Dollar weakens broadly in today’s Asian session as markets await what could be the last Fed rate hike in the current cycle. Risk sentiment is on the downside, with stock selloff carrying over from the US to Asia. Despite this, the greenback sees no apparent support. Conversely, Yen benefits from cautious sentiment a decline in benchmark treasury yields. Oversold condition is also helping the Japanese currency slightly.

Commodity currencies show mixed performance, with notable strength seen in New Zealand Dollar. Solid employment and wage data support another RBNZ hike later this month. Australian Dollar continues to reverse yesterday’s gains following the surprising RBA hike, while Canadian Dollar remains sluggish due to falling oil prices. European majors are also mixed, with eyes on tomorrow’s ECB rate decision.

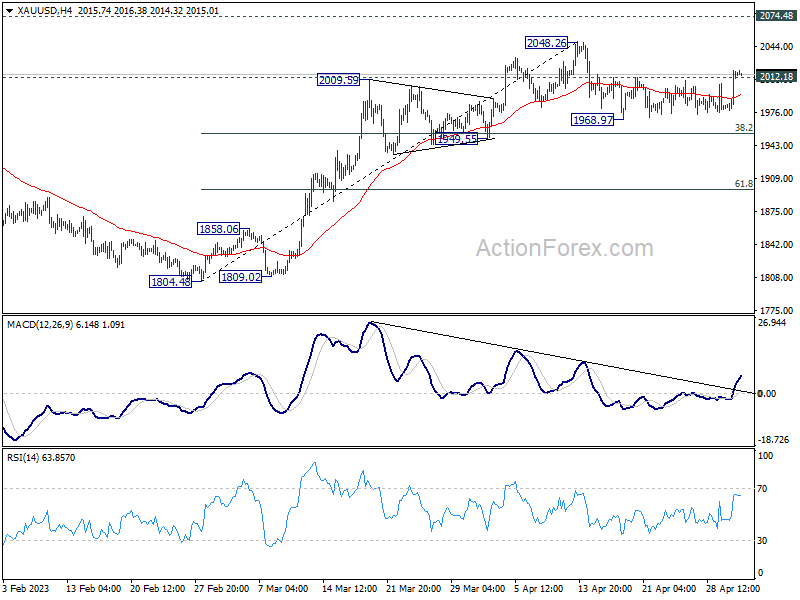

In technical terms, Gold broke 2012.18 resistance level overnight due to risk aversion, contrary to our expectations. This development suggests that pullback from 2048.26 may have already completed after defending 38.2% retracement of 1,804.48 to 2,048.26 well. Stronger rally back to 2,048.26 is now favored, with a break there resuming larger rally towards 2074.48 record high. If realized, this could also coincide with upside breakout in EUR/USD through 1.1094.

In Asia, at the time of writing, Hong Kong HSI is down -1.84%. Singapore Strait Times is down -0.81%. Japan and China are on holiday. Overnight, DOW dropped -1.08%. S&P 500 dropped -1.16%. NASDAQ dropped -1.08%. 10-year yield dropped -0.135 to 3.439.

NZD/USD jumps as strong job data supports another RBNZ hike

New Zealand Dollar surges broadly today, as strong job growth data together with record annual wages growth basically seal the deal for another RBNZ rate hike on May 24.

