Global markets continue to trade with cautious optimism, despite signs of strain in the fragile Israel-Iran ceasefire. Reports out of Tehran on renewed Israeli airstrikes—despite US President Donald Trump declaring a ceasefire hours earlier—have added tension. Israeli army radio said the strikes targeted an Iranian radar site near Tehran, while explosions were confirmed by Iranian media.

Still, there is no sign of panic in markets. WTI oil remains subdued near day low, hovering around 77, suggesting traders aren’t yet pricing in a full re-escalation. European indexes and US futures are in the green, reflecting relief that the broader conflict hasn’t spilled into a full-blown regional war. The Strait of Hormuz remains open, and risk appetite is finding a footing.

Dollar is the worst-performing major today, extending its post-Bowman slump as dovish Fed commentary mounts. Chair Jerome Powell warned in his Congressional testimony that allowing tariff-driven price spikes to evolve into entrenched inflation would be a policy failure. His insistence on anchoring expectations signals resistance to immediate rate cuts—even as July odds creep higher.

Atlanta Fed President Raphael Bostic echoed that sentiment, telling Reuters he prefers to wait until the fourth quarter to consider cutting rates. He noted that firms are gradually adjusting to tariffs through phased price increases, not sharp demand destruction. That slower pass-through gives the Fed more time to assess data and reinforces Powell’s “wait and see” stance.

In the forex markets, Kiwi leads gains today, followed by Yen and Aussie. Loonie lags alongside Dollar and Euro. Sterling and franc are middling performers, with CHF strength worth monitoring for potential geopolitical flows.

One pair to watch is USD/CHF, which resumed its selloff in early US trading. It’s unclear whether the move is entirely Dollar-driven or partially fueled by renewed geopolitical hedging. A break of the 0.8038/0.8054 zone would confirm continuation of the larger downtrend and may reflect a shift in risk sentiment if ceasefire doubts escalate further.

In Europe, at the time of writing, FTSE is up 0.36%. DAX is up 1.85%. CAC is up 1.30%. UK 10-year yield is up 0.003 at 4.499. Germany 10-year yield is up 0.038 at 2.548. Earlier in Asia, Nikkei rose 1.14%. Hong Kong HSI rose 2.06%. China Shanghai SSE rose 1.15%. Singapore Strait Times rose 0.65%. Japan 10-year JGB yield rose 0.009 to 1.420.

Fed’s Powell: Without price stability, strong labor markets can’t last

In his prepared remarks for Congressional testimony, Fed Chair Jerome Powell acknowledged that this year’s tariff increases are likely to both “push up prices and weigh on economic activity”. He noted that while the inflationary effects could be transitory, there’s also a risk that they become more persistent depending on the magnitude of pass-through and how firmly inflation expectations remain anchored.

Powell emphasized that Fed’s primary responsibility is to “keep longer-term inflation expectations well anchored and to prevent a one-time increase in the price level from becoming an ongoing inflation problem”.

He emphasized that “without price stability, we cannot achieve long periods of strong labor market conditions”.

Given the uncertainties ahead, Powell signaled that the FOMC remains in a wait-and-see mode, saying the Fed is “well positioned to wait” before making any policy changes.

Fed’s Bostic pushes back on July cut, sees Q4 as earliest window

Atlanta Fed President Raphael Bostic pushed back against market hopes for a near-term rate cut in July, saying he remains cautious about inflation and sees little urgency to ease policy.

In an interview with Reuters, Bostic said he would prefer to hold rates in a restrictive zone “for longer just to be absolutely sure” inflation returns sustainably to the 2% target. While others have floated the possibility of a cut in July, Bostic said “I would see the last quarter is sort of when I would expect we would know enough to move.”

Bostic acknowledged that tariff-related risks have not yet materialized into a “doomsday scenario”, thanks to business adaptability. He said executives have grown more confident in managing price pressures, and are already preparing to raise prices in phases as a response to higher input costs.

That business strategy, he argued, is one of the key reasons he remains wary of easing too early, fearing that inflation momentum could persist. “They tell me ‘I’m pretty sure I am going to have to raise my prices. The question is not whether but when,'” he emphasized.

Canada’s CPI steady at 1.7% in May, but underlying pressures linger

Canada’s headline CPI was unchanged at 1.7% yoy in May, matching expectations. Excluding energy, inflation eased from 2.9% yoy to 2.7% yoy. On a monthly basis, however, CPI rose 0.6% mom, slightly above expectations of 0.5% mom.

Core measures offered a mixed signal. CPI median and trimmed both softened from 3.1% yoy to 3.0% yoy, aligning with forecasts, However, CPI common, a key metric for the BoC, accelerated unexpectedly to 2.6% yoy from 2.5% yoy.

