The global financial markets are overall very quiet today, marked by a noticeable absence of significant economic data releases or impactful news. Euro emerges as the frontrunner, leading European majors higher, while Yen sees a slight dip in anticipation of Japan’s CPI data set to be released tomorrow. Commodity currencies are on the weaker side, particularly highlighted by New Zealand Dollar’s early sell-off. Dollar, meanwhile, is mixed as it awaits new drivers that could provide fresh momentum.

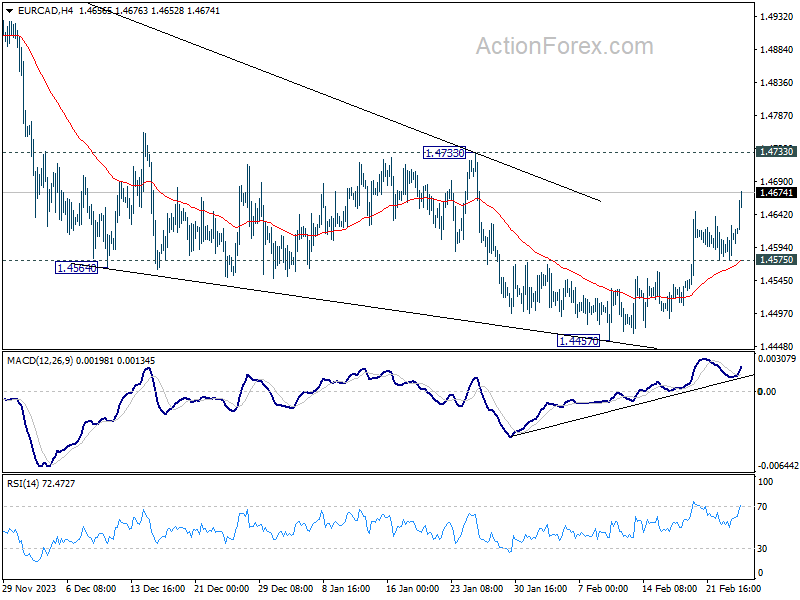

Technically, EUR/CAD’s rebound from 1.4457 resumed today and it’s on track to test 1.4733 resistance. Corrective fall from 1.5041 is seen as completed with three waves down. Rise from 1.4155 is probably resuming. Sustained break of 1.4733 will strengthen this bullish case and target 1.5041 resistance next. This will now remain the favored case long as 1.4575 support holds.

In Europe, at the time of writing, FTSE is down -0.28%. DAX is up 0.07%. CAC is down -0.34%. UK 10-year yield is up 0.0114 at 4.051. Germany 10-year yield is up 0.016 at 2.385. Earlier in Asia, Nikkei rose 0.35%. Hong Kong HSI fell -0.54%. China Shanghai SSE fell -0.48%. Singapore Strait Times fell -0.43%. Japan 10-year yield fell -0.0305 to 0.691.

Nikkei reaches new heights as Yen declines before Japan’s CPI

Nikkei index surged to new record today, signaling robust appetite for risk among Japanese investors, while Yen faces downward pressure, in particular against European majors. Consumer inflation data is in the spotlight in the upcoming Asian session.

Core CPI, which excludes food prices, is forecasted to decelerate from 2.3% to 1.8% in January, below BoJ’s 2% target for the first time in nearly two years. However, for the BoJ, the crucial figure lies in the core-core CPI (excluding both food and energy), which is awaited to see if it will decelerate from December’s 3.7%.

Governor Kazuo Ueda has consistently highlighted the significance of the outcomes from this year’s annual wage negotiations as a pivotal factor in determining the timeline for phasing out the negative interest rate policy.

With large businesses scheduled to conclude wage talks with unions on March 13, just days before BoJ’s next meeting on March 18-19, March is seen by some as a candidate for a rate hike. Yet, April, with the availability of new economic projections, remains a more plausible window for such policy adjustments.

However, any unexpected strength in the inflation report could fuel speculation about an earlier rate hike.

