{kind=link}

Yen recovered modestly during the Asian session as Japanese equities edged lower, but both moves lacked conviction. The pullback in the Nikkei 225 was mild, and the corresponding FX response suggests investors see little reason to reassess the broader trend.

Geopolitical developments are weighing on Japanese sentiment after China imposed export curbs on selected dual-use items destined for Japan. The measures cover goods and technologies with both civilian and military applications, including rare earths essential for chipmaking and drone production. The restrictions appear linked to comments by Prime Minister Sanae Takaichi last November on Taiwan. Beijing reacted strongly after Takaichi warned that a Chinese attack on the island could represent an existential threat to Japan, further straining already fragile ties.

Japan’s dependence on China remains significant, with around 60% of rare-earth imports sourced from country. Still, the lack of clarity on which items are affected makes it difficult to gauge the real economic impact for now. Meanwhile, some observers argue the move may be largely symbolic. China has historically avoided actions that would severely disrupt Japanese industry, and the latest step may be intended to stir domestic criticism of Takaichi rather than materially damage bilateral trade.

In contrast, Australian Dollar stayed well bid after extending gains earlier in the day, even as inflation data surprised slightly to the downside. The softer CPI reduced pressure for an immediate February hike by the RBA, but did little to derail the broader tightening narrative. Even with the softer headline outcome today, disinflation in underlying pressures remains modest. That persistence keeps the door open for rate hikes later in the year, even if February proves too soon.

Markets currently price around a two-thirds chance of a February hold, with a hike expected by June and a strong probability of a second before year-end. Nevertheless, RBA policymakers are expected to place greater weight on the full Q4 inflation report later this month. A 0.9% quarter-on-quarter or higher rise in core inflation could still push the RBA toward tightening in February.

In FX performance terms this week so far, Aussie continues to lead, followed by Sterling and Yen. Loonie sits at the bottom, with Swiss Franc and Euro also under pressure. Dollar and Kiwi are trading d in the middle. Focus now shifts to US ADP jobs and ISM Services PMI later today, though the decisive catalyst is expected to be Friday’s non-farm payrolls.

In Asia, Nikkei fell -1.06%. Hong Kong HSI is down -1.12%. China Shanghai SSE rose 0.05%. Singapore Strait Times is flat. Japan 10-year JGB yield fell -0.008 to 2.122. Overnight, DOW rose 0.99%. S&P 500 rose 0.62%. NASDAQ rose 0.65%. 10-year yield rose 0.014 to 4.179.

Australia CPI cools more than expected to 3.4%, easing near-term pressure on RBA

Australia’s inflation cooled more than expected in November, offering some relief after months of intensifying price pressure. Headline CPI slowed from 3.8% yoy to 3.4%, undershooting expectations of 3.6%. Trimmed mean inflation eased modestly from 3.3% yoy to 3.2%, pointing to a gradual moderation in underlying pressures.

The slowdown was broad-based. Annual goods inflation fell to 3.3% yoy from 3.8%, driven largely by a sharp deceleration in electricity prices, which rose 19.7% over the year compared with 37.1% previously. Services inflation also eased, slowing to 3.6% yoy from 3.9%, helped by a pullback in domestic holiday travel costs after October’s school-holiday and major sporting-event surge.

Despite the moderation, price pressures remain elevated in key areas. Housing inflation stayed firm at 5.2% yoy, while rents and medical services continued to rise at a solid pace. The data ease immediate pressure on the RBA for rate hike. But with inflation still well above target range, policymakers are likely to remain cautious about declaring victory too early.

Japan PMI composite finalized at 51.1, but confidence and hiring hold up

Japan’s service sector lost some momentum at the end of 2025, with Services PMI finalized at 51.6 in December, down from 53.2 in November. Composite PMI eased to 51.1 from 52.0, marking a seven-month low.

According to S&P Global Market Intelligence Economics Associate Director Annabel Fiddes, services firms reported slower growth in activity and new orders, while manufacturing showed relative improvement. Despite softer demand signals, business confidence across Japan’s private sector remained firm, supporting a “solid and accelerated rise in employment”.

Cost pressures, however, remain a key challenge. Input prices rose at the fastest pace since April, driven by higher costs, prompting firms to lift selling prices at a solid rate. With demand conditions softening slightly, companies face a “difficult balance” between passing on higher costs to protect margins and maintaining competitiveness.

