The financial markets are rather steady in Asian session today, showing little reaction to the brief “uprising” in Russia. Major indexes generally traded in tight range, with the exception of China which is just catching up the holidays on Thursday and Friday. In the currency markets, Aussie is the worst performer for now, followed by Kiwi by a distant. Yen is the stronger one, followed by Canadian. But overall, other than a few Aussie pairs, major pairs and crosses are bounded inside Friday’s range.

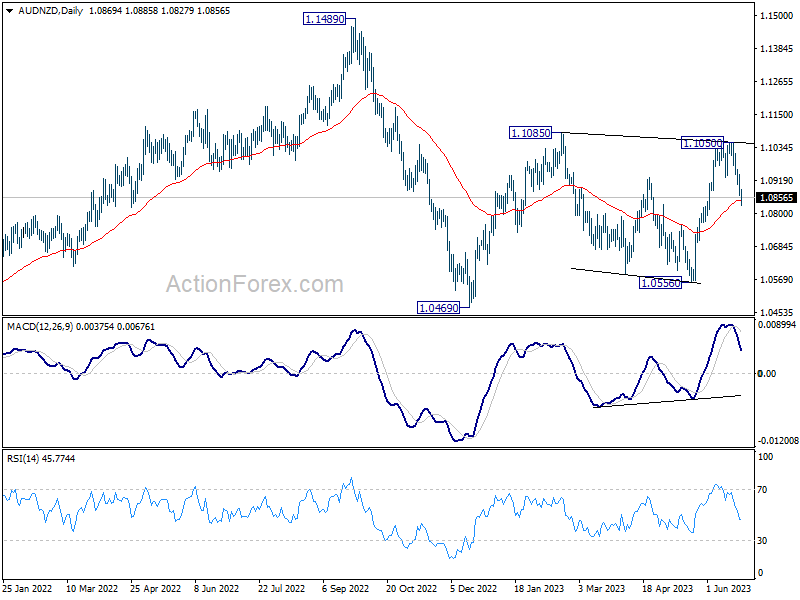

Technically, AUD/NZD’s decline from 1.1050 extended lower today and it’s now pressing 55 D EMA (now at 1.0846). Sustained trading below the EMA would pave the way down towards 1.0556 support. For now, break of 1.0469 is not envisaged unless further downside acceleration is seen. However, if this scenario does come to fruition, a deeper fall in AUD/NZD could potentially hinder the recovery of Aussie elsewhere.

In Asia, Nikkei closed down -0.25%. Hong Kong HSI is down -0.40%. China Shanghai SSE is down -1.51%. Singapore Strait Times is up 0.02%. Japan 10-year JGB yield is down further by -0.126 at 0.359.

Japan’s top officials voice concern over ‘rapid and one-sided’ yen moves

In the face of Yen’s swift depreciation, top Japanese currency diplomat Masato Kanda expressed concern on Monday, describing the recent changes as “rapid and one-sided. He added that “We have all options available and we are not ruling out any options.”

Kanda, Vice Finance Minister for International Affairs, however, refrained from using the phrase “decisive action,” a term he used before Japan intervened in the currency market last year. This careful choice of words suggests that while officials are monitoring the situation, they may not be ready to step in just yet.

Adding to this sentiment, Finance Minister Shunichi Suzuki highlighted the ongoing vigilance of the government, stating that “we will continue to watch the forex market with a sense of urgency.”

In keeping with this sense of readiness, Suzuki assured that authorities would respond “appropriately” to any excessive currency swings, indicating that the government is primed to intervene if necessary.

BoJ opinions: Persistent monetary easing stance upheld, first call YCC Debate

Summary of opinions from BoJ Monetary Policy Meeting on June 15-16 shed light on the prevailing sentiment among policymakers regarding the nation’s current monetary easing stance.

Among the opinions expressed, there was an evident call for maintaining the current monetary easing policy to support rising wage growth, which was described as “the highest in around 30 years.”