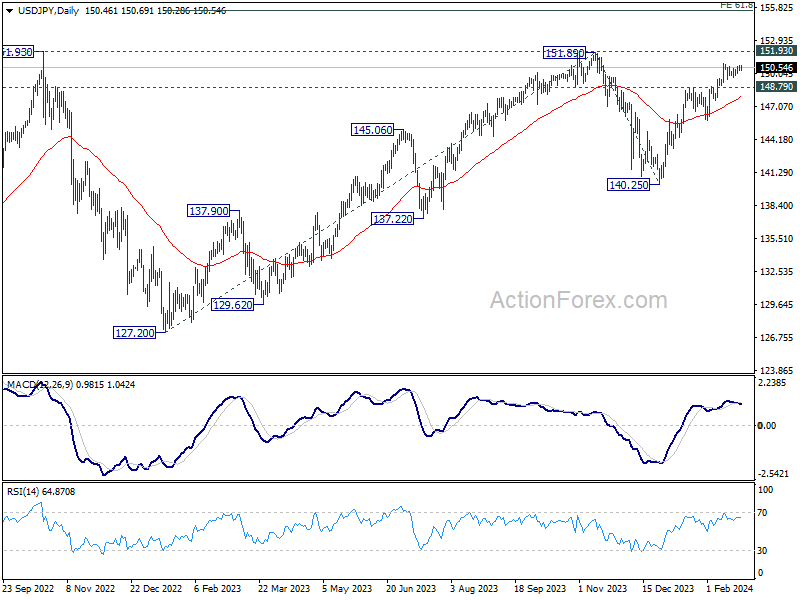

USD/JPY has been losing much momentum after breaking 150 handle. Threat of intervention by Japan could be a major factor keeping USD/JPY bulls from aggressive buying. Nevertheless, rally from 140.25 is still in tact as long as 148.79 support holds. But the path to 151.89/93 resistance zone would be slow.

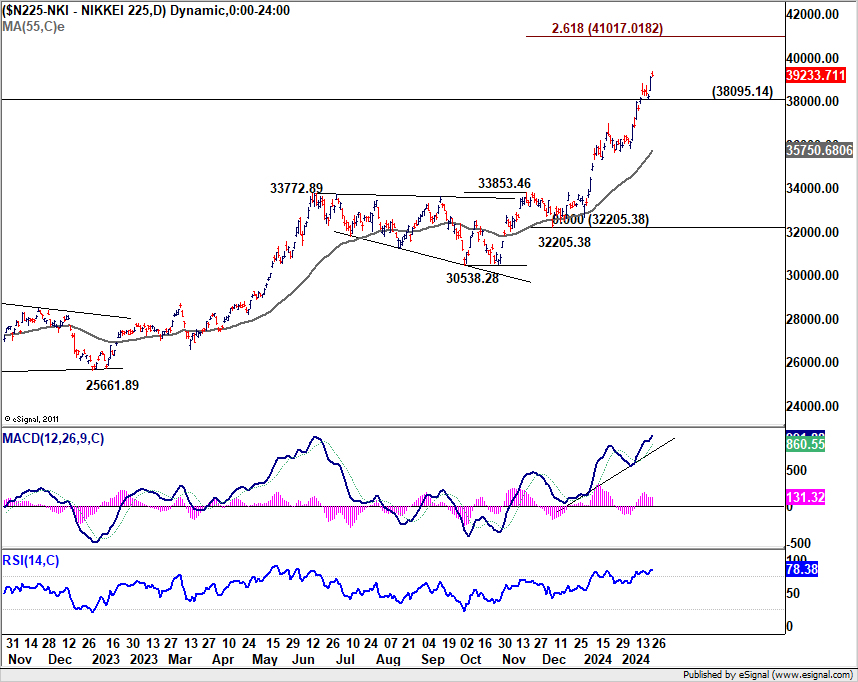

As for Nikkei, it should be rather undeterred by the inflation data. Near term outlook will stay bullish as long as 38095.14 support holds. Next target is 40k psychological level, or even further to 261.8% projection of 30538.28 to 33853.46 from 32205.38 at 41017.01.

