Yen declines broadly in a classic “sell-on-news” reaction following BoJ’s landmark decision to exit its eight-year negative interest rate policy and announce its first rate hike in 17 years. Although the immediate economic impact of this move is considered minimal, its psychological and symbolic significance cannot be understated. This policy shift was largely anticipated by investors, as evidenced by Nikkei’s stability post-announcement, which saw only brief initial buying before stabilizing.

In parallel, Australian Dollar faces some downward pressure after RBA keeps interest rates on hold as widely expected. The statement left the possibility of further rate hikes open, yet some market participants interpreted the central bank’s language as less hawkish than anticipated. The notion that RBA is “not ruling anything in or out” has led some to speculate that a rate cut could be the next course of action.

As of now, Euro is trading as the day’s strongest currency, followed by Dollar and Swiss Franc. Yen finds itself at the bottom of the performance list, with Australian Dollar and New Zealand Dollar also weak. Sterling and Canadian Dollar occupy the middle ground.

The markets have just begun to unravel the day’s volatility, with significant economic indicators such as German ZEW economic sentiment and Canadian CPI on the agenda. Furthermore, the week promises even more fluctuations with impending meetings from Fed, SNB, and BoE still to come.

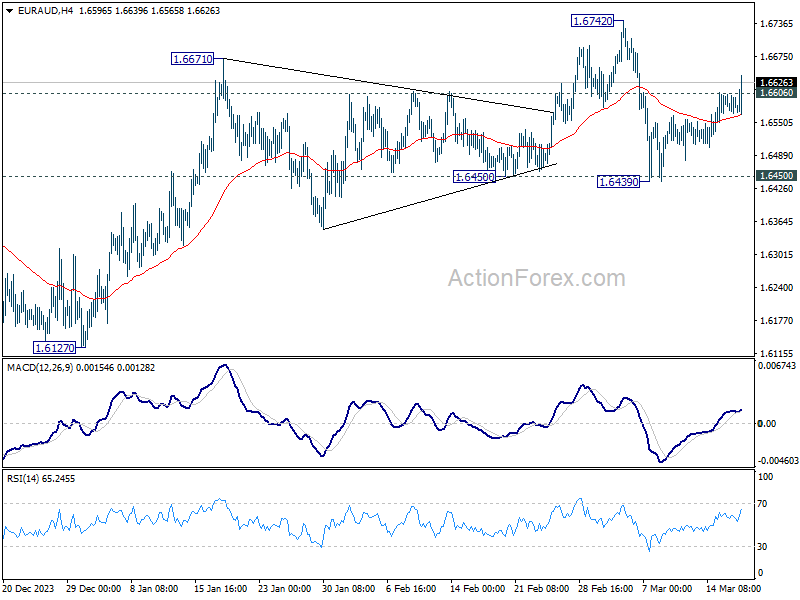

Technically, EUR/AUD’s break of 1.6606 resistance indicates that corrective pullback from 1.6742 has completed at 1.6439, after drawing support from 1.6450. More importantly, rise from 1.1627 low is still in progress. Further rise is now in favor to retest 1.6742 resistance first. Decisive break there will confirm rally resumption.

In Asia, at the time of writing, Nikkei is up 0.03%. Hong Kong HSI is down -1.11%. China Shanghai SSE is down -0.39%. Singapore Strait Times is up 0.04%. Japan 10-year JGB yield is down -0.0323 at 0.731. Overnight, DOW rose 0.20%. S&P 500 rose 0.63%. NASDAQ rose 0.82%. 10-year yield rose 0.036 to 4.340.