Board members noted, “In order to achieve the price stability target of 2 percent in a sustainable and stable manner, price rises accompanied by wage increases, rather than those caused by cost-push factors, are necessary.”

The Bank was thus urged to “keep supporting such momentum for wage hikes through continuation of the current monetary easing.”

Significantly, there was a focus on the potential risks associated with premature policy revisions. It was stated, “It would be premature to revise monetary policy if it would hinder such developments,” referring to increasing wage and investment willingness among small and medium-sized firms.

Policymakers also warned against a “hasty policy change” that could miss the chance to achieve the price stability target.

However, one board member signaled a notable dissent, explicitly calling for an early discussion about tweaking the BoJ’s yield curve control (YCC) – a tool for monetary easing.

This marked the first time a BOJ summary displayed a member’s open expression for an early debate on modifying the YCC, hinting at possible future shifts in the Bank’s policy discussions.

SNB: Monetary policy isn’t tight enough to anchor price stability

In a radio interview with public broadcaster SRF, SNB President Thomas Jordan subtly hinted at the potential need for a tighter monetary policy. This comes on the heels of the Swiss central bank’s recent interest rate hike, which saw an increase of 25 basis points to 1.75% last Thursday.

Interpreting SNB’s inflation forecasts, Jordan said, “If you look at our inflation forecasts and interpret them correctly, then you’ll see that from today’s perspective monetary policy possibly isn’t tight enough to anchor price stability.”

Acknowledging the inevitable, Jordan added, “We can’t completely prevent second-round effects — that would be an illusion — but we have to fight them.” These second-round effects typically refer to changes in wages and prices in response to initial inflationary shocks, underlining the broader impact of inflation on the economy.

Inflation figures and sentiment data: Main attractions for final week of H1

As we approach the final week of the first half of the year, markets will be keenly watching a deluge of consumer inflation data that will likely dictate future monetary tightening policies. Core PCE figures from US, Eurozone’s CPI flash estimate, and CPI from both Canada and Australia stand out as key barometers that their respective central banks will use to gauge the needed extent of further monetary tightening.

Additionally, the pulse of consumer and business sentiment will also come under scrutiny, with US consumer confidence, Germany’s Ifo business climate index, and New Zealand’s ANZ business confidence all on the docket. Moreover, PMI figures from China are set to offer insights into the country’s recovery trajectory and could provoke volatility in Asian and commodity markets.

Here are some highlights for the week:

- Monday: BoJ summary of opinions, Japan corporate services prices; Germany Ifo business climate.

- Tuesday: Canada CPI; US durable goods orders, house price index, consumer confidence, new home sales.

- Wednesday: Australia monthly CPI; Germany Gfk consumer sentiment; Eurozone M3 money supply; Swiss Credit Suisse economic expectations; US goods trade balance.

- Thursday: Japan retail sales, consumer confidence; New Zealand ANZ business confidence; Australia retail sales; Germany CPI flash; Eurozone monthly bulletin; UK M4 money supply, mortgage approvals; US GDP final, jobless claims, pending home sales.

- Friday: Japan Tokyo CPI, unemployment rate, industrial production, housing starts; Australia private sector credit; China PMIs; Germany import prices, retail sales; UK current account, GDP final; Swiss retail sales, KOF economic barometer; France consumer spending; Germany unemployment; Eurozone CPI flash, unemployment rate; Canada GDP, US personal income and spending and PCE price index, Chicago PMI.