BoE’s Greene see sticky inflation plateau, not hump

BoE policymaker Megan Greene said inflation may hover around 3.5% for the rest of 2025, warning that the disinflation path now looks more like a “plateau” than a “hump.”

Speaking in a speech, Greene cautioned that this could entrench elevated inflation expectations and influence wage and price-setting behaviors—particularly as food and energy prices, both highly salient for consumers, continue to surprise to the upside.

Greene said the risks are “skewed to the upside” on inflation and “to the downside” on growth—arguing for a cautious policy stance.

She also pointed to persistent domestic data noise and multiple unresolved global uncertainties, including US budget negotiations, “reciprocal tariffs” deadlines, and geopolitical tensions, as reasons to avoid rushing rate cuts.

“It’s unlikely that the uncertainty from these events – and subsequent developments – will be resolved any time soon. I therefore think a careful and gradual approach to removing monetary policy restrictiveness continues to be warranted,” she emphasized.

Villeroy says ECB may ease further if Euro strength holds, plays down tariff risks

French ECB Governing Council member François Villeroy de Galhau suggested that more monetary easing could be warranted later this year if the recent rise in the euro continues to buffer the inflationary impact of higher oil prices.

In an interview with the Financial Times, Villeroy said “inflation expectations remain moderate,” and the currency’s appreciation would help neutralize energy-driven price pressures. “If that was confirmed, it could possibly lead in the next six months to a further accommodation,” he added.

Policymakers will be cautious in reacting to short-term oil moves unless they translate into broader inflation risks. “If we were to see spillovers to underlying inflation and de-anchoring of inflation expectations, then we could possibly adapt monetary policy,” he added.

On the trade front, Villeroy dismissed fears that escalating US-EU tensions would create meaningful inflation in the bloc. He argued that the primary risk is to growth, not prices, given that EU tariffs would apply narrowly to US goods, unlike Washington’s broader measures. The stronger Euro also acts as a buffer, muting any imported inflation effects.

Germany’s Ifo business climate rises to 88.5, services and construction lead sentiment rebound

Germany’s Ifo Business Climate index rose from 87.5 to 88.4 in June, modestly above expectations. Expectations Index jumped to 90.7 from 88.9, while Current Assessment Index edged up only slightly from 86.1 to 86.2. Ifo said the economy is “slowly building confidence”.

Sector details showed the clearest momentum in services, where firms raised expectations significantly, especially among business-related providers. Manufacturing also saw better sentiment ahead, though order books remain under pressure. Construction extended its recovery trend, with expectations hitting the highest level since early 2022. Wholesale trade led the modest rebound in commerce, but retail conditions slipped again.

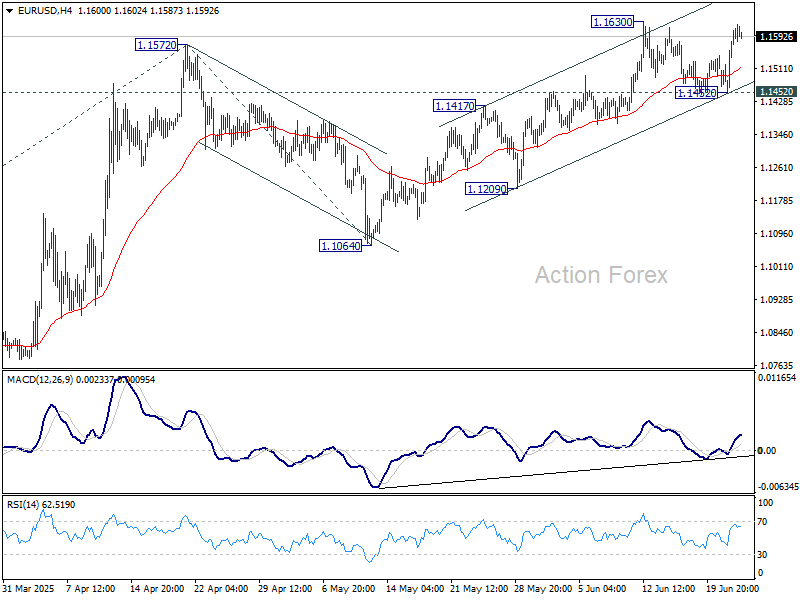

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1495; (P) 1.1538; (R1) 1.1623; More…

Intraday bias in EUR/USD remains neutral at this point. With 1.1452 support intact, further rise is expected. Break of 1.1630 resistance will extend the rise from 1.0176. Next target is 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927. However, break of 1.1452 support will indicate short term topping, and turn bias to the downside for deeper pullback.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 1.1604 support holds.

{kind=link}