In a surprising turn of events, the clear and direct hawkish message delivered by Fed Chair Jerome Powell has sent Dollar soaring and stocks tumbling overnight. The greenback maintained its solid gains during Asian session, and all eyes are now on Friday’s non-farm payroll report to see what the next move will be.

While Canadian dollar remains mixed, awaiting BoC’s statement today, it is widely expected that the central bank will stand pat. Australian dollar has had a rough week and continues to be the worst performer, although the sell-off appears to be slowing down a bit.

On the other hand, Yen’s decline could potentially intensify, given the outlook against other major currencies. Investors are eagerly awaiting further developments in these volatile currency markets.

Technically, if Dollar is to extend gains for the rest of the week, question is on which currency would be the biggest victim. EUR/JPY would be a pair to watch as it’s staying near term bullish in range. Break of 145.55 resistance will resume the whole rise from 137.37. That would add more fuel to USD/JPY’s rally.

In Asia, Nikkei closed up 0.48%. Hong Kong HSI is down -2.24%. China Shanghai SSE is down -0.15%. Singapore Strait Times is down -0.57%. Overnight, DOW dropped -1.72%. S&P 500 dropped -1.53%. NASDAQ dropped -1.25%. 10-year yield dropped -0.008 to 3.975.

Markets raise bets on 50bps Fed hike, a look at DOW and DXY

The markets were rocked by the “clear-cut” hawkish remarks by Fed Chair Jerome Powell overnight. In short, “he indicated that ultimate level of interests is “likely to be higher than previously anticipated”. Fed is also “prepared to increase the pace of rate hikes”. He also warned against “prematurely loosening policy. More here.

