Sterling weakened sharply overnight as risk appetite deteriorated on growing fears of military escalation in the Middle East. US President Donald Trump raised the stakes with Iran, issuing a public ultimatum to Supreme Leader Khamenei for “unconditional surrender” after claiming “total control” over Iranian airspace. There are intensified concerns that the US could intervene directly.

The recent US–UK trade deal, while politically symbolic, has failed to offer material support to the Pound. Despite exemptions on aerospace and automobile tariffs, the unresolved dispute over steel and aluminum and the conditional structure of the agreement left investors unimpressed. Indeed, Sterling’s weak showing contrasts with resilience seen in Kiwi and Aussie, which benefits from relative insulation from the geopolitical flashpoints.

Yet Sterling found support as European trading got underway, thanks to a firmer-than-expected inflation report. Notably, goods inflation surged to a seven-month high of 2.0%, suggesting that the impact of global tariffs may be starting to show up in consumer prices. Markets still expect BoE to deliver a rate cut in August, but the MPC’s decision on Thursday will be closely watched for signs of shifting sentiment with the Committee

In the broader picture, today’s FOMC meeting may have little short-term impact unless the dot plot shifts decisively. With no surprises expected, traders may look elsewhere for direction. That “elsewhere” may once again be geopolitical developments and trade tensions. Trump continues to ramp up his rhetoric, the EU that they will either make a “fair deal” or pay “whatever we say.” A deadline of July 9 looms for reciprocal tariffs to resume, and negotiations remain mixed at best.

For the week so far, Kiwi and Aussie are currently the stronger ones. Dollar is also on the firmer side. Sterling is at the bottom, followed by Yen, and then Swiss Franc. Euro and Loonie are positioning in the middle.

In Asia, at the time of writing, Nikkei is up 0.77%. Hong Kong HSI is down -1.30%. China Shanghai SSE is up 0.04%. Singapore Strait Times is down -0.44%. Japan 10-year JGB yield is down -0.06 at 1.466. Overnight, DOW fell -0.7%. S&P 500 fell -0.84%. NASDAQ fell -0.91%. 10-year yield fell -0.059 to 4.393.

