Yen continues its extended selloff today, except against New Zealand Dollar, in an otherwise subdued forex market. Reports indicate that BoJ may lower its economic growth forecasts for this year at its meeting later in July, while predicting that inflation will hover around 2% target in the coming years. These updated forecasts could keep the BoJ on track for another rate hike, potentially as soon as this meeting.

Additionally, BoJ’s plan to taper its bond purchases is drawing attention. This week, the central bank is meeting with institutional investors to discuss its strategy. One of the megabanks has suggested significantly reducing monthly bond purchases to JPY 1T. However, opinions vary, with life insurance firms and asset managers offering diverging views—some advocating for gradual reductions, while others call for an immediate halt to purchases.

Despite these discussions, Yen is receiving little support and is likely to remain weak until BoJ’s next meeting on July 30-31. Traders seem to be waiting for concrete actions rather than relying on speculative reports.

In the broader currency markets, New Zealand Dollar is the worst performer of the week so far, following today’s sharp decline after RBNZ hinted at future monetary easing. This dovish shift has led markets to anticipate the first rate cut could occur in November, earlier than previously expected. Yen is the second weakest currency, followed by Swiss Franc.

On the flip side, Canadian Dollar is currently the strongest performer. Dollar is the second strongest but is on edge ahead of tomorrow’s crucial US CPI release, which could significantly influence market movements. British Pound ranks third in performance, while Euro and Australian Dollar are trading in middle positions.

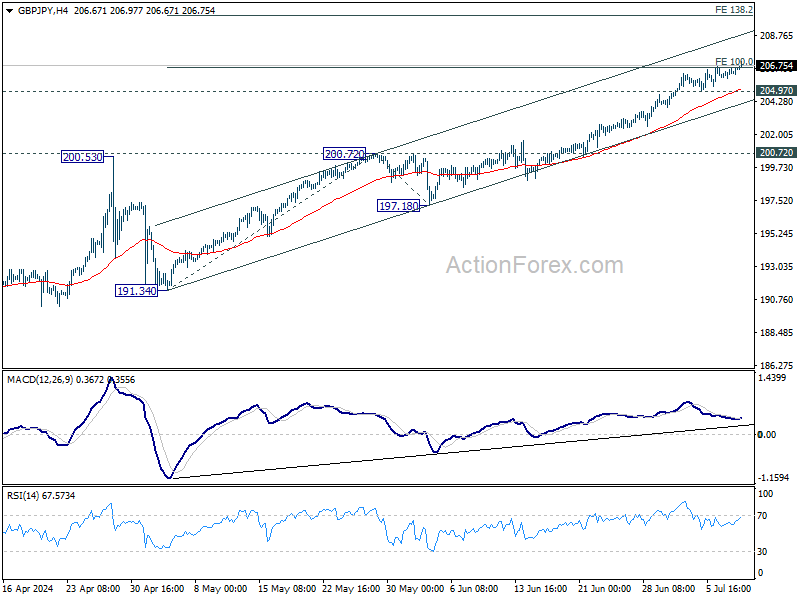

Technically, GBP/JPY’s recent up trend is trying to resume today and momentum appears to be picking up slightly, as seen in 4H MACD. Near term outlook will stay bullish as long as 204.94 support holds. sustained break of 100% projection of 191.34 to 200.72 from 197.18 at 206.56 will target 138.2% projection at 210.17. The cross will be closely watching tomorrow’s UK GDP release for further direction.

In Europe, at the time of writing, FTSE is up 0.61%. DAX is up 0.63%. CAC is up 0.64%. UK 10-year yield is down -0.0505 at 4.112. Germany 10-year yield is down -0.0586 at 2.528. Earlier in Asia, Nikkei rose 0.61%. Hong Kong HSI fell -0.29%. China Shanghai SSE fell -0.68%. Singapore Strait Times rose 0.99%. Japan 10-year JGB yield rose 0.0129 to 1.089.

In Europe, at the time of writing, FTSE is up 0.61%. DAX is up 0.63%. CAC is up 0.64%. UK 10-year yield is down -0.0505 at 4.112. Germany 10-year yield is down -0.0586 at 2.528. Earlier in Asia, Nikkei rose 0.61%. Hong Kong HSI fell -0.29%. China Shanghai SSE fell -0.68%. Singapore Strait Times rose 0.99%. Japan 10-year JGB yield rose 0.0129 to 1.089.

RBNZ holds rates at 5.50%, softens hawkish tone

RBNZ left OCR unchanged at 5.50%, as widely expected. The central bank softened its hawkish stance in the accompanying statement, indicating that the extent of monetary restriction “will be tempered over time consistent with the expected decline in inflation pressures.” Markets interpreted this as a signal that RBNZ is moving closer to lowering interest rates.

RBNZ also acknowledged that its restrictive monetary policy has “significantly reduced consumer price inflation,” with headline inflation expected to return to the 1-3% target band “in the second half of this year.” This decline in inflation reflects both receding domestic pricing pressures and lower inflation for imported goods and services. Additionally, labor market pressures have eased.

While domestically generated price pressures “remain strong,” RBNZ said there are signs that “inflation persistence will ease in line with the fall in capacity pressures and business pricing intentions.”

