In the forex market, clear weakness of Yen, Swiss Franc, and Kiwi contrasts with a broader sense of indecision elsewhere. Dollar’s rally attempt quickly lost momentum as it struggled to break through near-term resistance levels against both the Euro and Sterling. Additionally, the greenback remains stuck within familiar ranges against the Aussie and Loonie, a trend that has persisted since early Q2. Market participants are now eyeing Fed Chair Jerome Powell’s speech at the ECB forum today, though it is unlikely to offer any significant new insights. Traders are more focused on tomorrow’s ISM Services PMI and Friday’s Non-Farm Payroll report before making substantial moves.

At this point in the week, Euro is the best performer, although it lacks follow-through momentum due to political uncertainties in France. Sterling is the second strongest currency, followed by Dollar. On the other hand, Swiss Franc remains the worst performer, followed by Kiwi and Yen. The Aussie and the Loonie are positioned in the middle of the performance spectrum.

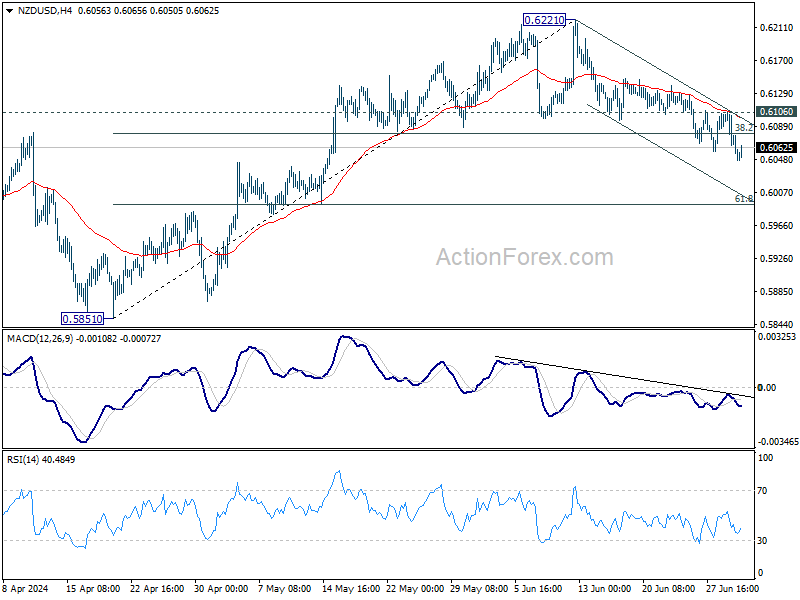

Technically, NZD/USD’s fall from 0.6221 resumed today and further decline is expected as long as 0.6106 resistance holds. Even as a corrective move, current decline would now target 61.8% retracement of 0.5851 to 0.6221 at 0.5992. However, firm break of 0.6106 will argue that the pullback has completed and bring retest of 0.6221 high instead.

In Europe, at the time of writing, FTSE is down -0.44%. DAX is down -1.14%. CAC is down -0.84%. UK 10-year yield is down -0.0409 at 4.246. Germany 10-year yield is down -0.007 at 2.601. Earlier in Asia, Nikkei rose 1.12%. Hong Kong HSI rose 0.29%. China Shanghai SSE rose 0.08%. Singapore Strait Times rose 0.88%. Japan 10-year JGB yield rose 0.0276 to 1.092.

Fed’s Goolsbee suggests rate cuts if inflation declines further

Chicago Fed President Austan Goolsbee has suggested that Fed should consider cutting interest rates if inflation continues its downward trajectory towards the 2% target. He emphasized the importance of adjusting monetary policy to align with changing inflation dynamics.

Goolsbee explained that holding the current rate as inflation decreases effectively tightens monetary conditions. He noted, “If you sit with the rate somewhere while inflation goes down, you’re tightening. The reason that you would want to tighten is if you think that you’re not on a path to 2%.”

Furthermore, Goolsbee pointed out the importance of balancing inflation control with overall economic stability. He noted, “If employment starts falling apart or if the economy begins to weaken, which you’ve seen some warning signs, you’ve got to balance that off with how much progress you’re making on the price front.” While acknowledging that the unemployment rate remains relatively low, he also highlighted its recent upward trend, indicating potential economic softening.