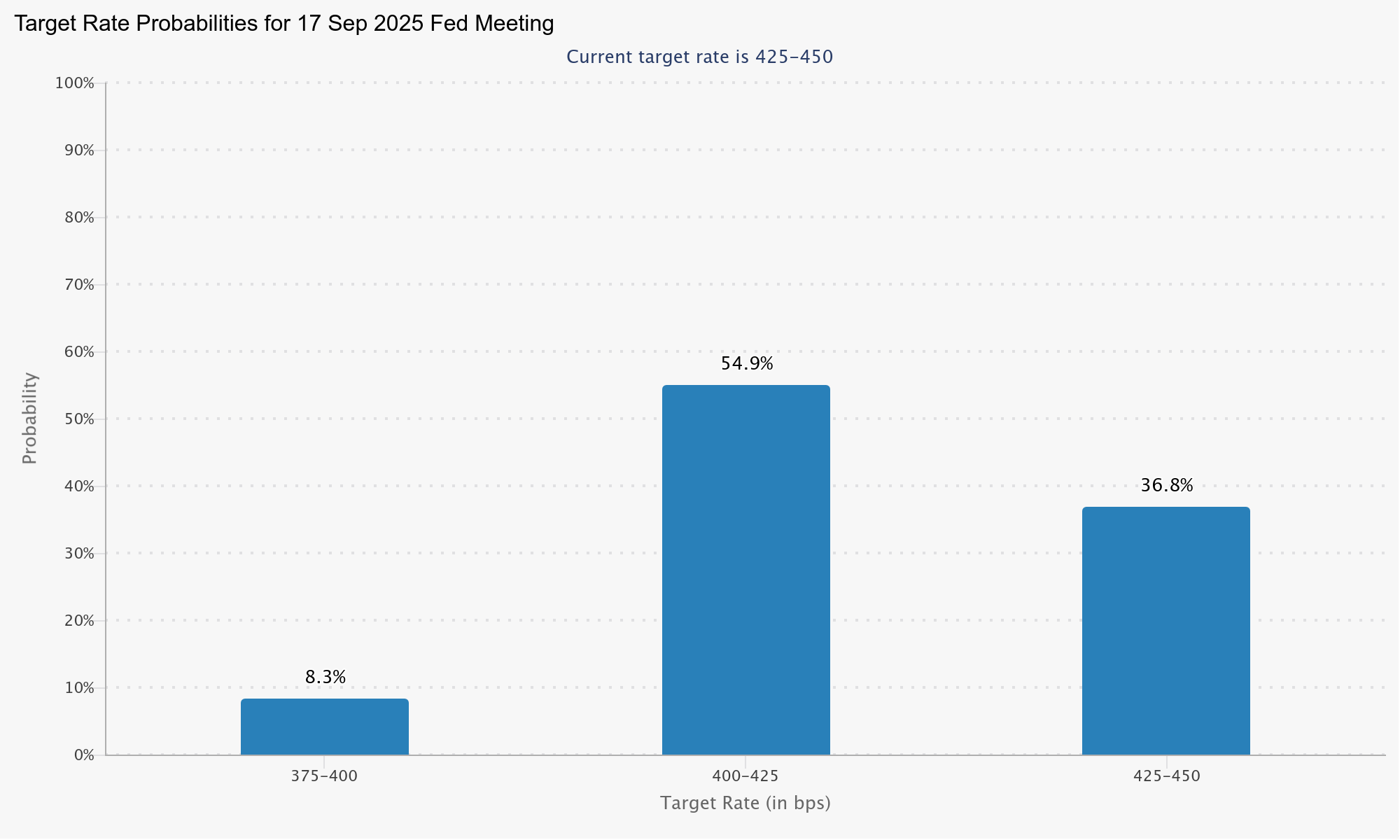

Fed to hold at 4.25–4.50%, eyes on (any) dot plot shift

Fed is all but certain to keep its target rate unchanged at 4.25–4.50% today, with fed fund futures assigning a near-unanimous 99.9% probability to that outcome. Similarly, the likelihood of any move in July is negligible, with markets pricing in an 85% chance that rates will remain on hold. Instead, the focus is on the September meeting, where futures suggest a roughly 63% chance of Fed resume its easing cycle.

The biggest variable in today’s announcement will be the updated Summary of Economic Projections, especially the dot plot. In March, the median forecast signaled two rate cuts in 2025. However, that view was narrowly held, and it would take just two FOMC members adjusting their dots to shift the median forecast to one cut.

However, the inflation and growth projections themselves may offer limited clarity due to the lingering uncertainty over trade policy. The 90-day reciprocal tariff truce expires in early July, and with no clear signal from Washington, Fed is unlikely to factor tariff impacts heavily into its base case just yet.

Chair Jerome Powell is expected to reiterate his recent message that “policy is in a good place” and that there is no rush to cut. Investors will watch closely for any tone shift in his comments on labor market softening and disinflation trends, but the overall message will likely reinforce Fed’s preference for patience. With no new direction expected, market reactions are likely to be limited in the immediate aftermath of the meeting.

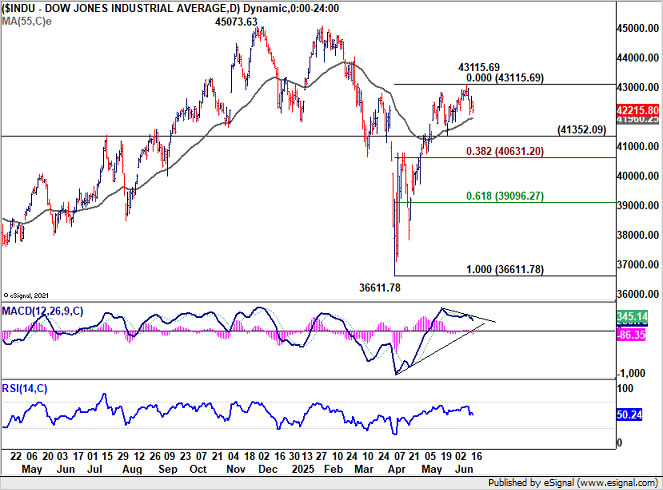

Technically, DOW’s rally attempt this week lacks conviction. Bearish divergence condition in D MACD suggests that a short term top could have already formed at 43115.69. Deeper pull back is likely in the near term. Firm break of 41352.09 support will bring deeper fall to 38.2% retracement of 36611.78 to 43115.69 at 40631.20 at least, even still as a corrective move to the rally from 36611.78, not to mention that there is risk of near term bearish reversal.

UK CPI slows to 3.3% in May, but goods prices surges to highest since late 2023

UK headline CPI eased from 3.5% yoy to yoy in May, slightly above expectations of 3.3% yoy. Core CPI (excluding energy, food, alcohol and tobacco) also slowed from 3.8% to 3.5%, in line with forecasts.

While the overall trend points to gradual disinflation, markets might pay more attention to the reacceleration in goods prices, which rose to 2.0% yoy, the highest rate since November 2023.

Services inflation, however, showed a more meaningful decline, falling from 5.4% yoy to 4.7% yoy, suggesting underlying pressures are softening.

On a monthly basis, CPI rose by 0.2% mom, matching expectations.