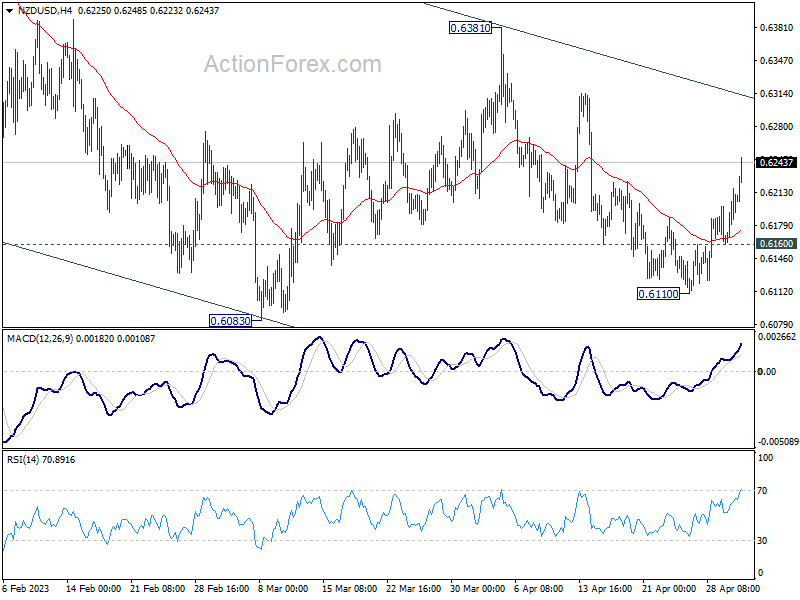

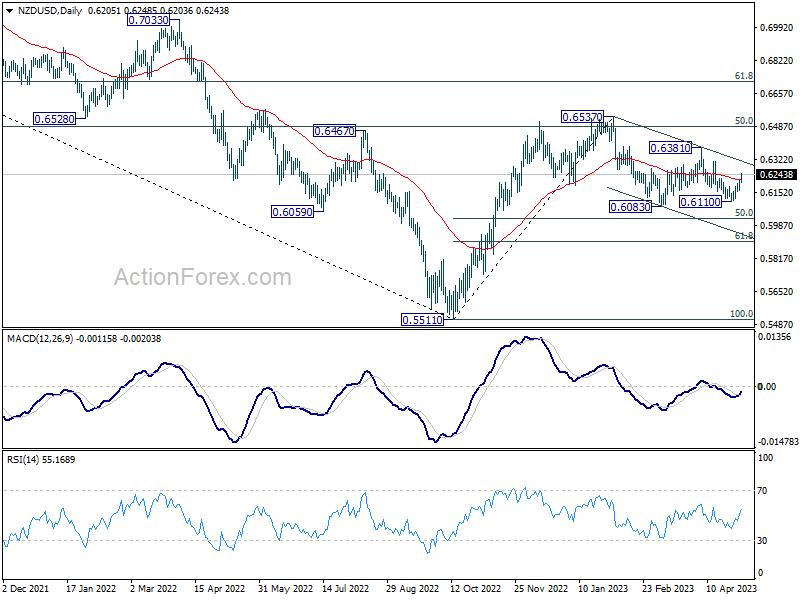

Technically, NZD/USD’s fall from 0.6381 should have completed at 0.6110 already, and further rise is now in favor back towards this resistance. The favored case is that current rise is merely the third leg of the sideway pattern from 0.6083. Outlook remains bearish as long as 0.6381 resistance holds, for resumption of the corrective decline from 0.6537 at a later stage. Break of 0.6160 minor support should bring deeper fall through 0.6083.

Nevertheless, firm break of 0.6381 will argue that the correction from 0.6537 has completed, and the whole rally from 0.5511 might then be ready to resume through 0.6537 high.

New Zealand employment growth exceeds expectations; unemployment rate remains low

New Zealand employment data for Q1 showcased a 0.8% qoq increase, surpassing expectation of 0.4% qoq growth. Unemployment rate remained steady at 3.4%, defying expectations of rise to 3.5% and staying close to record low of 3.2% made in Q1 2022. Additionally, employment rate climbed from 69.3% to 69.5%, while labor force participation rate rose from 71.8% to 72.0%. Both employment and participation rates reached their highest levels since records began in 1986.

All sector wage inflation was at 1.0%, 4.3% yoy. “Annual wage cost inflation is at its highest level since the series began in 1992, up from 4.1 percent in the year to the December 2022 quarter,” business prices manager Bryan Downes said. “This aligns with other wage measures, like the unadjusted LCI and average hourly earnings, both of which also had the largest annual increases on record.”

New Zealand’s financial system well-positioned for higher interest rate environment

In May 2023 Financial Stability Report, RBNZ Governor Adrian Orr highlighted that the country’s financial system is well-placed to handle the higher interest rate environment and international financial disruptions. Global inflation continues to persist at levels significantly above central banks’ policy targets. Although central banks have recently slowed pace of tightening, the full impact of previous tightening measures remains to be seen.