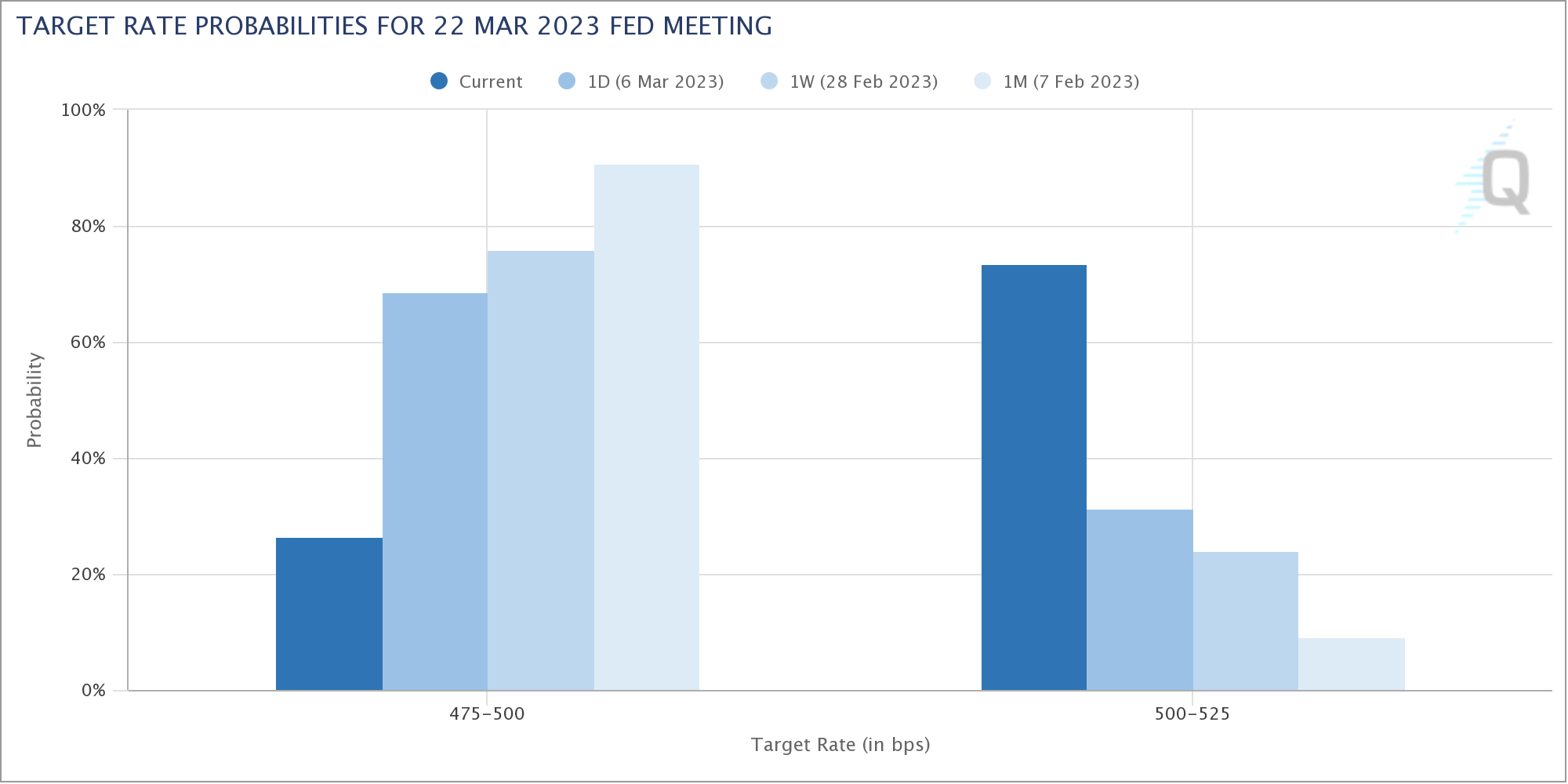

As a result, Fed fund futures are now pricing in 73% chance of a 50bps rate hike to 5.00-5.25% on March 22, comparing to just 31% a day ago.

The stock markets were sold off deeper, with DOW losing -1.72% or -574.98 pts to close at 32856.46. Technically, it isn’t the end of the world for DOW… yet, as it’s staying in familiar range despite the selloff The rejection of 55 day EMA is a bearish sign though.

So, near term focus is now back on 38.2% retracement of 28660.94 to 34712.28 at 32400.66. As long as this level holds, DOW is just in a sideway consolidation pattern.

However, sustained break there will suggest bearish reversal and at least bring deeper fall to 61.8% retracement at 30972.55.

Dollar index closed sharply higher on expectation of more aggressive Fed and risk aversion The support from 55 day EMA is a near term bullish sign. But DXY will still need to overcome 38.2% retracement of 114.77 to 100.82 at 106.14 to confirm underlying momentum.

Rejection by 106.14 will keep the rise from 100.82 as a corrective move and maintains medium term bearishness for another fall through 100.82 at a later stage. However, sustained break of 106.14 will indicate trend reversal and bring stronger rally to 109.44, and possibly above.

RBA Lowe: Further tightening required, but closer to a pause

RBA Governor Philip Lowe said in a speech that further rate hike is still necessary. But the central bank is now closer to the point of a pause.

The board’s judgment remained that “further tightening of monetary policy is likely to be required to bring inflation back to target within a reasonable timeframe”, Lowe said.

“Inflation is still too high and while it looks to be on a declining path it is likely to remain higher than target for a few years,” he added. “If we don’t get inflation down fairly soon, the end result will be even higher interest rates and more unemployment.

Meanwhile, ” with monetary policy now in restrictive territory, we are closer to the point where it will be appropriate to pause interest rate increases to allow more time to assess the state of the economy,” he noted.

“At what point it will be appropriate to pause will be determined by the data and our assessment of the outlook”.

SNB Jordan: Monetary policy is still too loose

Swiss National Bank Chairman Thomas Jordan, stated that the current monetary policy is too loose to bring inflation back to price stability in the medium term, and further tightening cannot be ruled out. The comment came after recent data showed that consumer inflation reaccelerated to 3.4% in February, staying well above SNB’s 0-2% target.

“The SNB’s monetary policy is still too loose to return inflation back to price stability in the medium term,” Jordan yesterday at Zurich University. “We cannot exclude that we have to tighten further.”