China’s CPI slows to 0.2% in Jun, PPI negative for 21st month

China’s CPI slowed to 0.2% yoy in June, down from 0.3% yoy in May, missing expectations of a 0.4% yoy increase. Core CPI, which excludes volatile food and energy prices, rose by 0.6% yoy, unchanged from May, but slightly slower than the 0.7% increase observed in the first half of the year.

On a month-on-month basis, inflation remained negative in June, with CPI falling by -0.2%, following a -0.1% decrease in May. This continued negative trend reflects ongoing deflationary pressures in the economy.

PPI fell by -0.8% yoy, improving from the prior month’s -1.4% yoy decline and matching market expectations. Despite the slight improvement, PPI has remained negative for the 21st consecutive month, indicating persistent weakness in industrial prices.

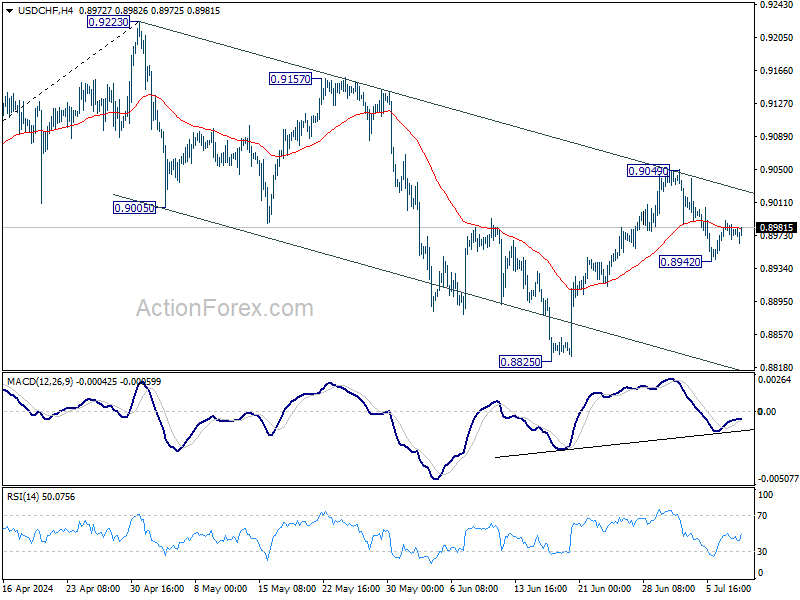

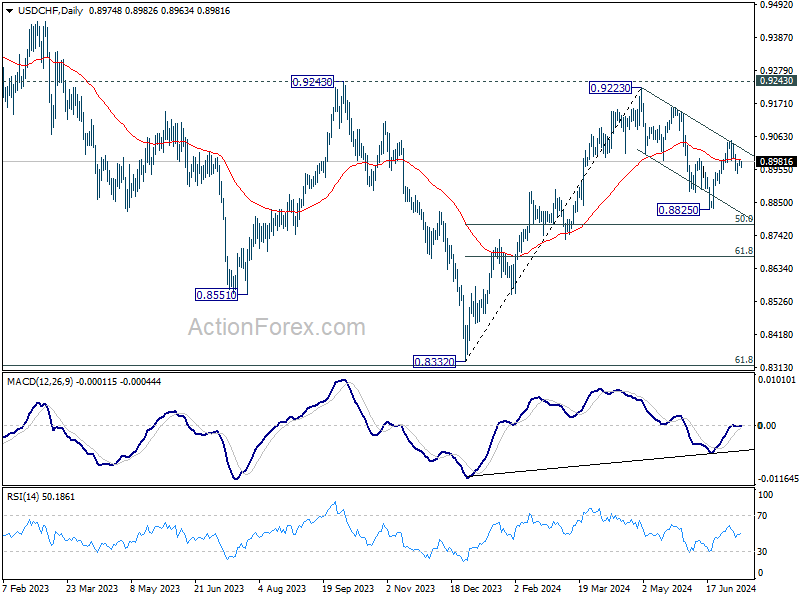

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8965; (P) 0.8978; (R1) 0.8991; More…

USD/CHF is staying in range of 0.8942/9049 and intraday bias remains neutral. As noted before, rebound from 0.8825 could have completed at 0.9049, after rejection by falling channel resistance. Below 0.8942 will bring deeper fall to 0.8825 support. Nevertheless, break of 0.9049 will revive near term bullishness and resume the rebound from 0.8825 instead.

In the bigger picture, focus remains on 0.9223/9243 resistance zone. Decisive break there would suggest larger bullish trend reversal and turn outlook bullish. Nevertheless, rejection by 0.9223/43 will keep medium term outlook neutral at best, for more range trading between 0.8332/9243 first.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | PPI Y/Y Jun | 2.90% | 2.90% | 2.40% | 2.60% |

| 01:30 | CNY | CPI Y/Y Jun | 0.20% | 0.40% | 0.30% | |

| 01:30 | CNY | PPI Y/Y Jun | -0.80% | -0.80% | -1.40% | |

| 02:00 | NZD | RBNZ Interest Rate Decision | 5.50% | 5.50% | 5.50% | |

| 08:00 | EUR | Italy Industrial Output M/M May | 0.50% | 0.20% | -1.00% | |

| 14:00 | USD | Wholesale Inventories May F | 0.60% | 0.60% | ||

| 14:30 | USD | Crude Oil Inventories | 0.7M | -12.2M | ||

| 18:00 | USD | Fed’s Beige Book |

{kind=link}