Dollar remains subdued in the aftermath of its significant selloff triggered by CPI release overnight. Market sentiment has swiftly shifted, with the majority now almost ruling out the possibility of further rate hikes by Fed. This shift indicates a growing consensus that current federal funds rate of 5.25-5.50% marks the peak of this cycle.

Moreover, traders are increasingly speculating more boldly on the timing of rate cuts, with approximately 30% chance by the end of Q1 and over 80% probability by the end of the first half of the next year. This speculation is primarily driven by the belief that Fed might pivot to easing policies sooner if economic data continues to show signs of a downturn.

The impact of these expectations is evident across various markets. Notably, NASDAQ led a robust closing in major indexes, and the 10-year yield experienced a significant decline, losing nearly -0.2%. Looking back, the psychological level of 5% yields seemed to have attracted significant treasury buying interest. Future data that underperforms could spur an even more pronounced dip in yields, and intensifying expectation of Fed’s pivot to rate cuts in 2024.

In the foreign exchange markets, Australian and New Zealand Dollars have emerged as the primary beneficiaries of Dollar’s weakness, leading the performance charts for the week. This strength is amplified by positive sentiment flowing through Asian markets. British Pound, known for its sensitivity to shifts in risk sentiment, has also performed strongly, while Euro trails closely behind. Conversely, Japanese Yen and Swiss Franc, despite their appreciable gains against Dollar, have not matched the momentum seen in other major currencies.

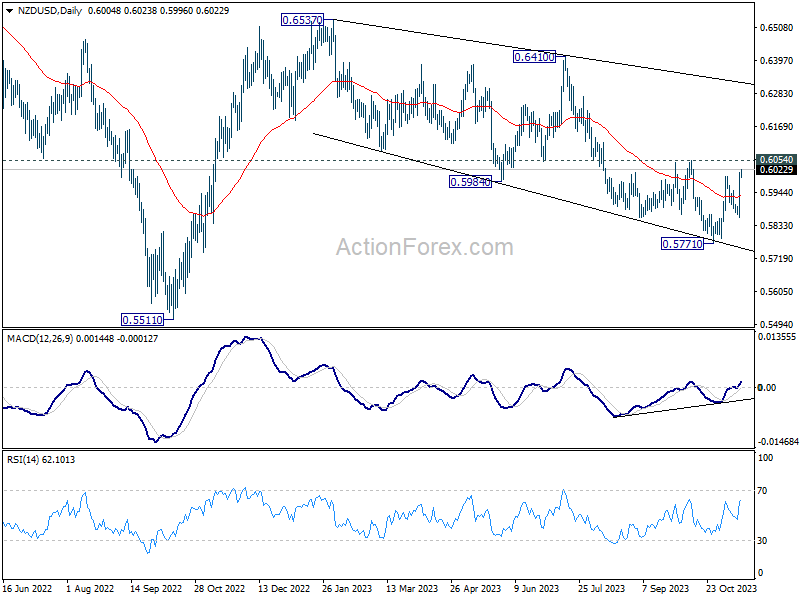

From a technical perspective, a key question is whether NZD/USD and AUD/USD’s down trend since February has already completed in October. Focus is now on 0.6054 resistance in NZD/USD (corresponding level of 0.6510 in AUD/USD) for the near term. Decisive break of 0.6054 will argue that the fall from 0.6537 has completed with three waves down to 0.5771. That would change near term outlook bullish for at least a take on falling trend resistance (now at 0.6318). Synchronized rallies in NZD/USD and AUD/USD will reinforce each other.

In Asia, at the time of writing, Nikkei is up 2.28%. Hong Kong HSI is up 2.83%. China Shanghai SSE is up 0.45%. Singapore Strait Times is up 0.50%. Japan 10-year JGB yield is down -0.077 at 0.779. Overnight, DOW rose 1.43%. S&P 500 rose 1.91%. NASDAQ rose 2.37%. 10-year yield fell -0.191 to 4.441.

Fed’s Goolsbee eyes housing as crucial for continued disinflation progress

Chicago Fed President Austan Goolsbee acknowledged yesterday that “progress continues towards 2% inflation target. He highlighted the decline in goods inflation, but points out the critical role of housing inflation in the coming quarters.

Goolsbee emphasized, “With goods inflation already coming down and nonhousing services inflation typically slow to adjust, the key to further progress over the next few quarters will be what happens to housing inflation.”

Separately, Richmond Fed President Thomas Barkin exhibited a more guarded stance. He expresses doubts about a smooth transition to the Fed’s inflation target, underscoring the complexity of the current economic scenario.

