{kind=link}

Market conditions have settled after earlier risk-on moves, with European indexes and US futures showing little direction. The absence of follow-through buying suggests traders are shifting toward more cautious trading. With desks fully staffed again, attention is turning to Friday’s December US non-farm payrolls report. Dollar remains broadly on the back foot and will be looking to the labor data for support after this week’s underperformance.

The base case still points to Fed delivering one more rate cut later this year, in line with the latest dot plot guidance. However, any renewed tightness in the labor market could push the timing of that move deeper into the second half of 2026. Even so, there remains a substantial flow of inflation and employment data before the March FOMC meeting. As a result, markets could remain wary of taking large directional bets based on a single payroll print.

The immediate attention, though, is shifting to Australia’s November CPI data first, which will be released in the upcoming Asian session. Consensus hopes for a moderation in inflation from October’s 3.8% pace, though forecasts span a wide range, leaving scope for upside surprise.

Australia’s interest-rate outlook has undergone a sharp reassessment since late 2025. Expectations have swung from further easing — after three cuts last year — to discussions around an extended pause and even the possibility of renewed tightening this year. That pivot was reinforced by RBA Governor Michele Bullock, who said she does not see rate cuts “on the horizon for the foreseeable future,” adding that the board is weighing an extended hold against the risk of a rate rise.

Markets currently see February as a low-probability hiking window for the RBA, but pricing jumps sharply by mid-year, with a quarter-point increase fully priced by August. Tomorrow’s data could reshape these expectations.

For the week so far, Sterling leads FX performance, followed by Aussie and Kiwi. Loonie lags at the bottom, with Euro and Swiss Franc also under pressure. Dollar and Yen sit mid-pack.

In Europe, at the time of writing, FTSE is up 1.08%. DAX is up 0.29%. CAC is down -0.03%. Germany 10-year yield is down -0.021 at 4.486. UK 10-year yield is down -0.029 at 2.845. Earlier in Asia, Nikkei rose 1.32%. Hong Kong HSI rose 1.38%. China Shanghai SSE rose 1.50%. Singapore Strait Times rose 1.27%. Japan 10-year JGB yield rose 0.011 to 2.130.

Fed’s Barkin says policy near neutral, dual mandate tensions persist

Richmond Fed President Tom Barkin said today the outlook for US monetary policy is in a “delicate balance,” as policymakers weigh still-elevated inflation against signs of rising unemployment. Speaking on the policy outlook, Barkin stressed that conflicting pressures mean “both sides of the Fed’s dual mandate bear watching.”

Barkin noted that last year’s 75 basis points of easing have brought interest rates “within range of neutral,” likening the move to taking out insurance against downside risks. Inflation has cooled but remains above target, while unemployment is still low by historical standards. However, he cautioned that policymakers do not want labor market conditions to deteriorate much further.

Despite near-term uncertainty, Barkin said he is optimistic on the 2026 outlook. He expects last year’s elevated uncertainty to ease, boosting confidence among consumers and businesses. Fiscal changes, deregulation efforts, and the delayed impact of monetary easing are all expected to provide meaningful support to economic growth.

UK PMI services finalized at 51.4, tepid expansion, inflation risks linger

UK service sector activity showed only marginal improvement at the end of 2025, with Services PMI finalized at 51.4 in December, up fractionally from 51.3 in November. Composite PMI also edged higher to 51.4 from 51.2, pointing to continued but lackluster expansion across the broader economy.

According to S&P Global Market Intelligence, Economics Director Tim Moore said business activity growth remained subdued and weaker than indicated by the earlier flash estimate. Survey respondents cited persistent sales headwinds tied to soft UK growth prospects, rising business costs, and weak overseas demand, contributing to another notable decline in service sector employment.

Despite muted demand, inflation pressures intensified. Input prices rose at the fastest pace in seven months, while output charge inflation rebounded from November’s low.