Eurozone CPI slowed to 2.5% in Jun, but core unchanged at 2.9%

Eurozone CPI slowed from 2.6% yoy to 2.5% yoy in June, matched expectations. CPI core (ex-energy, food, alcohol & tobacco) was unchanged at 2.9% yoy, above expectation of 2.8% yoy.

Looking at the main components, services is expected to have the highest annual rate in June (4.1%, stable compared with May), followed by food, alcohol & tobacco (2.5%, compared with 2.6% in May), non-energy industrial goods (0.7%, stable compared with May) and energy (0.2%, compared with 0.3% in May).

ECB’s Lane highlights need for more data on services inflation

ECB Chief Economist Philip Lane emphasized today that June inflation data alone will not suffice to address questions surrounding services inflation, suggesting the ECB may delay further interest rate cuts until additional data is available.

Lane noted, “The key is really services inflation. What we’ve seen in the last days is that services inflation remains the outlier, and what we need to see is whether higher services inflation is a backward element and is a legacy of the rapid disinflation or is it a persistent element. We need time to work on it.”

On the political front, Lane downplayed concerns about France’s recent political turmoil impacting markets significantly, stating, “It is clearly natural in an election for the market to reprice. There are elections all the time, there are movements in spreads all the time. Of course, France is an important country, but this looks like an ordinary repricing to me.”

Other ECB Governing Council members also shared their perspectives at the ECB forum. Lithuania’s Gediminas Simkus aligned with expectations for further rate cuts, stating, “Expectations for two more cuts this year are in line with my own thinking, if data evolve as expected.” Similarly, Belgium’s Pierre Wunsch remarked, “The first two rate cuts are relatively easy as long as inflation hovers around 2.5% because we will still clearly be restrictive.”

RBA minutes: The narrow path is becoming narrower

Minutes of RBA’s June meeting emphasize the need to remain “vigilant to upside risks to inflation”. The RBA noted that the information received since the previous meeting reinforced this need, underscoring the “extent of uncertainty” in the current economic environment, which makes it “difficult either to rule in or rule out” future changes in interest rates.

Concerns were raised about the “narrow path” to bringing inflation back to target within a reasonable timeframe without significantly deviating from full employment. This path, according to the minutes, is “becoming narrower.”

The decision to keep the cash rate target unchanged at 4.35% was deemed the stronger option compared to another rate hike. Data received since May meeting “had not been sufficient” to alter RBA’s assessment that inflation would return to target by 2026, despite “some elevated upside risk” surrounding the forecast. Moreover, the minutes revealed that the members felt there was “not enough evidence” to suggest that the outlook for aggregate demand had strengthened.

NZIER survey shows rising pessimism among New Zealand firms

The NZIER Quarterly Survey of Business Opinion for Q2 reveals increasing pessimism among New Zealand firms. A net 44% of firms are now pessimistic about the economy’s outlook over the next six months, up from 25% in Q1. Additionally, a net 28% reported a deterioration in their own trading during the three months through March, marking the weakest reading since mid-2020 during the COVID-19 pandemic.

Employment figures are equally concerning. A net 25% of firms laid off workers in Q2, the highest level since the global financial crisis in 2009. Furthermore, a net 10% expect to reduce staff numbers in the three months through September. Profit expectations are also bleak, with a net 34% of firms anticipating weaker profits in the third quarter, accompanied by falling investment intentions.

On a slightly more positive note, only a net 23% of firms expect to increase prices in Q3, the lowest since 2021. Additionally, companies are finding it easier to recruit workers, signaling reduced wage pressure. Fewer companies also reported rising costs, suggesting some relief from inflationary pressures.

