Today’s currency market sees Euro gaining some traction, especially against Japanese Yen, which is underperforming alongside Australian Dollar. Despite RBA’s hinting at a potential rate hike, Aussie is struggling, not only against major currencies but also against its commodity-linked counterparts. British Pound, too, is lagging behind despite UK reporting GDP figures marginally above expectations. Dollar is showing signs of firmness but is unable to muster a strong momentum to significantly build upon this week’s recovery efforts.

In commodity markets, Gold is slipping below 1950 handle again. WTI crude oil is experiencing stagnation, hovering around 76 mark, following a notable decline earlier in the week. While US 10-year Treasury yield showcased an impressive bounce yesterday, it has not managed to maintain the upward trajectory, suggesting caution among bond investors.

A more optimistic note is seen in cryptocurrency market, where Bitcoin and Ethereum are showing significant bullish momentum. Bitcoin has successfully broken 37k mark, while Ethereum has powered through 2000 level, signaling intensifying investor interest in digital assets.

Technically, Ether now looks set to break through 2141.75 resistance to resume the whole rebound from 878.50. Key resistance level lies in 38.2% retracement of 4863.75 to 878.50 at 2400.85. (Bitcoin has already broken equivalent fibonacci resistance. Decisive break there could pave the way to 61.8% retracement at 3341.38 in the medium term. In any case, outlook will stay bullish as long as 1849.05 support holds.

In Europe, at the time of writing, FTSE is down -1.31%. DAX is down -0.68%. CAC is down -1.00%. Germany 10-year yield is up 0.0570 at 2.708. Earlier in Asia, Nikkei dropped -0.24%. Hong Kong HSI dropped -1.76%. China Shanghai SSE dropped -0.47%. Singapore Strait Times dropped -0.91%. Japan 10-year JGB yield rose 0.0153 to 0.857.

NIESR forecasts slight growth for UK economy, averting recession in 2023

According to NIESR’s projections, UK economy is set to witness a marginal increase in GDP of 0.1% in the fourth quarter of this year. The institute’s report highlighted, “Our central forecast does not expect a recession in 2023.”

Delving into the specifics of the economic forecast, NIESR stated, “These forecasts remain broadly consistent with the longer-term trend of low, but stable economic growth in the United Kingdom.”

Looking ahead to the next two years, NIESR expects the pace of growth to remain relatively subdued. The institute’s report forecasts GDP growth of 0.6% for 2023, followed by further restrained growth of 0.5% in 2024. The primary cause for this muted growth, as per NIESR, is the ongoing productivity slump.

UK economy shows resilience: GDP up 0.2% mom in Sep, flat in Q3

UK’s economy displayed unexpected resilience in today’s data releases, GDP figures surpassed market expectations both on a monthly and quarterly basis.

In September, GDP grew by 0.2% mom, defying the stagnation prediction of 0.0% mom. This growth was primarily driven by a 0.2% increase in the services sector, a crucial component of the UK economy. Additionally, the construction sector contributed positively with a 0.4% mom= growth, while production remained steady with no significant change.

On a quarterly scale, GDP figures remained flat at 0.0%, which is a more favorable outcome compared to the anticipated contraction of -0.1% qoq. On a year-on-year basis, GDP registered a growth of 0.6% yoy, indicating a modest but steady recovery from the same quarter in the previous year.

The services sector experienced a slight contraction of -0.1% qoq, whereas construction saw a marginal growth of 0.1% qoq. The production sector’s performance was broadly unchanged.

RBA’s hawkish SoMP points to another rate hike

RBA’s latest Statement on Monetary Policy presents a more hawkish picture than market observers anticipated, with upward revisions in both headline and underlying inflation projections, alongside stronger growth outlook.

More importantly, these projections rest on the assumption that cash rate will peak around 4.50%, comparing to the current 4.35%, suggesting another rate hike could be imminent.