“The SNB has to act to reach price stability in the medium term again,” he said. “The barren Swiss labor market can lead to second- and third-round effects happening more easily.”

Meanwhile Jordan also pointed out that the central bank has more than one option, as “we can raise rates, but also sell foreign currency — and we have sold foreign currency in the past.”

SNB will meet on March 23 to decide on monetary policy.

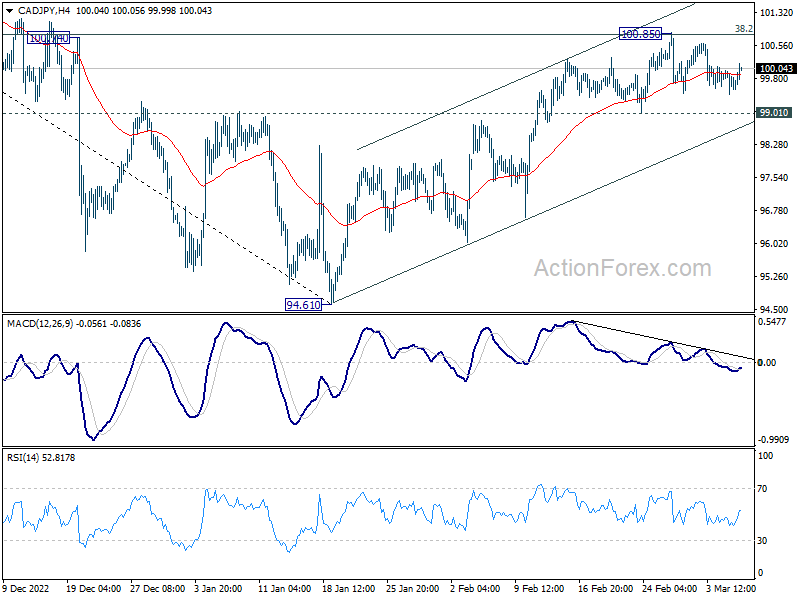

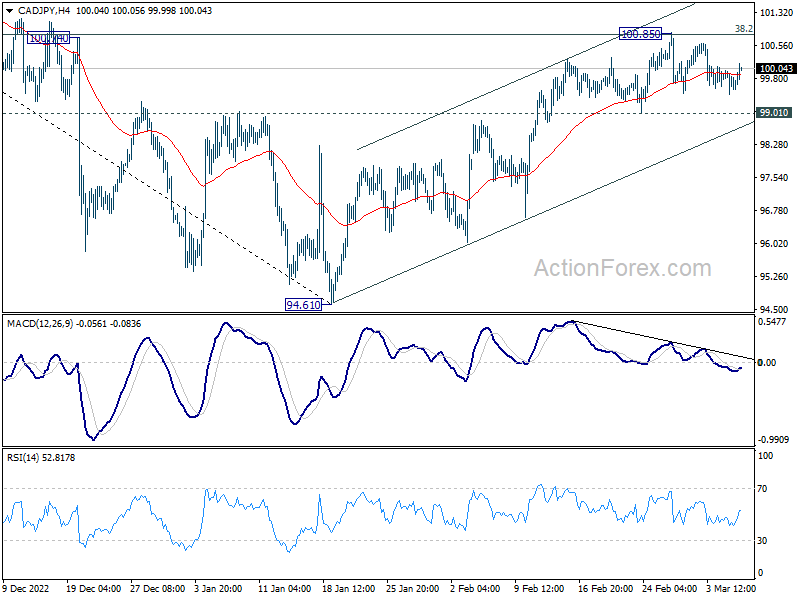

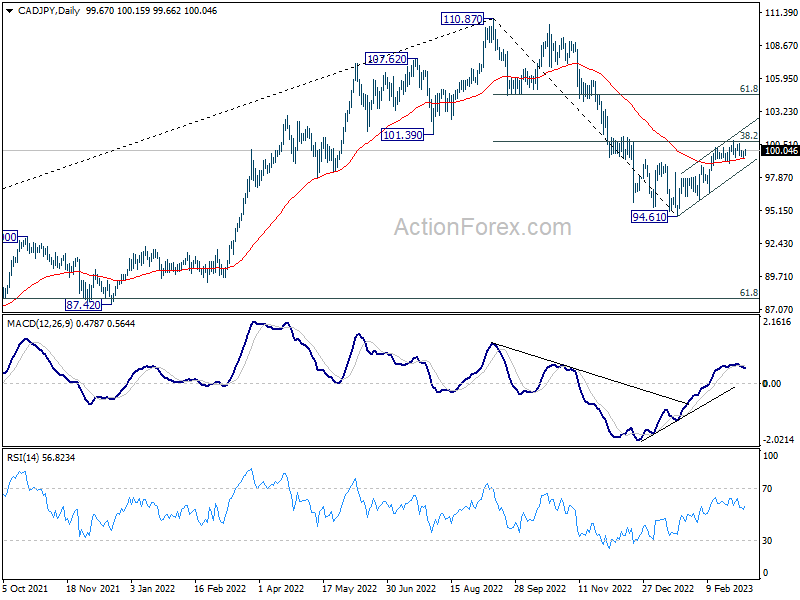

BoC to stand pat, CAD/JPY staying bullish in range

BoC is widely expected to stand pat today, and keep the benchmark overnight rate unchanged at 4.50%. Governor Tiff Macklem has explicitly indicated that in inflation comes down as predicted, there is no need to raise interest rates further. But of course, he’s prepared to act if that doesn’t happen as expected. For now, markets are pricing in around 80% chance of another hike within this year. But it’s too early for BoC to shift its evidence for now.

