The forex markets appear stable in today’s Asian session, with most major pairs and crosses remaining within yesterday’s range. Stabilization of US stocks helped calm investors for now, but overall sentiment remains vulnerable. Australian Dollar continues to be the week’s worst performer, facing a triple blow of risk aversion, declining copper prices, and RBA speculation. Canadian Dollar trails as the second-worst performer, while Dollar is the third weakest due to concerns over regional bank issues.

On the flip side, Euro leads this week on expectations of extended tightening by the ECB and optimism that the Eurozone economy is regaining momentum in Q2. Sterling and Swiss Franc are also performing well. Surprisingly, Yen is currently the second-best performer, partly due to falling yields and risk aversion. However, Yen’s weekly gain is limited so far, and its next move will depend heavily on tomorrow’s BoJ rate decision.

Technically, Bitcoin appears to have found support at 55 D EMA and rebounded notably yesterday. This development keeps near-term outlook bullish for another rise soon. Breaking 31,011 resistance level will resume the overall rally from 15,452 low. It’s worth noting that the NASDAQ is also attempting to find support from 55 D EMA. If Bitcoin’s rise resumes, it could signal a return to a risk-on sentiment, at least in the tech sector. This development could help NASDAQ rebound from its current level towards 12,695, bolstering overall market sentiment.

In Asia, at the time of writing, Nikkei is up 0.01%. Hong Kong HSI is down -0.15%. China Shanghai SSE is up 0.30%. Singapore Strait Times is down -0.49%. Japan 10-year JGB yield is up 0.006 at 0.464. Overnight, DOW dropped -0.68%. S&P 500 dropped -0.38%. NASDAQ rose 0.47%. 10-year yield rose 0.036 to 3.432.

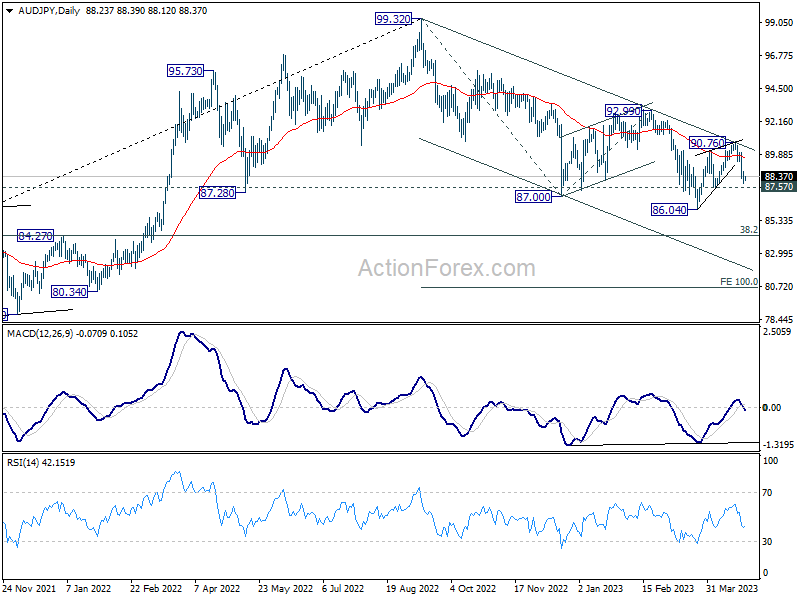

AUD/JPY a top loser as Aussie suffers triple blow

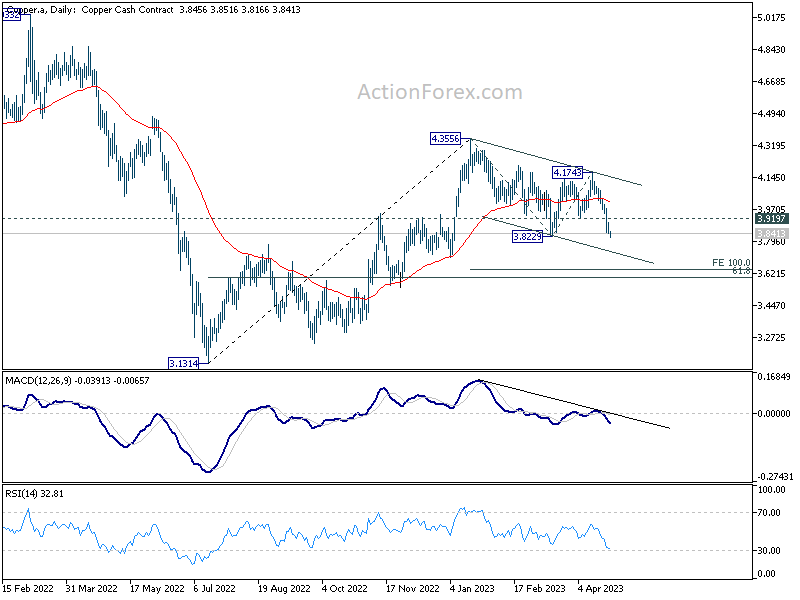

Australian Dollar continues to trade as the worst performer for the week, suffering triple blow including risk aversion, free fall in copper price and RBA speculations. Copper’s selloff accelerated this week and broke to new low in 2023 today. There are increasing doubts on whether RBA will raise interest rate next week or opt for the second pause in a row after yesterday’s CPI data.