RBA’s heightened vigilance against inflation is clear: “The weight of recent information suggests that the risk of inflation remaining higher for longer has increased,” the bank stated, highlighting domestic inflation persistence and possible global factors, such as energy market disruptions and food price hikes tied to El Niño effects.

Economic projections now show a year-average GDP growth expected to hit 2.00% in 2023, rising to 1.75% in 2024, and reaching 2.25% in 2025. These figures mark an upgrade from June’s forecast of 1.50%, 1.25%, and 2.00% respectively, suggesting a resilient economy that could withstand tighter monetary policy.

Inflation forecasts have also been adjusted upward, with headline CPI inflation now seen at 4.50% at the year’s end in 2023, followed by 3.50% in 2024, and softening to 3.00% in 2025. They are upgraded from 4.25%, 3.25% and 2.75% respectively.

The trimmed mean inflation follows a similar upward trajectory, projected to be at 4.50% in year-ended 2023, 3.25% in 2024, and 3.00% in 2025, up from prior forecast of 4.00%, 3.00%, and 2.75% respectively.

Underpinning these projections are technical assumptions of a cash rate peaking at around 4.50%, with a gradual decline to approximately 3.50% by the end of 2025, indicating a higher rate path than previously used.

NZ BNZ PMI fell to 42.5, manufacturing downturn reaches lowest point since 2009

October has marked a significant downturn for New Zealand’s manufacturing sector, with BusinessNZ Performance of Manufacturing Index plummeting from 45.1 to 42.5. This figure not only represents the fifth consecutive month of declining activity but also stands as the lowest activity level for a month unaffected by COVID-19 restrictions since May 2009, deeply underscoring the sector’s distress.

Delving into the components, the bleak picture becomes clearer: Production has taken a hit, sliding down from 44.3 to 41.5, and employment in the sector is also suffering, with a drop from 45.1 to 43.3. New orders barely held ground, marginally decreasing from 44.8 to 44.1. A significant retreat was seen in finished stocks, which contracted from 51.2 to 45.7, and deliveries were also on the downturn from 44.3 to 42.9.

Amidst these figures, the voice of the industry has tilted towards concern, with 65.1% of comments categorized as negative, albeit slightly less pessimistic than previous months, at 68.8% in September and 66.7% in August.

BNZ Senior Economist, Doug Steel, highlighted the potential ramifications for the broader economy: “Today’s PMI is not a good look for GDP and employment growth,” he noted. With the current forecasts including a downturn in manufacturing for the latter half of 2023, Steel warned, “There’s a chance that decline is bigger than we think, if the PMI does not bounce in the final months of the year.”