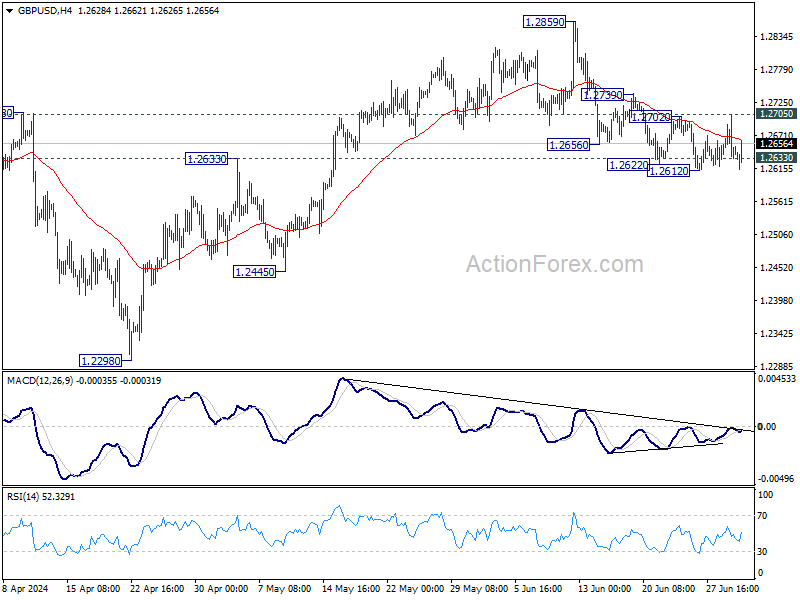

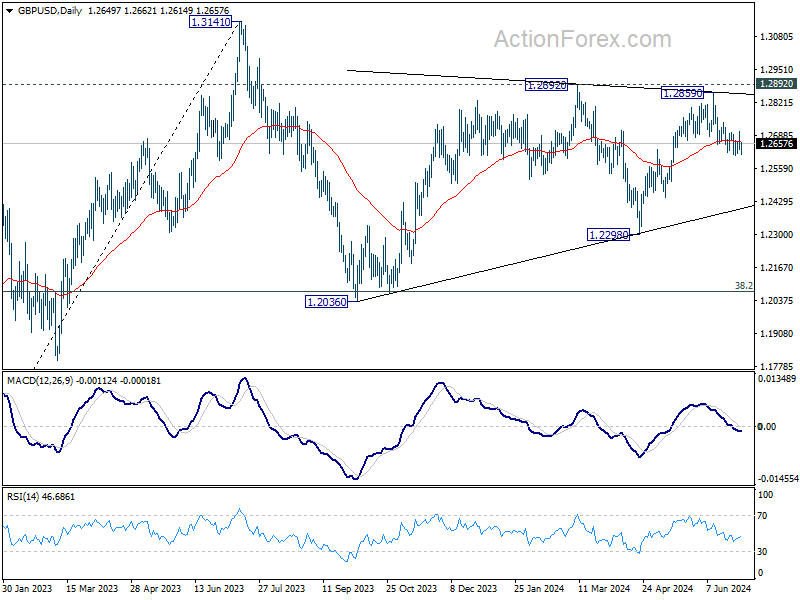

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2622; (P) 1.2661; (R1) 1.2690; More…

GBP/USD recovered ahead of 1.2612 support as range trading continues. Intraday bias remains neutral at this point. On the upside, firm break of 1.2705 resistance will argue that pull back from 1.2859 has completed, and bring retest of this high instead. Nevertheless, sustained trading below 1.2633 resistance turned support will argue that whole rise from 1.2298 has completed, and target 1.2445 and below.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern that is still in progress. Break of 1.2445 support will confirm that another falling leg has started and target 1.2036 cluster support again (38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075. Nevertheless, break of 1.2892 resistance will argue that larger up trend from 1.0351is ready to resume through 1.3141.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M May | -1.70% | -1.90% | -2.10% | |

| 01:30 | AUD | RBA Meeting Minutes | ||||

| 09:00 | EUR | Eurozone Unemployment Rate May | 6.40% | 6.40% | 6.40% | |

| 09:00 | EUR | Eurozone CPI Y/Y Jun P | 2.50% | 2.50% | 2.60% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Jun P | 2.90% | 2.80% | 2.90% | |

| 13:30 | CAD | Manufacturing PMI Jun | 50.2 | 49.3 |

{kind=link}