Governor Orr explained that “to date there have been limited signs of distress in banks’ lending portfolios, with only a small share of borrowers falling behind on their payments.” This resilience, he said, reflects ongoing strength of the labor market and the ability of borrowers to adjust their spending or use previous savings and repayment buffers.

Australian retail sales exceed expectations, rising 0.4% mom in Mar

Australia’s retail sales turnover increased by 0.4% mom to AUD 35.3m in March, surpassing expectations of 0.2% mom. Year-on-year, sales turnover was up by 5.4% compared to the same month a year ago.

Ben Dorber, Australian Bureau of Statistics Head of Retail Statistics, noted that while retail sales recorded a third consecutive rise in March, pull-back in spending on discretionary goods has kept monthly turnover at a similar level to six months ago.

Dorber also noted the importance of analyzing quarterly retail sales volumes, set to be released next week, in order to understand the impact of consumer prices on recent turnover growth, particularly as CPI data showed high inflation levels despite slower growth in March quarter.

Fed to hike 25bps today, but pause afterwards?

Fed is widely anticipated to deliver another 25bps rate hike today, bringing federal funds rate target to 5.00-5.25%. Despite ongoing concerns over regional banks in the US, Fed appears unconcerned about overall financial stability. Service prices remain sticky, even as inflation appears to be declining.

With market pricing in near 90% chance of the 25 bps move, surprises seem unlikely. However, after this increase, fed fund futures indicate an almost 100% chance of no change in June, with the path beyond that trending downward. Fed Chair Jerome Powell may stay non-committal in the post-meeting press conference, and point to June’s new economic projections for guidance. But a more explicit pause signal could boost risk markets.

Here are some readings on FOMC:

- Fed Hike, Then What?

- Will the Fed Hike Rates for the Last Time?

- Fed Preview: One More Hike – Cuts Still Far Away

- April Flashlight for the FOMC Blackout Period: Is the Tightening Cycle Coming to an End?

As for US stocks, despite initial selloff yesterday, major indexes recovered some ground and close down around -1% only. NASDAQ is still struggling to break through 12269.55 resistance. But near term bias will remain on the upside as long as 11798.77 support holds. The real test lies in 38.2% retracement of 16212.22 to 10102.61 at 12436.48. Decisive break there will be a solid bullish sign that should push for at least a test on 13181.08 cluster resistance. Nevertheless, firm break of 11798.77 support could prompt near term reversal, and steeper selloff back to 10982.80 support and possibly below.

On the data front

Eurozone unemployment rate will be a main feature in European session. US will release ADP employment and ISM services.