Some previews on BoC:

- Bank of Canada to Set Tightening Campaign on Hold

- Bank of Canada Preview: At Interest Rates Peak?

- Canadian jobs report, Bank of Canada decision back in the spotlight

Canadian Dollar’s performance this week is not too bad, as it’s just down against the strong Dollar, Euro and Swiss Franc. For example, CAD/JPY is just holding in range below 100.85 temporary top, with the shallow retreat contained above 99.02 support, as well as 55 day EMA. Further rally remains in favor.

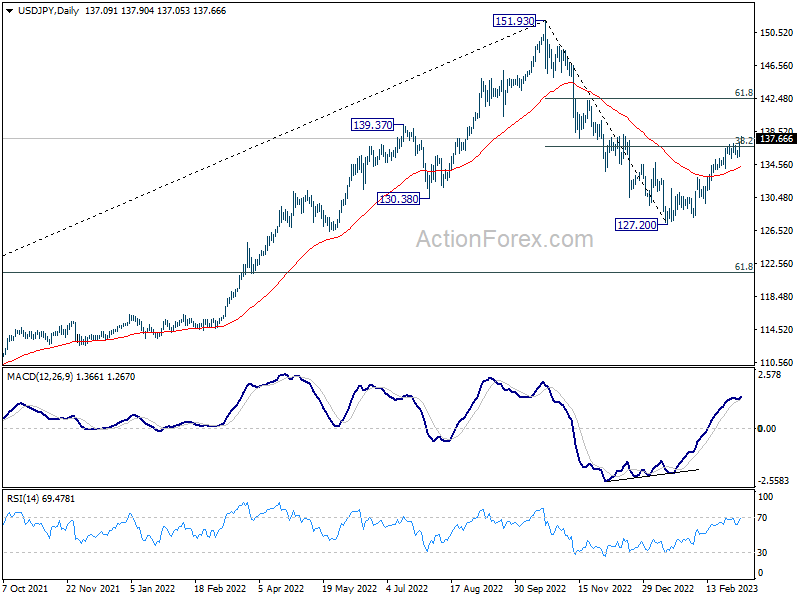

Firm break of 38.2% retracement of 110.87 to 94.61 at 110.82 will argue that the down trend from 110.87 to 94.61 is reversal. That would bring stronger rally to 61.8% retracement at 104.65. (USD/JPY has taken out equivalent level of 38.2% retracement of 151.93 to 127.20 at 136.64 already).

Elsewhere

Germany industrial production, retail sales, Italy retail sales, Eurozone GDP and employment final will be released in European session.