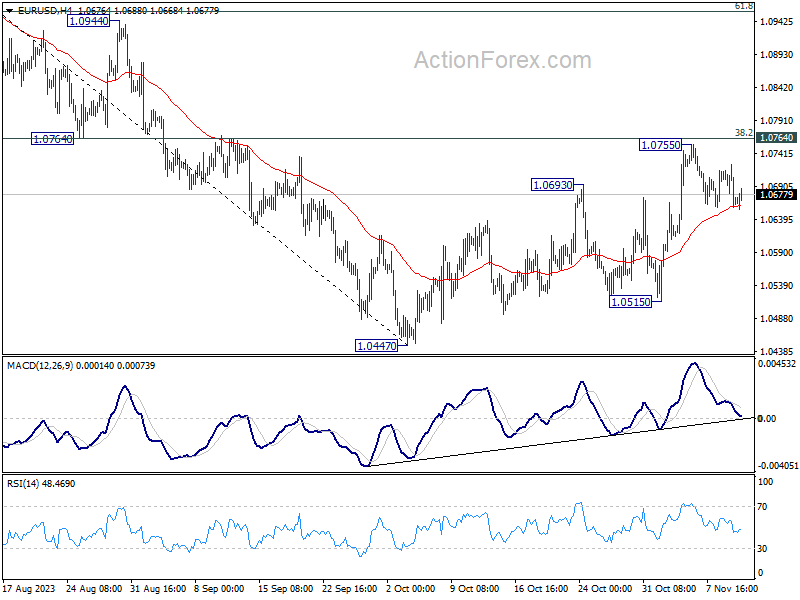

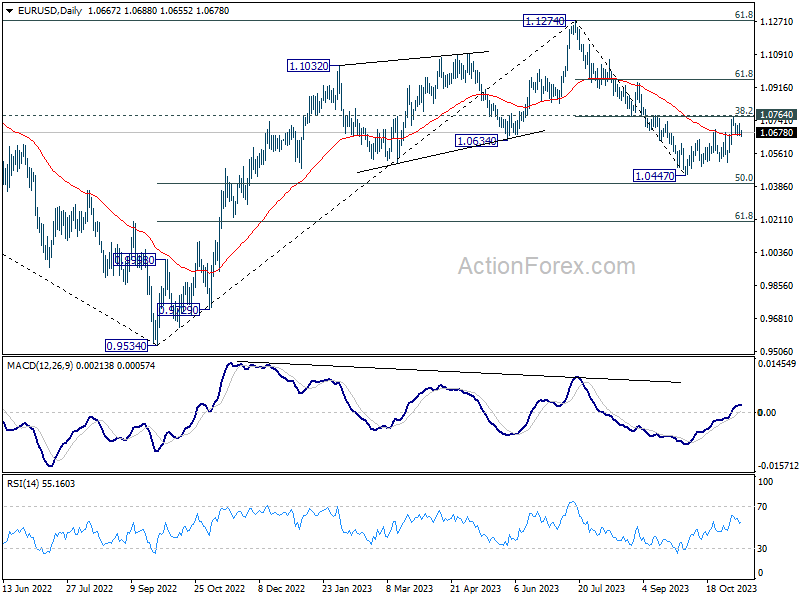

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0644; (P) 1.0685; (R1) 1.0709; More…

EUR/USD is trying to draw support from 55 4H EMA (now at 1.0657) and intraday bias remains neutral first. Further rise is in favor as long as this EMA holds. Decisive break of 1.0764 cluster resistance (38.2% retracement of 1.1274 to 1.0447 at 1.0763) will extend the rise from 1.0447 to 61.8% retracement at 1.0958 next. However, sustained break of 55 4H EMA will argue that the rebound has completed, and target 1.0515 support, and then 1.0447 low.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PMI Oct | 42.5 | 45.3 | 45.1 | |

| 23:50 | JPY | Money Supply M2+CD Y/Y Oct | 2.40% | 2.40% | ||

| 00:30 | AUD | RBA Monetary Policy Statement | ||||

| 07:00 | GBP | GDP M/M Sep | 0.20% | 0.00% | 0.20% | 0.10% |

| 07:00 | GBP | GDP Q/Q Q3 P | 0.00% | -0.10% | 0.20% | |

| 07:00 | GBP | Manufacturing Production M/M Sep | 0.10% | 0.30% | -0.80% | -0.70% |

| 07:00 | GBP | Manufacturing Production Y/Y Sep | 3.00% | 3.10% | 2.80% | 3.00% |

| 07:00 | GBP | Industrial Production M/M Sep | 0.00% | -0.10% | -0.70% | -0.50% |

| 07:00 | GBP | Industrial Production Y/Y Sep | 1.50% | 1.10% | 1.30% | 1.50% |

| 07:00 | GBP | Goods Trade Balance (GBP) Sep | -14.3B | -15.3B | -16.0B | -15.5B |

| 09:00 | EUR | Italy Industrial Output M/M Sep | 0.00% | -0.10% | 0.20% | 0.30% |

| 12:00 | GBP | NIESR GDP Estimate (3M) Oct | 0.10% | -0.10% | 0.00% | |

| 15:00 | USD | Michigan Consumer Sentiment Index Nov P | 63.6 | 63.8 |

{kind=link}