Barkin noted, “I’m just not convinced that inflation is on some smooth glide path down to 2%.” He acknowledges the recent decrease in inflation rates but attributes it primarily to the partial reversal of spikes seen during the Covid era, driven by high demand and supply constraints.

Barkin further points out that certain sectors, such as shelter and services, continue to exhibit inflation rates above historical norms.

Japan’s GDP down -0.5% qoq, -2.1% annualized in Q3

Japan’s GDP contracted -0.5% qoq in Q3, starkly underperformed market expectations of -0.1% qoq decline. On annualized basis, the situation appears even more drastic, with the economy shrinking by -2.1%, far exceeding anticipated -0.6% contraction, and being the worst since Q3 2021.

A critical factor in this downturn was a -0.6% decrease in business investment, marking a continuous decline for two consecutive quarters. This reduction was primarily influenced by reduced spending on semiconductor production equipment, reflecting broader challenges in global tech sector.

Additionally, private consumption, a key driver of economic activity, saw a marginal fall of -0.04%. This marks the second successive quarter of decline, with slump in vehicle sales significantly impacting consumer spending.

China’s industrial and retail growth surpass expectations, PBOC injects fresh funds

China’s industrial output and retail sales for October exceeded market expectations. Industrial production rose 4.6% yoy, surpassing forecasted 4.5% yoy, marking an improvement from September’s 4.5% yoy growth. Retail sales recorded a robust 7.6% yoy growth, significantly higher than anticipated 7.0% yoy and showing a considerable improvement from 5.5% yoy increase in September.

However, fixed asset investment experienced slower growth, rising only 2.9% ytd yoy, which was below the expected 3.1%. The real estate sector particularly faced challenges, with investment dropping by -9.3% ytd yoy, a deterioration compared to the previous period through September.

In a separate development, People’s Bank of China maintained interest rate on CNY 1.45T worth of one-year medium-term lending facility loans at 2.50%, consistent with previous operations. As CNY 850B worth of MLF loans were set to expire this month, this move resulted in a net injection of CNY 600B of fresh funds into the banking system.

The central bank stated that this loan operation aimed to keep the banking system’s liquidity at a reasonably ample level, countering short-term factors such as tax payments and government bond issuances.

Looking ahead

UK CPI is the main focus in European while PPI and RPI will also be released. Eurozone trade balance and industrial production will be featured too.

Later in the day, US retail sales will be the main focus, along with PPI and Empire stat manufacturing index. Canada will release manufacturing sales and wholesale sales.

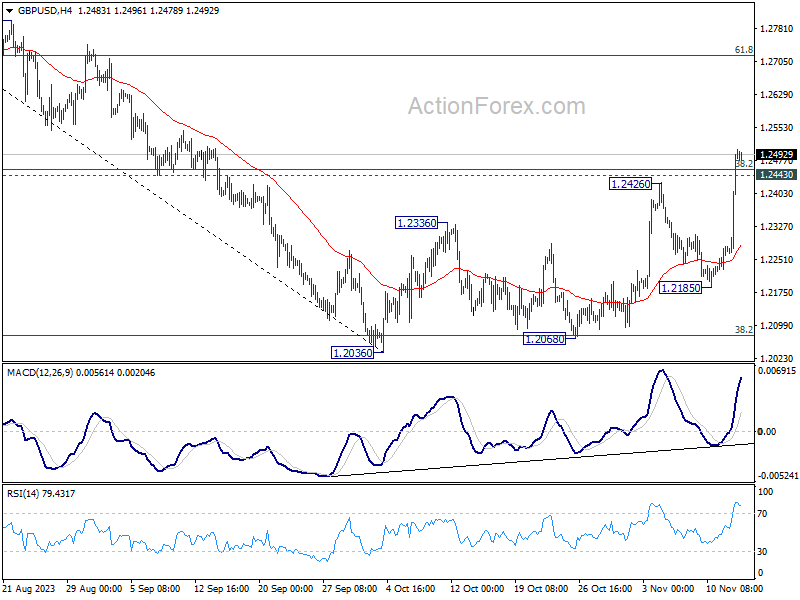

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2337; (P) 1.2421; (R1) 1.2583; More…

GBP/USD’s rally extends to as high as 1.2504 so far. Intraday bias remains on the upside at this point. Sustained trading above 38.2% retracement of 1.3141 to 1.2036 at 1.2458 will pave the way to 61.8% retracement at 1.2716. On the downside, below 1.2443 minor support will turn intraday bias neutral and bring retreat. But downside should be contained well above 1.2185 support to bring another rally.