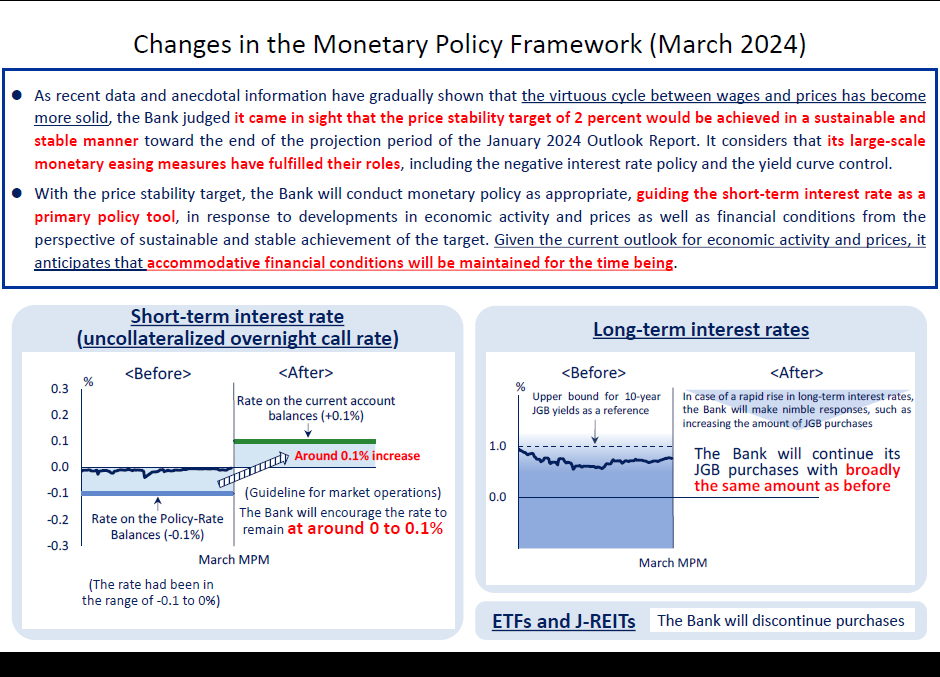

BoJ ends YCC and negative rates as they have fulfilled their roles

In a landmark decision that marks a significant shift in Japan’s monetary policy, BoJ announced the termination of its Yield Curve Control framework and negative interest rate policy, signifying that these measures “have fulfilled their roles.”

This pivotal move is underpinned by BoJ’s assessment that a “virtuous cycle between wages and prices” has come in sight and that the long-standing 2% inflation target is on track to be “achieved in a sustainable and stable manner.”

Setting the overnight call rate to a range of 0-0.1%, the decision was reached with a majority vote of 7-2.

BoJ will continue its purchase of JGBs at “broadly the same amount as before,” ensuring a measure of stability in the bond market. This part of the decision was made with an 8-1 vote. Meanwhile, BoJ has pledged to “respond nimbly” in the event of a rapid rise in long-term interest rates

Additionally, BoJ has outlined plans to discontinue the purchase of ETFs and J-REITs, while the procurement of commercial paper and corporate bonds will be gradually reduced, aiming for discontinuation within approximately one year.

RBA stands pat, not ruling anything in or out

RBA has opted to maintain cash rate target unchanged at 4.35% today, aligning with broad market expectations. The central bank’s stance reflects a cautious approach, emphasizing the prevailing uncertainty in both the global and domestic economic environments. RBA’s declaration that the path of interest rates remains “uncertain” and that it is “not ruling anything in or out” underscores a flexible policy outlook, leaving the door open for rate adjustments in the future, including the possibility of further hikes.

On the inflation front, RBA acknowledges a moderating trend, consistent with its latest forecasts. This moderation is attributed primarily to slowdown in goods inflation. However, services inflation remains stubbornly high, and ism ode rating at a slower pace. Wages growth, a critical factor in the inflation equation, appears to have peaked.

Addressing the economic outlook, RBA paints a picture of significant uncertainty. Internationally, questions loom over China’s economic outlook and the broader impacts of geopolitical conflicts in Ukraine and the Middle East. Domestically, uncertainties pertain to the lag effects of monetary policy adjustments, firms’ pricing decisions, wages dynamics, and household consumption patterns.

Looking ahead

Swiss trade balance and SECO economic forecasts will be released in European session. Germany will publish ZEW economic sentiment. Later in the day, Canada CPI is the main focus while US will release building permits and housing starts.

