 09:30 | GBP | Manufacturing PMI Feb F | 49.2 | 49.2 | ||

| 13:00 | EUR | Germany CPI M/M Feb P | 0.80% | 1.00% | ||

| 13:00 | EUR | Germany CPI Y/Y Feb P | 8.70% | 8.70% | ||

| 14:30 | CAD | Manufacturing PMI Feb | 51 | |||

| 14:45 | USD | Manufacturing PMI Feb F | 47.8 | 47.8 | ||

| 15:00 | USD | ISM Manufacturing PMI Feb | 47.9 | 47.4 | ||

| 15:00 | USD | ISM Manufacturing Prices Paid Feb | 45.2 | 44.5 | ||

| 15:00 | USD | ISM Manufacturing Employment Index Feb | 50.6 | |||

| 15:00 | USD | Construction Spending M/M Jan | 0.20% | -0.40% | ||

| 15:30 | USD | Crude Oil Inventories | 1.7M | 7.6M |

{kind=link}