New Zealand Dollar falls notably during Asian session, triggered by the latest survey from the RBNZ, which revealed a further easing in inflation expectations. The implications of these findings have prompted traders to pare back the bets on the likelihood of more monetary tightening imminent meeting February. Australian Dollar is also dragged down by the Kiwi and trades as the second weakest for the moment.

Meanwhile, Japanese Yen finds itself on the losing end as well, contributing to the extended rally in Nikkei, which soared to a new 34-year high, breaking past the 37,000 psychological level.

On the contrary, Dollar stands out as the day’s strongest performer for now, with the financial markets on edge for the upcoming US CPI data release. Analysts are forecasting deceleration in headline CPI from 3.4% to 2.9% in January, alongside minor decrease in core CPI from 3.9% to 3.8%.

It should be emphasized that the broadening of disinflation from goods to services sectors remains a critical consideration for Fed. The pace and timing of rate rate cuts hinge on this data. Presently, Fed fund futures indicate a 57% likelihood of a rate cut by May, with the probability exceeding 90% by June.

Elsewhere in the currency markets, Euro is currently the second strongest while Swiss Franc and Sterling are mixed. UK employment and wages down will be a key focus in European session. But Swiss CPI and Germany ZEW economic sentiment could also be market moving.

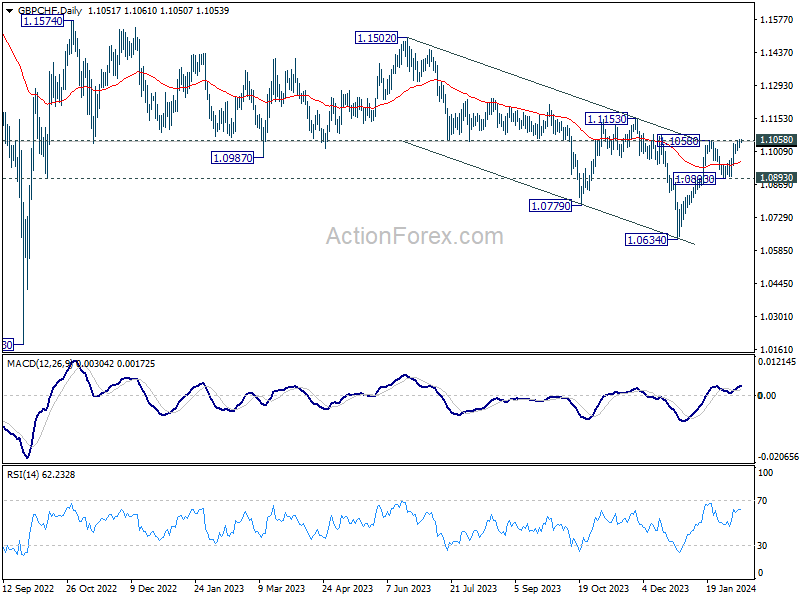

A pair garnering particular interest is GBP/CHF, which is currently pressing 1.1058 resistance level. Decisive break there will resume the whole rebound from 1.0634. More importantly, that would strength the case that whole corrective down trend from 1.1574 ha completed. Further rally would be seen to 1.1153 resistance for confirmation. At the same time, break of 0.8512 support in EUR/GBP will also solidify Sterling’s overall momentum, as least against its European peers.

In Europe, at the time of writing, Nikkei is up 2.88%. Japan 10-year JGB yield is up 0.0042 at 0.729. Singapore Strait Times is down -0.14%. Hong Kong and China are still on holiday. Overnight, DOW rose 0.33%. S&P 500 fell -0.09%. NASDAQ fell -0.30%. 10-year yield fell -0.015 to 4.172.

RBA’s Kohler points to slightly faster than expected inflation decline

Marion Kohler, RBA’s Head of Economic Analysis, noted in a speech that inflation is “still high” but acknowledged a welcome trend: it’s decreasing “at a slightly faster rate” than what RBA had forecasted three months prior.

Looking ahead, RBA’s expectation is for inflation to settle back into its 2-3% target range by 2025 and reach the midpoint by the following year. However, Kohler underscored the “substantial uncertainty” surrounding these long-term predictions.