USD/JPY Daily Outlook

Daily Pivots: (S1) 148.93; (P) 149.13; (R1) 149.35; More…

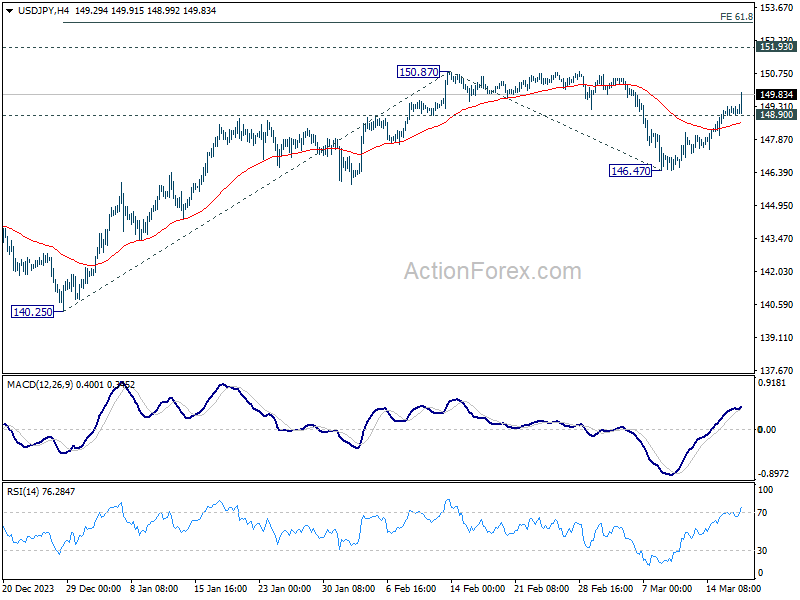

USD/JPY’s rally from 146.47 continues today and intraday bias stays on the upside for retesting 150.87/89 key resistance. Decisive break there will confirm larger up trend resumption. Next near term target will be 61.8% projection of 140.25 to 150.87 from 146.47 at 153.03. On the downside, below 148.90 minor support will delay the bullish case and turn intraday bias neutral first. But outlook will now remain bullish as long as 146.47 support holds.

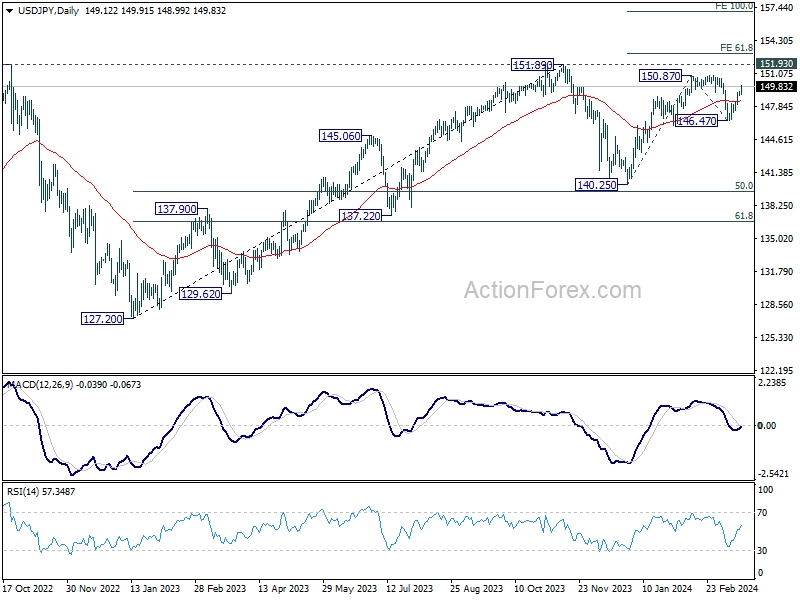

In the bigger picture, correction from 151.87 (2023) high could have completed at 140.25 already. Rise from 127.20 (2023 low), as part of the long term up trend, is probably ready to resume. Decisive break of 151.93 resistance (2022 high) will confirm this bullish case. Also, this will remain the favored case as long as 140.25 support holds, in case of another fall.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 03:30 | AUD | RBA Interest Rate Decision | 4.35% | 4.35% | 4.35% | |

| 03:36 | JPY | BoJ Interest Rate Decision | 0.10% | 0.00% | -0.10% | |

| 04:30 | AUD | RBA Press Conference | ||||

| 04:30 | JPY | Industrial Production M/M Jan F | -6.70% | -7.50% | -7.50% | |

| 07:00 | CHF | Trade Balance (CHF) Feb | 3.50B | 4.74B | ||

| 08:00 | CHF | SECO Economic Forecasts | ||||

| 10:00 | EUR | Germany ZEW Economic Sentiment Mar | 21 | 19.9 | ||

| 10:00 | EUR | Germany ZEW Current Situation Mar | -80 | -81.7 | ||

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Mar | 25.4 | 25 | ||

| 12:30 | CAD | CPI M/M Feb | 0.60% | 0.00% | ||

| 12:30 | CAD | CPI Y/Y Feb | 3.10% | 2.90% | ||

| 12:30 | CAD | CPI Median Y/Y Feb | 3.40% | 3.30% | ||

| 12:30 | CAD | CPI Trimmed Y/Y Feb | 3.50% | 3.40% | ||

| 12:30 | CAD | CPI Common Y/Y Feb | 3.60% | 3.40% | ||

| 12:30 | USD | Building Permits Feb | 1.50M | 1.47M | ||

| 12:30 | USD | Housing Starts Feb | 1.43M | 1.33M |

{kind=link}