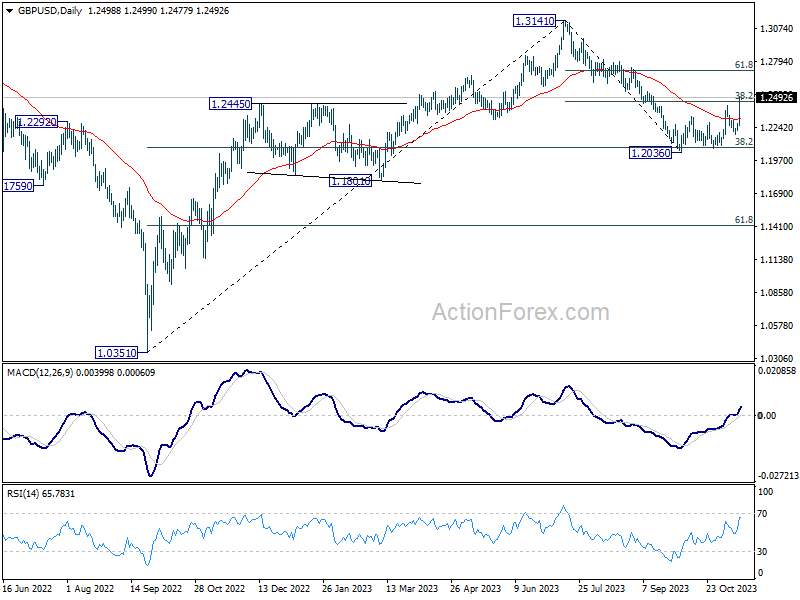

In the bigger picture, price actions from 1.3141 are seen as a corrective pattern to rise from 1.0351 (2022 low). Strong rebound from 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 will argue that current rise from 1.2036 is already the second leg. However, while further rally could be seen, upside should be limited by 1.3141 to bring the third leg of the pattern.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Wage Price Index Q/Q Q3 | 1.30% | 1.30% | 0.80% | 0.90% |

| 23:50 | JPY | GDP Q/Q Q3 P | -0.50% | -0.10% | 1.20% | |

| 23:50 | JPY | GDP Deflator Y/Y Q3 P | 5.10% | 4.80% | 3.50% | |

| 02:00 | CNY | Industrial Production Y/Y Oct | 4.60% | 4.50% | 4.50% | |

| 02:00 | CNY | Retail Sales Y/Y Oct | 7.60% | 7.00% | 5.50% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Oct | 2.90% | 3.10% | 3.10% | |

| 04:30 | JPY | Industrial Production M/M Sep F | 0.50% | 0.20% | 0.20% | |

| 07:00 | GBP | CPI M/M Oct | 0.20% | 0.50% | ||

| 07:00 | GBP | CPI Y/Y Oct | 4.70% | 6.70% | ||

| 07:00 | GBP | Core CPI Y/Y Oct | 5.80% | 6.10% | ||

| 07:00 | GBP | RPI M/M Oct | 0.50% | |||

| 07:00 | GBP | RPI Y/Y Oct | 6.40% | 8.90% | ||

| 07:00 | GBP | PPI Input M/M Oct | 0.10% | 0.40% | ||

| 07:00 | GBP | PPI Input Y/Y Oct | -2.60% | |||

| 07:00 | GBP | PPI Output M/M Oct | 0.10% | 0.40% | ||

| 07:00 | GBP | PPI Output Y/Y Oct | -0.10% | |||

| 07:00 | GBP | PPI Core Output M/M Oct | 0.00% | |||

| 07:00 | GBP | PPI Core Output Y/Y Oct | 0.70% | |||

| 10:00 | EUR | Eurozone Trade Balance (EUR) Sep | 12.3B | 11.9B | ||

| 10:00 | EUR | Eurozone Industrial Production M/M Sep | -0.90% | 0.60% | ||

| 13:30 | CAD | Manufacturing Sales M/M Sep | 0.80% | 0.70% | ||

| 13:30 | CAD | Wholesale Sales M/M Sep | 1.40% | 2.30% | ||

| 13:30 | USD | Empire State Manufacturing Index Nov | -2.6 | -4.6 | ||

| 13:30 | USD | Retail Sales M/M Oct | -0.30% | 0.70% | ||

| 13:30 | USD | Retail Sales ex Autos M/M Oct | -0.20% | 0.60% | ||

| 13:30 | USD | PPI M/M Oct | 0.10% | 0.50% | ||

| 13:30 | USD | PPI Y/Y Oct | 1.90% | 2.20% | ||

| 13:30 | USD | PPI Core M/M Oct | 0.20% | 0.30% | ||

| 13:30 | USD | PPI Core Y/Y Oct | 2.70% | 2.70% | ||

| 15:00 | USD | Business Inventories Sep | 0.30% | 0.40% | ||

| 15:30 | USD | Crude Oil Inventories |

{kind=link}