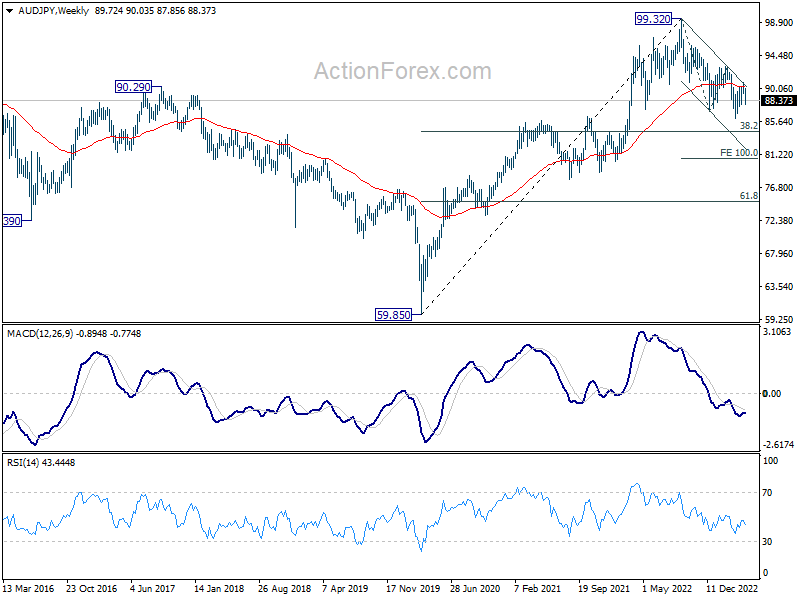

AUD/JPY is currently the second biggest mover for the week, just next to EUR/AUD. Current development indicates that corrective recovery from 86.04 has concluded with three waves up to 80.76, after being rejected by channel resistance. This implies that the larger downtrend from 99.32 (2022 high) is ongoing and may be ready to resume.

Immediate focus is now on 87.57 support. Firm break there will confirm this bearish case, and target 38.2% retracement of 59.85 to 99.32 at 84.24. Firm break there could prompt downside acceleration to 100% projection of 99.32 to 87.00 from 92.99 at 80.67. But of course, the whole development would also depend on any surprise from BoJ on Friday.

As for Copper, with breach of 3.8229 support, whole decline from 4.3556 is likely resuming. There is risk of more downside acceleration if it cannot recovery back above 3.9197 support turned resistance soon. Next target would be 100% projection of 4.3555 to 3.8229 from 4.1743 at 3.6416, which is close to 61.8% retracement of 3.1314 to 4.3556 at 3.5990, that is, around 3.6 handle. If this extended selloff in copper materializes, it could put additional pressure on Aussie.

NZ ANZ business confidence dropped slightly, inflation expectation lowest since Mar 2022

New Zealand ANZ Business Confidence index decrease slightly in April, dipping from -43.4 to -43.8. On the other hand, Own Activity Outlook improved from -8.5 to -7.6. A closer look at the details reveals that export intentions jumped from -8.9 to -1.5, while investment intentions remained unchanged at -6.8. Employment intentions rose from -4.6 to -2.4, and pricing intentions fell from 56.8 to 53.7. Cost expectations dropped from 86.4 to 84.2, and profit expectations declined from -33.9 to -37.7.

Inflation expectations decreased from 5.82 to 5.70, reaching the lowest level since March 2022. ANZ observed that the overall decline in inflation signals is consistent with RBNZ gradually gaining traction. However, the situation is far from resolved, as the proportion of firms experiencing high costs and intending to raise prices remains “problematically high”.

ANZ added: “The RBNZ will be encouraged to see the ongoing fall in the inflation indicators in the survey. While there’s still a way to go, inflation is set to continue easing over the year ahead, as they and we are forecasting.

“It’s important to note that the data does not represent a ‘surprise’ for the RBNZ; rather, it’s what they will be expecting to see if their forecasts are to come to fruition, with the OCR able to top out shortly.

“There are risks on both sides: inflation could get “stuck” north of the target band, or global markets could deliver a side-swipe, for example. But the overall message from this month’s survey is “on track.”

Looking ahead:

Eurozone economic sentiment indictor is the main feature in European session. US Q1 GDP advance will take center stage later in the day, with jobless claims and pending home sales scheduled too.