A notable aspect of Australia’s inflation dynamics, as Kohler pointed out, is the “divergence in the path of core goods and services price inflation.”

The primary driver behind the recent dip in inflation rates is the decrease in goods price inflation, whereas services price inflation remains “high and broadly based.” This sector’s inflation is predicted to “only gradually” diminish as a more equitable demand-supply relationship is established and domestic cost pressures begin to ease.

Kohler also touched on labor costs, particularly significant in the labor-intensive services sector, as a crucial factor influencing the pricing strategies of businesses. RBA believes wage growth is “around its peak” and anticipates a gradual reduction in line with improvements in the labor market. Signs of “easing wage pressures” are already evident in specific industries, notably within business services.

Australia NAB business conditions down to 6, price pressures easing

Australia NAB Business Confidence improved slightly form 0 to 1 in January. Despite this marginal improvement, Business Conditions dropped from 8 to 6, with notable decreases in trading conditions from 11 to 8, profitability conditions from 7 to 5, and employment conditions also falling from 7 to 5.

In terms of cost pressures, labour cost growth remained steady at 2.0% in quarterly equivalent terms, while purchase cost growth saw a slight increase to 1.8% from 1.7%. Product price growth experienced a pickup, moving to 1.2% in quarterly terms from 0.9%, reflecting a broader trend of easing price pressures. Specifically, retail price growth rose to 0.9% from 0.5%, and the growth rate for recreation & personal services prices increased to 1.2% from 0.9%.

NAB Chief Economist Alan Oster commented on the findings, stating, ” Capacity utilisation remains high, despite the slowing in growth over the second half of 2023, and price pressures are easing, with hopes they settle well below where they are now.”

Australian Westpac consumer sentiment hits 20-Month high, but still pessimistic

Australia Westpac Consumer Sentiment Index surged by 6.2% mom to 86 in February, marking the highest level since June 2022. This increase also represents the largest monthly gain since April of the previous year, which conincided with a period when RBA temporarily halted its tightening cycle.

According to Westpac, the surge in consumer sentiment was notably propelled by improved sentiment towards major purchases, which climbed 11.3% to 86.8, and more optimistic outlook for the economy over the next year, rising 8.8% to 88.9—the highest since May 2022. Additionally, five-year economic outlook rose 4.4% to 93.

The cooling inflation and more favorable perspective on interest rates are believed to be the primary factors behind this uplift. However, despite the recent gains, consumer mood remains in the pessimistic territory.

A notable “sharp turnaround” in sentiment was observed following RBA’s decision in February to maintain the cash rate steady, with sentiment dropping from 94.1 to just 80 post-meeting. While the decision to keep rates unchanged aligned with general expectations, the decline in sentiment suggests consumers were anticipating a “clearer indication” that interest rates might begin to decrease.

Looking forward, Westpac anticipates the RBA will maintain the current interest rate in March, contingent on inflation continuing to align with expectations.

RBNZ survey reveals easing inflation expectations, NZD dips

According to RBNZ’s latest Survey of Expectations, one-year inflation expectation fell by 38 basis points from 3.60% to 3.22%, marking its lowest point since September 2021. The survey also indicates a growing consensus, with more than half of respondents expecting that CPI inflation will fall back to RBNZ’s target range of 1-3% by the end of 2024

Furthermore, the survey pointed to a decrease in inflation expectations over the longer term, with two-year-ahead predictions dropping from 2.76% to 2.50%, and expectations for five and ten years ahead also seeing decline to 2.25% (from 2.43%) and 2.16% (from 2.28%), respectively.

In terms of interest rates, survey participants anticipate OCR to average at 5.46% by the end of March, with projected decrease to 4.74% by the end of the year. The OCR currently stands at 5.50%.

The publication of the survey’s results led to a discernible decline in the NZD, as market participants began to reevaluate the likelihood of another RBNZ rate hikes.