Eurozone PMI services slows but remains key pillar for 2026 outlook

Eurozone economic momentum cooled modestly at the end of 2025, with Services PMI finalized at 52.4 in December, down from 53.6 in November. Composite PMI also eased to 51.5 from 52.8.

Performance across countries remained uneven. Spain led the bloc with a composite reading of 55.6, a two-month high. Ireland slipped to 53.6. Germany eased to 51.3, its lowest in four months, Italy fell to 50.3, an eleven-month low, and France hovered at the stagnation threshold at 50.0.

Despite the slowdown, Hamburg Commercial Bank Chief Economist Cyrus de la Rubia said the services sector has now expanded for seven consecutive months and that “the picture looks good” overall. He added that Composite PMI averaged a “visibly higher level” in the final quarter, suggesting GDP growth likely accelerated toward year-end, driven primarily by services. Growth prospects for 2026 improve modestly, with overall expansion seen above 1% but far from robust.

At the same time, rising cost pressures in services remain a key constraint on policy. ECB President Christine Lagarde has stressed close monitoring of services inflation, where higher wages continue to push costs and prices up. That dynamic explains why the ECB has paused further rate cuts.

Japan monetary base drops below JPY 600T, as BoJ presses ahead with normalization

Japan’s monetary base contracted in 2025 for the first time since 2007, underlining the Bank of Japan’s decisive shift away from decades of ultra-loose policy. Data released today showed the average balance of the monetary base fell -4.9% year-on-year, echoing the period when the BoJ last embarked on a rate-hike cycle.

The contraction accelerated toward year-end. The average balance in December stood at JPY 594.19 trillion, down -9.8% yoy and falling below the JPY 600 trillion mark for the first time since September 2020.

The decline reflects the BoJ’s ongoing exit from its decade-long stimulus, which began in 2024. Since then, the central bank has raised interest rates, slowed purchases of JGBs and wound down funding schemes designed to encourage bank lending. With policy normalization still underway, Japan’s monetary base is expected to continue shrinking as bond tapering and further rate hikes proceed.

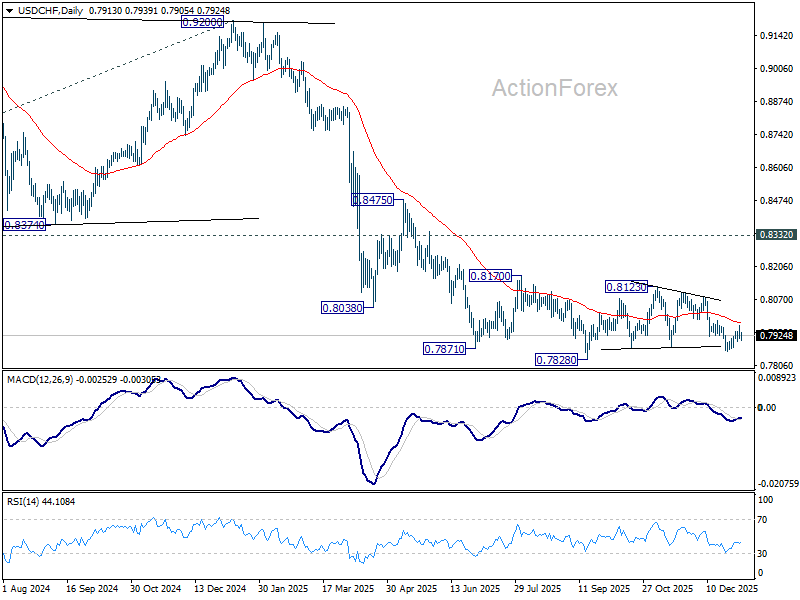

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7897; (P) 0.7932; (R1) 0.7952; More….

Intraday bias in USD/CHF stays neutral for the moment. Further decline is mildly in favor with 0.7986 resistance intact. On the downside, below 0.7900 minor support will turn bias to the downside. Break of 0.7860 will target a retest on 0.7828 low. However, break of 0.7986 will argue that corrective pattern from 0.7828 is still extending with another rising leg already in progress.

In the bigger picture, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low). Long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.