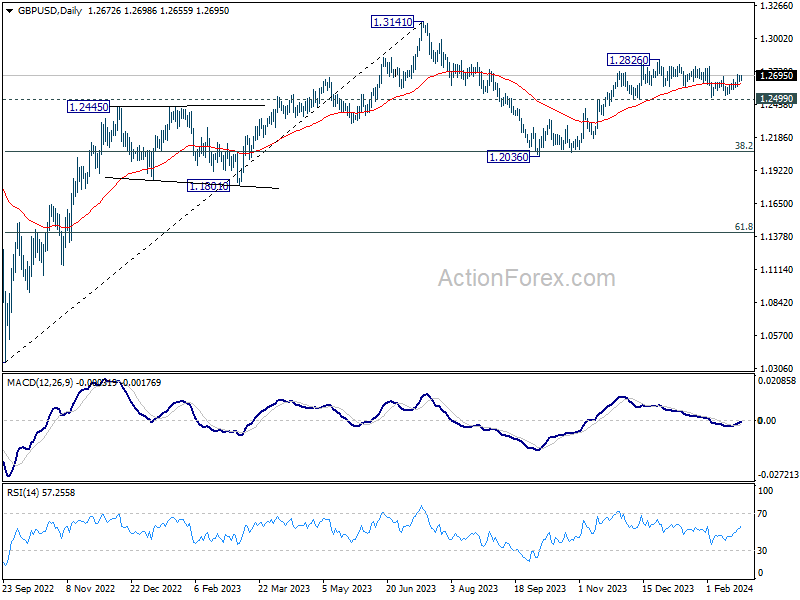

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2647; (P) 1.2674; (R1) 1.2699; More…

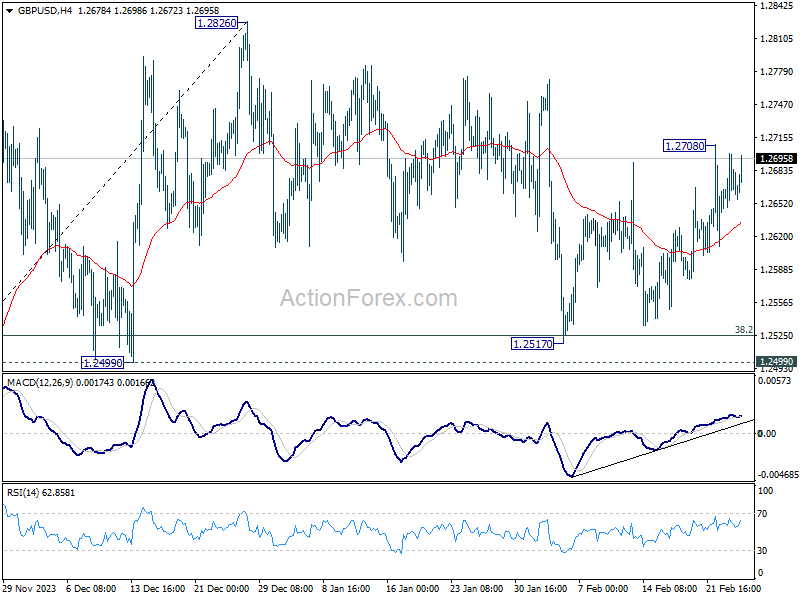

GBP/USD is still capped below 1.2708 temporary top and intraday bias remains neutral first. On the upside, break of 1.2708 resistance will indicate that correction from 1.2826 has completed. Intraday bias will be back on the upside for retesting 1.2826. Nevertheless, decisive break of 1.2499 will argue that whole rise from 1.2036 has completed and turn near term outlook bearish.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which could be still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Jan | 2.10% | 2.40% | 2.40% | |

| 15:00 | USD | New Home Sales M/M Jan | 685K | 664K |

{kind=link}