Later in the day, US will release ADP employment and trade balance. Fed chair Jerome Powell will have the second day of testimony. Fed will also publish Beige Book report. Canada will release trade balance before BoC rate decision.

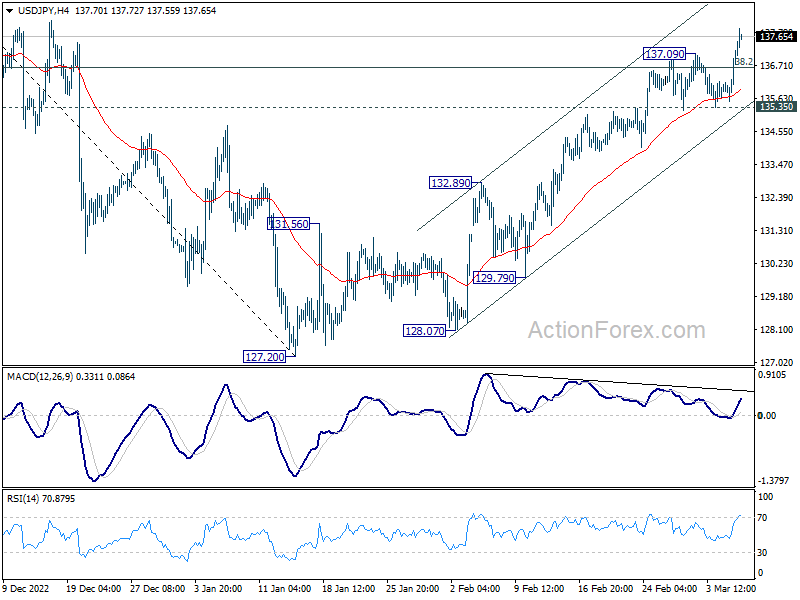

USD/JPY Daily Outlook

Daily Pivots: (S1) 136.07; (P) 136.63; (R1) 137.72; More…

USD/JPY’s rally resumed to breaking through 137.09 resistance. The strong break of 136.64 fibonacci level also carries larger bullish implication. Intraday bias is back on the upside. Current rally would now target next fibonacci level at 142.48. On the downside, break of 135.35 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, the break of 38.2% retracement of 151.93 to 127.20 at 136.64 suggests that whole down trend from 151.93 has completed at 127.20 already. Tentatively, rise from 127.20 is seen as the second leg the medium term pattern from 151.93. Further rally is expected to 61.8% retracement at 142.48. This will now remain the favored case as long as 55 day EMA (now at 134.10) holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Bank Lending Y/Y Feb | 3.30% | 3.20% | 3.10% | |

| 23:50 | JPY | Current Account (JPY) Jan | 0.22T | 0.85T | 1.18T | |

| 05:00 | JPY | Leading Economic Index Jan P | 96.5 | 97.1 | 97.2 | |

| 05:00 | JPY | Eco Watchers Survey: Current Feb | 52 | 48.3 | 48.5 | |

| 07:00 | EUR | Germany Industrial Production M/M Jan | 1.50% | -3.10% | ||

| 07:00 | EUR | Germany Retail Sales M/M Jan | 2.00% | -5.30% | ||

| 09:00 | EUR | Italy Retail Sales M/M Jan | 0.20% | -0.20% | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q4 F | 0.10% | 0.10% | ||

| 10:00 | EUR | Eurozone Employment Change Q/Q Q4 F | 0.40% | 0.40% | ||

| 13:15 | USD | ADP Employment Change Feb | 200K | 106K | ||

| 13:30 | USD | Trade Balance (USD) Jan | -69.0B | -67.4B | ||

| 13:30 | CAD | Trade Balance (CAD) Jan | -0.2B | -0.2B | ||

| 15:00 | USD | Fed’s Chair Powell testifies | ||||

| 15:00 | CAD | BoC Interest Rate Decision | 4.50% | 4.50% | ||

| 15:30 | USD | Crude Oil Inventories | 1.3M | 1.2M | ||

| 18:00 | USD | Fed’s Beige Book |

{kind=link}