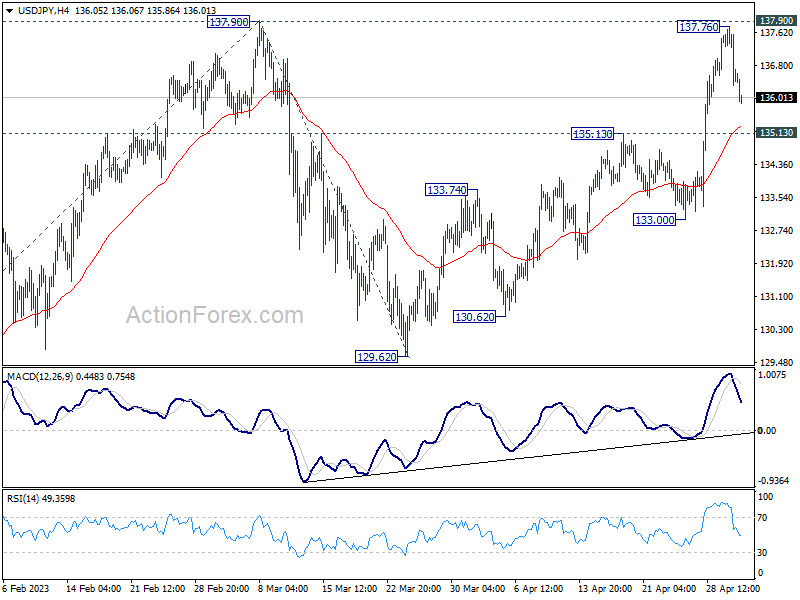

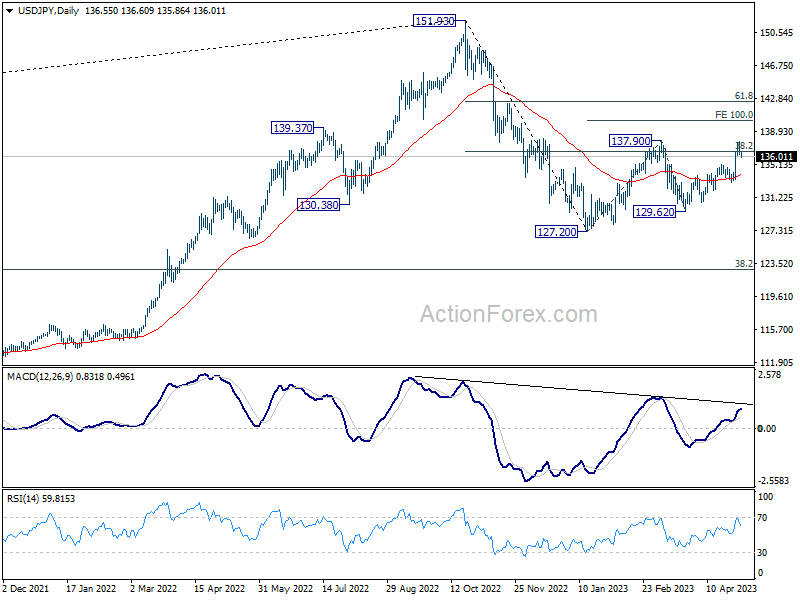

USD/JPY Daily Outlook

Daily Pivots: (S1) 135.43; (P) 136.00; (R1) 136.88; More…

With current retreat, a temporary top is formed in USD/JPY at 137.76, ahead of 137.90 resistance. Intraday bias is turned neutral for some consolidations first. Further rally will remain in favor as long as 135.13 resistance turned support holds. Decisive break of 137.90 will resume whole rebound from 127.20, and target 100% projection of 127.20 to 137.90 from 129.62 at 140.32. However, firm break of 135.13 will turn bias back to the downside for 133.00 support and below.

In the bigger picture, price actions from 151.93 high are currently seen as a corrective pattern to the long term up trend. The first leg should have completed at 127.20. Rebound from there is seen as the second leg. Sustained break of 31.8% retracement of 151.93 to 127.20 at 136.34 will bring stronger rebound to 61.8% retracement at 142.48. Meanwhile, break of 129.62 will argue that the third leg is starting through 127.20 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Employment Change Q1 | 0.80% | 0.40% | 0.20% | |

| 22:45 | NZD | Unemployment Rate Q1 | 3.40% | 3.50% | 3.40% | |

| 22:45 | NZD | Labour Cost Index Q/Q Q1 | 0.90% | 1.10% | 1.10% | |

| 01:30 | AUD | Retail Sales M/M Mar | 0.40% | 0.20% | 0.20% | |

| 08:00 | EUR | Italy Unemployment Rate Mar | 8.10% | 8.00% | ||

| 09:00 | EUR | Eurozone Unemployment Rate Mar | 6.60% | 6.60% | ||

| 12:15 | USD | ADP Employment Change Apr | 150K | 145K | ||

| 13:45 | USD | Services PMI Apr F | 53.7 | 53.7 | ||

| 14:00 | USD | ISM Services PMI Apr | 53.1 | 51.2 | ||

| 14:30 | USD | Crude Oil Inventories | -0.5M | -5.1M | ||

| 18:00 | USD | Fed Interest Rate Decision | 5.25% | 5.00% | ||

| 18:30 | USD | FOMC Press Conference |

{kind=link}