Dollar is currently taking a pause from its recent gains, with traders digesting the impact of Fed Chair Jerome Powell’s previous testimony. While Powell will appear again in front of Congress today, there shouldn’t be any more surprises. The market has also remained relatively unmoved by a stronger-than-expected ADP private job report, with many traders waiting for Friday’s non-farm payroll report before making any significant moves.

Swiss Franc and Euro are currently among the strongest currencies this week, trailing Dollar. Meanwhile, Australian dollar is still struggling, despite a slight recovery today, and Sterling and New Zealand dollar are also underperforming. Yen is mixed, with its fortunes largely dependent on the development of treasury yields and the upcoming BoJ meeting on Friday. Finally, the Canadian Dollar is also mixed, with traders awaiting the BoC’s decision later in the session.

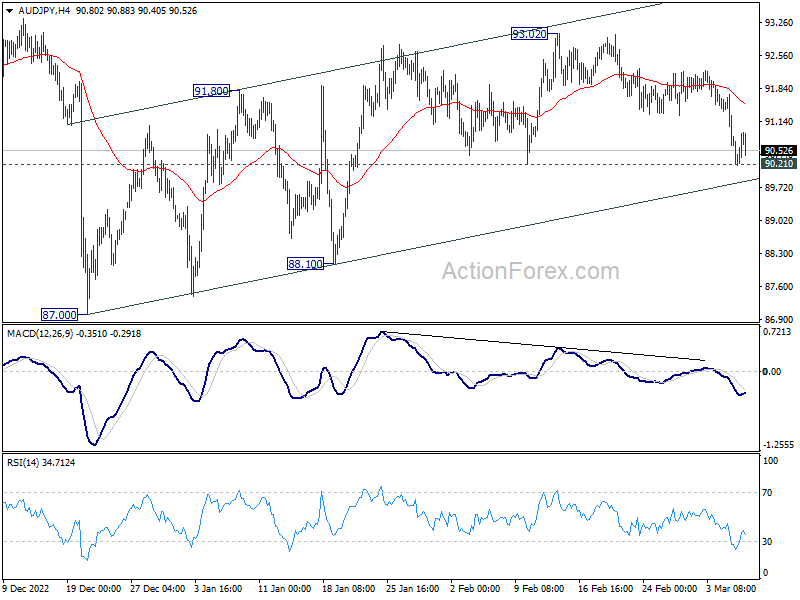

Technically, AUD/JPY is under pressure once again after a weak recovery earlier in the day If the cross breaks below the support level of 90.21 decisively, it would indicate that the corrective recovery from 87.00 to 93.02 has ended. In this case, a deeper fall could be expected towards the support zone of 87.00/88.10. Such a drop is likely to be accompanied by a deeper selloff in the Aussie in other trading pairs as well.

In Europe, at the time of writing, FTSE is up 0.08%. DAX is up 0.42%. CAC is up 0.04%. Germany 10-year yield is down -0.0378 at 2.651. Earlier in Asia, Nikkei rose 0.48%. Hong Kong HSI dropped -2.35%. China Shanghai SSE dropped -0.06%. Singapore Strait Times dropped -0.57%. Japan 10-year JGB yield rose 0.0012 to 0.507.

US ADP jobs grew 242k in Feb, pay growth still quite elevated

US ADP private sector employment grew 242k in February, above expectation of 200k. By sector, goods-producing jobs rose 52k and service-providing jobs rose 190k. By size, small companies lost -61k jobs, but medium companies added 148k and large companies added 160k. Pay growth for job stays slowed to 7.2% yoy, slowest in 12 months.

“There is a tradeoff in the labor market right now,” said Nela Richardson, chief economist, ADP. “We’re seeing robust hiring, which is good for the economy and workers, but pay growth is still quite elevated. The modest slowdown in pay increases, on its own, is unlikely to drive down inflation rapidly in the near-term.”

BoE Dhingra: Prudent to hold rates steady because of material overtightening risk

BoE dove Swati Dhingra warned in a speech that overtightening posses a more material risk now. She called for holding interest rate unchanged.

“Overtightening poses a more material risk at this point, through potential negative impacts from increased borrowing costs and reduced supply capacity going forwards,” she explained. “It risks unnecessarily denting output at a time when the economy is weak and deepening the pain for households when budgets are already squeezed through energy and housing costs.”

“In my view, a prudent strategy would hold policy steady amidst growing signs external price pressures are easing, and be prepared to respond to developments in price evolution. This would avoid overtightening and return the economy sustainably to our 2% inflation target in the medium-term.”

“Overall, the evidence does not point to persistent cost-push inflation becoming embedded in wages and margins,” she said. “Even after a year and a half of above-target inflation, there is little evidence for such cost-push inflation beyond what might be expected following an unprecedented terms of trade shock.”

“Consumption remains weak and many of the tightening effects of monetary policy are yet to fully take hold,” she added.

RBA Lowe: Further tightening required, but closer to a pause

RBA Governor Philip Lowe said in a speech that further rate hike is still necessary. But the central bank is now closer to the point of a pause.

The board’s judgment remained that “further tightening of monetary policy is likely to be required to bring inflation back to target within a reasonable timeframe”, Lowe said.

“Inflation is still too high and while it looks to be on a declining path it is likely to remain higher than target for a few years,” he added. “If we don’t get inflation down fairly soon, the end result will be even higher interest rates and more unemployment.

Meanwhile, ” with monetary policy now in restrictive territory, we are closer to the point where it will be appropriate to pause interest rate increases to allow more time to assess the state of the economy,” he noted.

“At what point it will be appropriate to pause will be determined by the data and our assessment of the outlook”.