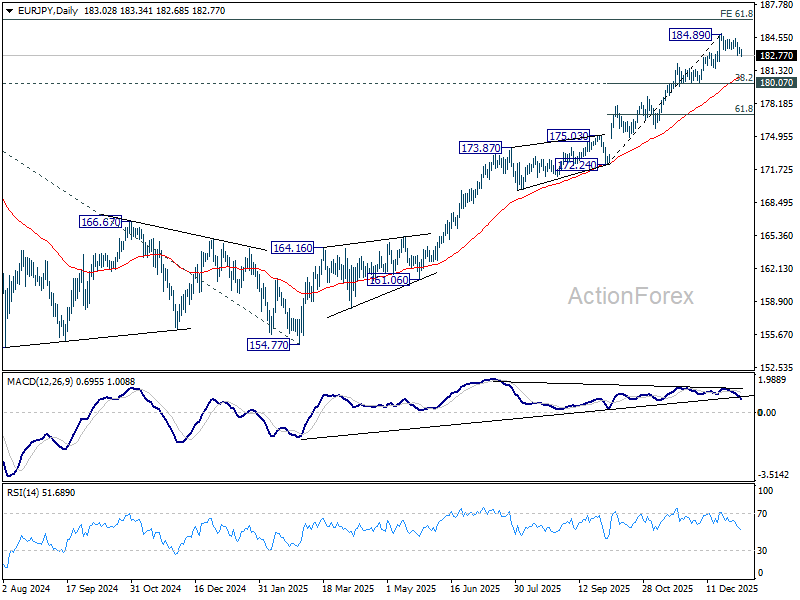

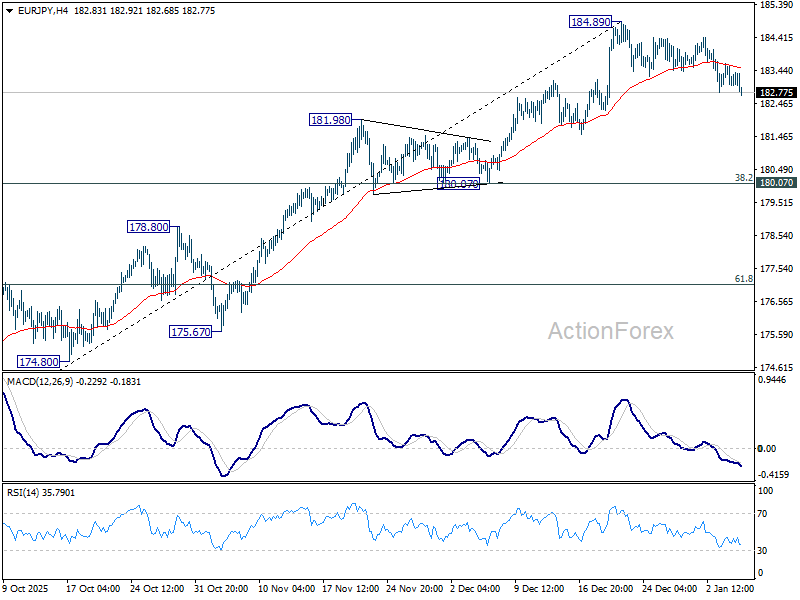

EUR/JPY Daily Outlook

Daily Pivots: (S1) 182.87; (P) 183.26; (R1) 183.53; More…

EUR/JPY edges lower today and the sustained trading below 55 4H EMA (now at 183.45) argues that fall from 184.89 short term top is already correcting the rally from 172.24. Intraday bias is mildly on the downside for 55 D EMA (now at 180.74). But strong support should emerge from 180.07 cluster (38.2% retracement of 172.24 to 184.89 at 180.05) to bring rebound. ON the upside, firm break of 184.89 will resume larger up trend to 186.31 fibonacci level.

In the bigger picture, up trend from 114.42 (2020 low) is in progress and should target 61.8% projection of 124.37 to 175.41 from 154.77 at 186.31. Considering bearish divergence condition in D MACD, upside could be capped by 186.31 on first attempt. Still, outlook will stay bullish as long as 55 W EMA (now at 172.16) holds, even in case of deep pullback. Sustained break of 186.31 will pave the way to 100% projection at 205.81 next.