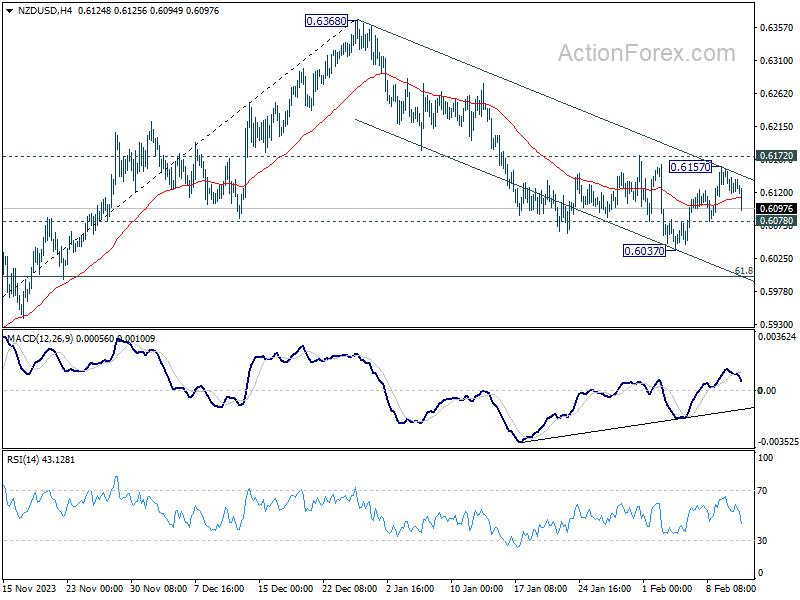

Technically, with 0.6172 resistance intact, recovery from 0.6037 is seen as a correction to the fall from 0.6368 only. Break of 0.6078 minor support will argue that this decline is ready to resume through 0.6037.

ECB’s Cipollone: No further economic slack necessary

In a speech overnight, ECB Executive Board member Piero Cipollone suggested that additional tightening of monetary policy may not be necessary to rein in inflation. His remarks hint at a potentially less restrictive approach going forward, should inflationary pressures continue to subside.

Cipollone emphasized that the current economic conditions, “with demand still weak and inflation expectations anchored”, arguing against the need for monetary policy to “generate further slack to keep inflation in check”. This perspective underlines a significant shift from aggressive tightening to a more measured stance, possibly preparing the ground for a more accommodative monetary policy in the near future.

Unwinding of supply shocks offers room for demand to pick up “without fuelling inflation”. Additionally, the downturn in energy prices could allow for “some wage catch-up, especially if profits normalize.”

However, Cipollone also stressed the importance of a balanced approach to policy-making, pointing out that the path to the ECB’s inflation target would depend on a complex interplay of economic factors. Consequently, he advocated for a “data-driven” approach to future monetary-policy decisions.

Looking ahead

UK employment, Swiss CPI and German ZEW economic sentiment will be released in European session. Later in the day, US CPI will tak center stage.

USD/CHF Daily Outlook

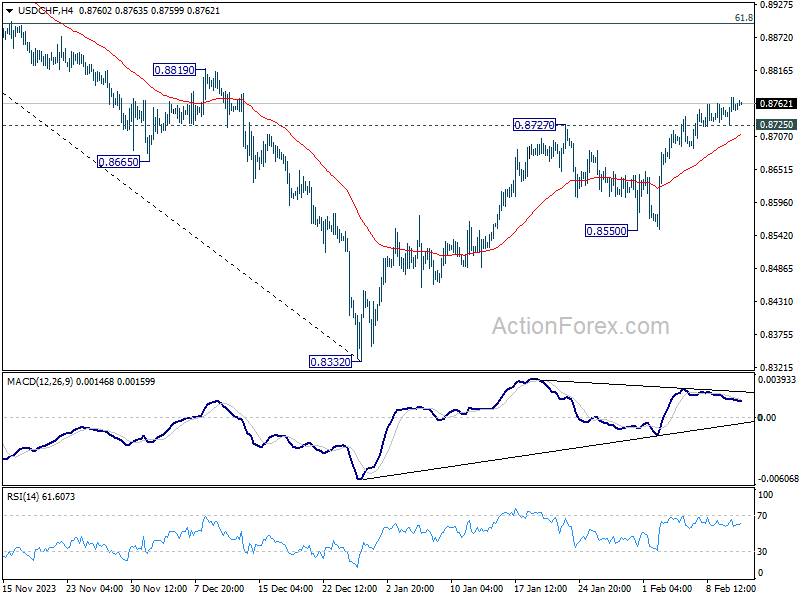

Daily Pivots: (S1) 0.8732; (P) 0.8752; (R1) 0.8778; More….