Japan’s exports slide – 1.7% yoy in May as auto tariffs from US take toll

Japan’s trade data for May revealed growing pressure on its export sector, with headline exports falling -1.7% yoy to JPY 8.135T. Imports dropped -7.7% yoy to JPY 8.773T. The resulting trade deficit stood at JPY -637.6B.

Of particular concern was the sharp -11.1% fall in exports to the US, where car shipments plunged -24.7% yoy on the immediate impact of US tariffs.

Despite posting a trade surplus of JPY 451.7B with the US, the bilateral trend was negative. Imports from the US dropped -13.5% yoy. Japanese exporters are now grappling with a 25% tariff on autos and auto parts, plus a 10% baseline levy on all other goods. Steel and aluminum products have also been hit with a 50% tariff in early June.

On a seasonally adjusted basis, exports edged up just 0.1% mom, while imports declined -0.3% mom, leaving a narrower but still negative trade balance of JPY -305B.

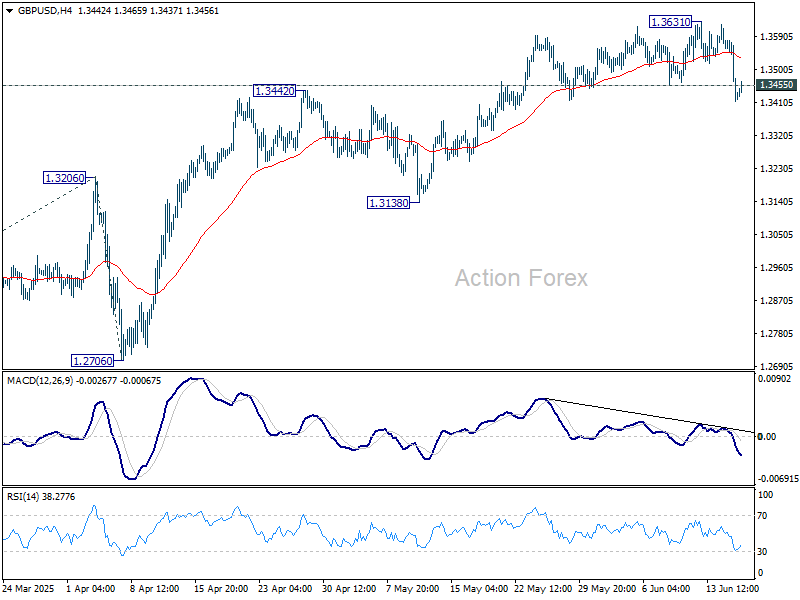

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3364; (P) 1.3480; (R1) 1.3545; More…

GBP/USD’s steep decline confirms short term topping at 1.3631, on bearish divergence condition in 4H MACD. Intraday bias is back on the downside for correction to 55 D EMA (now at 1.3328). Strong support could be seen there to bring rebound. Brea of 1.3631 will resume the rally from 1.2099 and target 100% projection of 1.2099 to 1.3206 from 1.3138 at 1.3813. However, sustained break of 55 D EMA will indicate that deeper correction is underway.

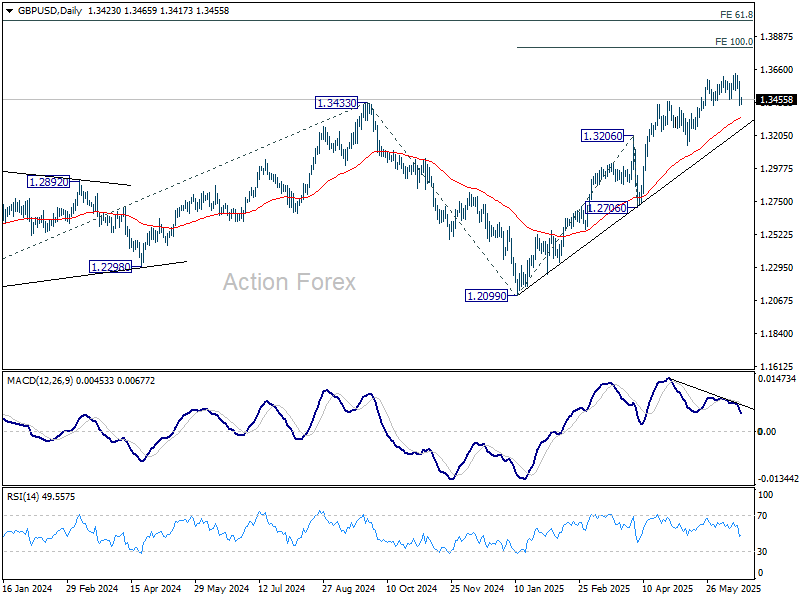

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2937) holds, even in case of deep pullback.

{kind=link}