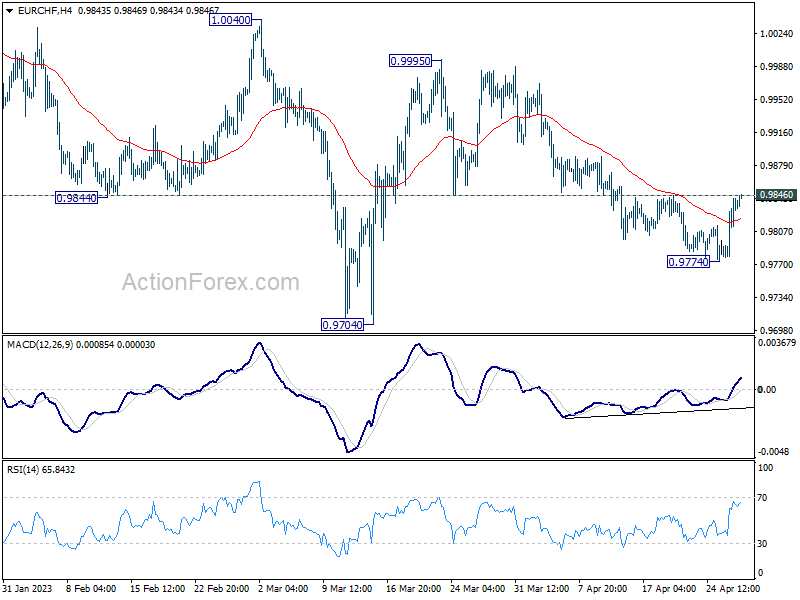

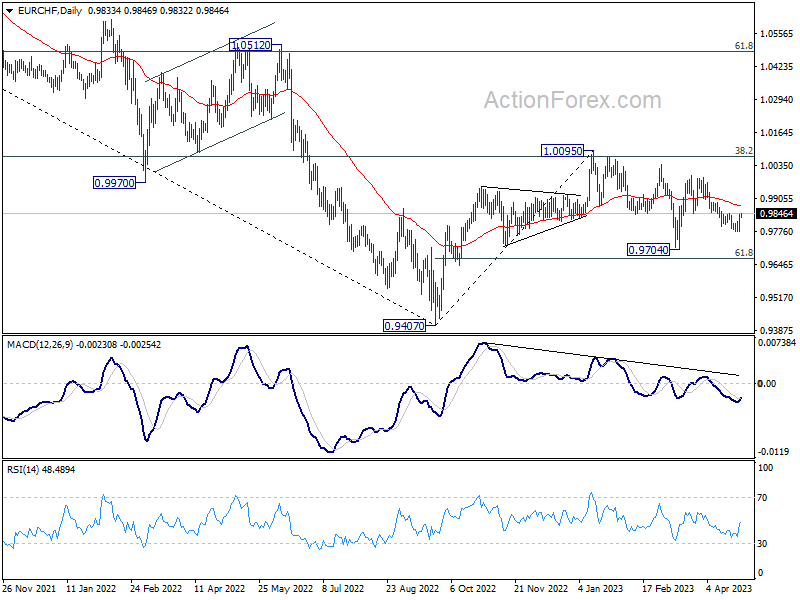

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9798; (P) 0.9821; (R1) 0.9864; More…

Immediate focus is now on 0.9846 in EUR/CHF as rebound from 0.9774 extends. Decisive break there will argue that pull back from 0.9995 has completed. More importantly, that would revive the case that whole correction from 1.0095 has completed at 0.9704. Intraday bias will be back on the upside for 55 D EMA (now at 0.9876). Sustained trading above there will pave the way back to 0.9995 resistance next. Nevertheless, break of 0.9774 will resume recent decline to 0.9704 support and below.

In the bigger picture, prior rejection by 55 W EMA (now at 0.9989) and 38.2% retracement of 1.1149 to 0.9407 at 1.0072 suggests that medium term outlook is staying bearish. That is, down trend from 1.2004 is not completed yet and is in favor to resume through 0.9407 at a later stage. However, decisive break of 1.0095 resistance will raise the chance of bullish trend reversal. Rise from 0.9407 should then target 1.0505 cluster resistance (2020 low at 1.0505, 61.8% retracement of 1.1149 to 0.9407 at 1.1484).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:00 | NZD | ANZ Business Confidence Apr | -43.8 | -43.4 | ||

| 01:30 | AUD | Import Price Index Q/Q Q1 | -4.20% | 0.60% | 1.80% | |

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Apr | 99.9 | 99.3 | ||

| 09:00 | EUR | Eurozone Services Sentiment Apr | 9.5 | 9.4 | ||

| 09:00 | EUR | Eurozone Industrial Confidence Apr | 0.2 | -0.2 | ||

| 09:00 | EUR | Eurozone Consumer Confidence Apr F | -17.5 | -17.5 | ||

| 12:30 | USD | Initial Jobless Claims (Apr 21) | 245K | 245K | ||

| 12:30 | USD | GDP Annualized Q1 P | 2.00% | 2.60% | ||

| 12:30 | USD | GDP Price Index Q1 P | 3.70% | 3.90% | ||

| 14:00 | USD | Pending Home Sales M/M Mar | 1.00% | 0.80% | ||

| 14:30 | USD | Natural Gas Storage | 76B | 75B |

{kind=link}