Intraday bias in USD/CHF remains on the upside despite loss of momentum as seen in 4H MACD. Current rise from 0.8332 should target 61.8% retracement of 0.9243 to 0.8332 at 0.8995. On the downside, below 0.8725 minor support will turn intraday bias neutral first. But near term outlook will stay cautiously bullish as long as 0.8550 support holds.

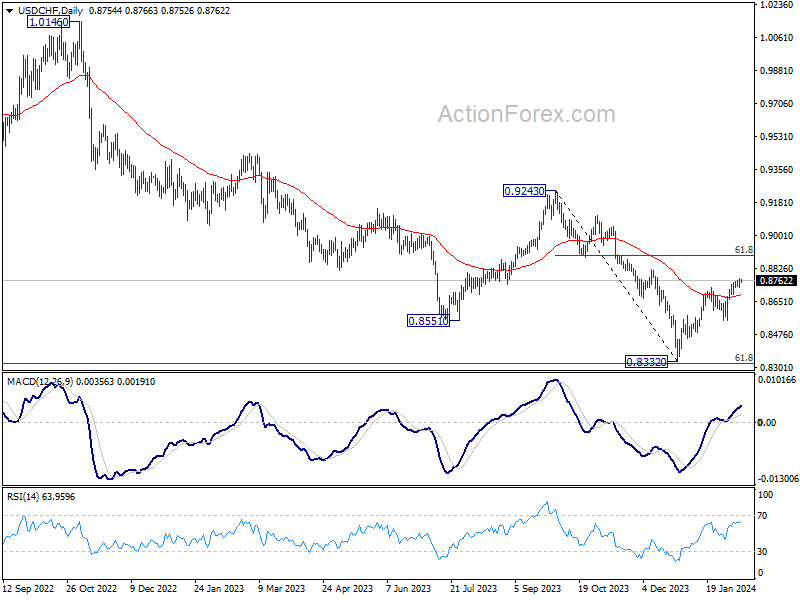

In the bigger picture, sustained trading above 55 D EMA (now at 0.8687) will solidify the case of medium term bottoming at 0.8332, just ahead of 0.8317 long term fibonacci support, on bullish convergence condition in W MACD. Further rise should be seen to 0.9243 resistance, even as a correction to the larger down trend from 1.0146 (2022 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Consumer Confidence Feb | 6.20% | -1.30% | ||

| 23:50 | JPY | PPI Y/Y Jan | 0.20% | 0.10% | 0.00% | 0.20% |

| 00:30 | AUD | NAB Business Confidence Jan | 1 | -1 | ||

| 00:30 | AUD | NAB Business Conditions Jan | 6 | 7 | ||

| 02:00 | NZD | RBNZ Inflation Expectations Q1 | 2.50% | 2.76% | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Jan | -9.90% | |||

| 07:00 | GBP | Claimant Count Change Jan | 15.2K | 11.7K | ||

| 07:00 | GBP | Unemployment rate Dec | 4.00% | 4.20% | ||

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Dec | 5.70% | 6.50% | ||

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Dec | 6.00% | 6.60% | ||

| 07:30 | CHF | CPI M/M Jan | 0.60% | 0% | ||

| 07:30 | CHF | CPI Y/Y Jan | 1.60% | 1.70% | ||

| 10:00 | EUR | Germany ZEW Economic Sentiment Feb | 17.5 | 15.2 | ||

| 10:00 | EUR | Germany ZEW Current Situation Feb | -79 | -77.3 | ||

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Feb | 20.1 | 22.7 | ||

| 11:00 | USD | NFIB Business Optimism Index Jan | 91.1 | 91.9 | ||

| 13:30 | USD | CPI M/M Jan | 0.20% | 0.30% | ||

| 13:30 | USD | CPI Y/Y Jan | 2.90% | 3.40% | ||

| 13:30 | USD | CPI Core M/M Jan | 0.30% | 0.30% | ||

| 13:30 | USD | CPI Core Y/Y Jan | 3.80% | 3.90% |

{kind=link}