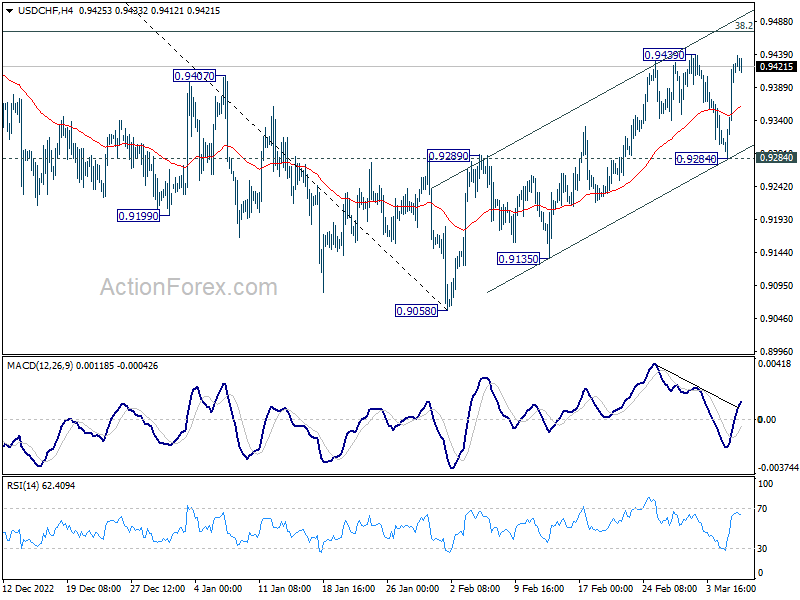

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9329; (P) 0.9378; (R1) 0.9469; More…

Intraday bias in USD/CHF stays on the upside with focus on 0.9439 resistance. Break there will resume the rise from 0.9058 for 38.2% retracement of 1.0146 to 0.9058 at 0.9474. Decisive break there will carry larger bullish implications. On the downside, break of 0.9284 will turn bias back to the downside for retesting 0.9058 low instead.

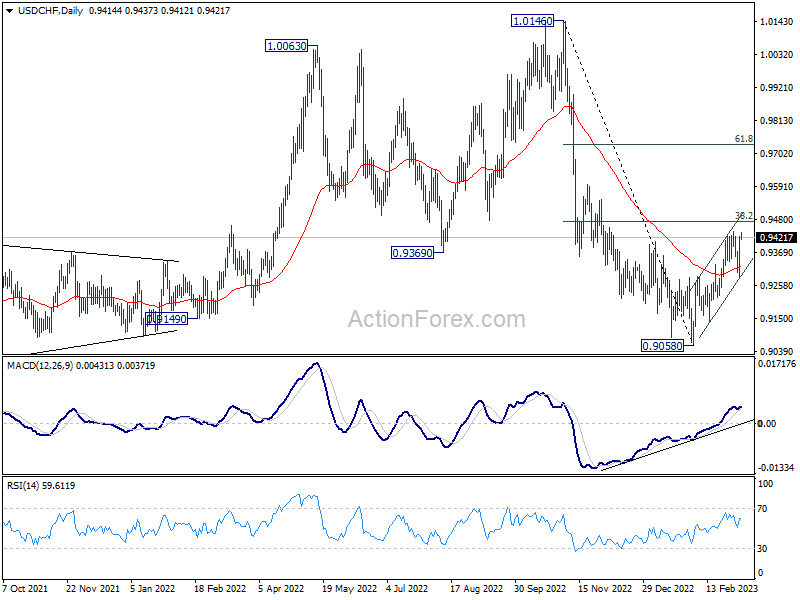

In the bigger picture, decline from 1.0146 is seen as part of a long term sideway pattern. As long as 38.2% retracement of 1.0146 to 0.9058 at 0.9474 holds, another fall is in favor through 0.9058. However, sustained trading above 0.9474 will indicate that the medium term trend has reversed, and open up further rally to 61.8% retracement at 0.9730 and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Bank Lending Y/Y Feb | 3.30% | 3.20% | 3.10% | |

| 23:50 | JPY | Current Account (JPY) Jan | 0.22T | 0.85T | 1.18T | |

| 05:00 | JPY | Leading Economic Index Jan P | 96.5 | 97.1 | 97.2 | |

| 05:00 | JPY | Eco Watchers Survey: Current Feb | 52 | 48.3 | 48.5 | |

| 07:00 | EUR | Germany Industrial Production M/M Jan | 3.50% | 1.50% | -3.10% | -2.40% |

| 07:00 | EUR | Germany Retail Sales M/M Jan | -0.30% | 2.00% | -5.30% | -4.90% |

| 09:00 | EUR | Italy Retail Sales M/M Jan | 1.70% | 0.20% | -0.20% | |

| 10:00 | EUR | Eurozone GDP Q/Q Q4 F | 0.00% | 0.10% | 0.10% | |

| 10:00 | EUR | Eurozone Employment Change Q/Q Q4 F | 0.30% | 0.40% | 0.40% | |

| 13:15 | USD | ADP Employment Change Feb | 242K | 200K | 106K | 119K |

| 13:30 | USD | Trade Balance (USD) Jan | -68.3B | -69.0B | -67.4B | -67.2B |

| 13:30 | CAD | Trade Balance (CAD) Jan | 1.9B | -0.2B | -0.2B | 1.2B |

| 15:00 | USD | Fed’s Chair Powell testifies | ||||

| 15:00 | CAD | BoC Interest Rate Decision | 4.50% | 4.50% | ||

| 15:30 | USD | Crude Oil Inventories | 1.3M | 1.2M | ||

| 18:00 | USD | Fed’s Beige Book |

{kind=link}