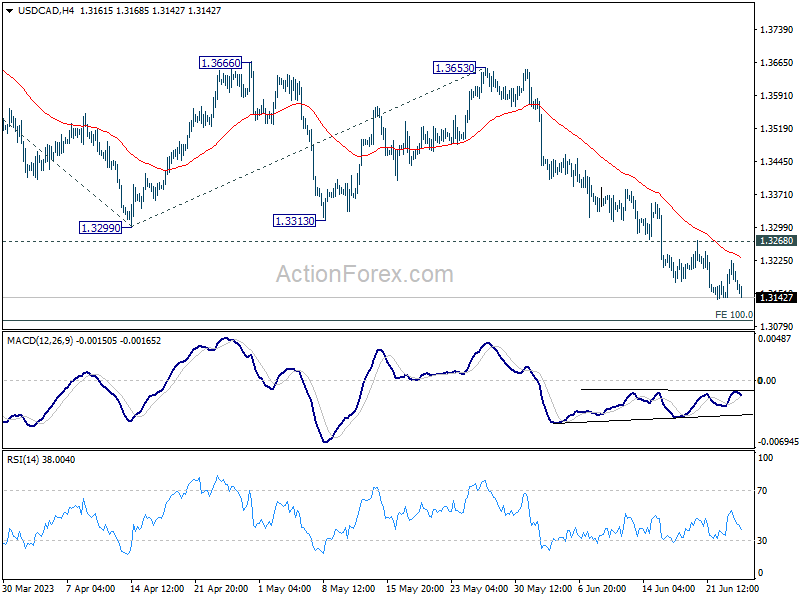

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3141; (P) 1.3183; (R1) 1.3224; More….

Further decline is expected in USD/CAD with 1.3268 resistance intact. Current fall from 1.3653 should target 100% projection of 1.3860 to 1.3299 from 1.3653 at 1.3092. Decisive break there will target 161.8% projection at 1.2745. On the upside, however, break of 1.3268 resistance should now indicate short term bottoming, and turn bias back to the upside for rebound.

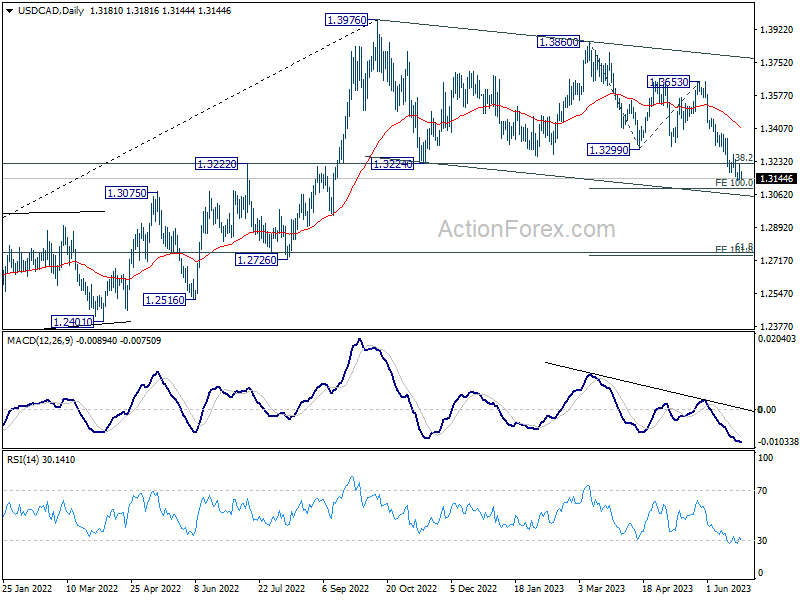

In the bigger picture, price actions from 1.3976 are still viewed as a correction to up trend from 1.2005 (2021 low), but chance of trend reversal is increasing with current decline. In either case, sustained trading below 38.2% retracement of 1.2005 to 1.3976 at 1.3233 will pave the way to 61.8% retracement at 1.2758. Risk will stay on the downside as long as 1.3299 support turned resistance holds, even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y May | 1.60% | 1.80% | 1.60% | |

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 08:00 | EUR | Germany IFO Business Climate Jun | 91.2 | 91.7 | ||

| 08:00 | EUR | Germany IFO Current Assessment Jun | 93.5 | 94.8 | ||

| 08:00 | EUR | Germany IFO Expectations Jun | 88 | 88.6 |

{kind=link}