{kind=link}

Yen recovered broadly today after Japan delivered its strongest verbal intervention in months, temporarily slowing the currency’s slide. The shift in tone came as USD/JPY neared 160, its strongest level since July 2024, prompting officials to push back more forcefully against what they described as excessive moves.

Crucially, the rhetoric was aimed at speed and volatility rather than level. Japan has repeatedly stressed opposition to speculative, one-sided moves, without defining a red line or objecting to depreciation per se. That distinction matters for markets still aligned with a structurally weaker-Yen view.

Finance Minister Satsuki Katayama said authorities would “take appropriate action against excessive currency moves without excluding any options,” calling the recent swings “extremely regrettable” and out of line with fundamentals. The comments marked a clear escalation in language, even if no action followed.

Japan’s top currency diplomat Atsushi Mimura echoed the warning, describing recent moves as “one-sided and rapid.” Pressed on whether intervention was on the table, he declined to be specific, stressing that volatility and speculative behavior — not the exchange rate level — were the real concern.

Despite the firmer tone, Yen’s rebound should be treated more as a pause rather than a reversal. The so-called “Takaichi trade” remains firmly in force, with Japanese equities continuing to surge. The Nikkei hit another record today, underlining persistent risk-on sentiment tied to domestic politics.

That backdrop is political. It is now confirmed that Prime Minister Sanae Takaichi plans to dissolve parliament next week and call a snap election, seeking public backing for expansionary spending plans. Liberal Democratic Party Secretary General Shunichi Suzuki said a fresh mandate is needed, noting that the public has yet to pass judgment on the current coalition arrangement. The prospect of fiscal stimulus continues to support equities and weigh on Yen.

Beyond Japan, central-bank independence is spreading as a sensitive global theme. New Zealand Foreign Minister Winston Peters publicly rebuked RBNZ Anna Breman for signing a statement in support of Fed Chair Jerome Powell, arguing the RBNZ should avoid involvement in US domestic politics.

The controversy followed a rare joint declaration by global central bank heads backing Powell and defending monetary independence. Peters said the governor should “stay in her New Zealand lane,” highlighting how politically charged the issue has become even outside the US.

Japan’s absence from the signatories also drew attention. According to government sources, the BoJ consulted officials informally but was unable to approve participation in time, reflecting election sensitivity and the delicate US relationship. Former BoJ board member Takahide Kiuchi said the episode highlight how the BoJ still operates within political constraints, even as it guards its neutrality.

In Europe, at the time of writing, FTSE is up 0.25%. DAX is down -0.37%. CAC is up 0.03%. UK 10-year yield is down -0.021 at 4.381. Germany 10-year yield is down -0.006 at 2.844. Earlier in Asia, Nikkei rose 1.48%. Hong Kong HSI rose 0.56%. China Shanghai SSE fell -0.31%. Singapore Strait Times rose 0.11%. Japan 10-year JGB yield rose 0.019 to 2.186.

US retail sales beat expectations with 0.6% mom growth in November

US retail sales posted a solid upside surprise in November. Headline sales rose 0.6% mom to USD 735.9B, beating expectations of a 0.4% increase.

The gains were broad-based. Sales excluding autos increased 0.5% mom to USD 597.2B, also above forecasts of 0.4%. Sales excluding gasoline climbed 0.6% mom to USD 683.0B. The data suggests that underlying consumption momentum remains intact rather than being driven by volatile components.

On a quarterly basis, total retail sales for the September–November period were up 3.6% from a year earlier.

China’s exports jump 6.9% yoy in Dec, US decoupling continues

China’s December trade data surprised to the upside, pointing to resilient external demand despite ongoing tariff tensions. Exports surged 6.6% yoy, more than double expectations of 3.0%. Imports rose 5.7% yoy, far exceeding forecasts of 0.9% and marking the strongest growth since September last year. The trade balance posted a USD 114.1B surplus, broadly in line with expectations.

However, the headline strength masked a deepening collapse in trade with the US. Shipments to the US plunged -30% yoy, extending a ninth straight month of contraction, while imports from the US fell -29% yoy. By contrast, China’s trade with other regions remained robust. Exports to the EU and ASEAN climbed 12% and 11% respectively. While imports from Europe jumped 18%. Imports from Southeast Asia declined -5%.

For the full year, exports grew 5.5% while imports were flat, driving China’s trade surplus to a record USD 1.19T, up 20% from 2024. Trade with the US weakened sharply amid tariff frictions, with exports down -20% and imports falling -14.6%.

Commenting on the data, General Administration of Customs spokesperson Lv Daliang called for dialogue and negotiation, stressing that China–US trade relations should remain mutually beneficial.

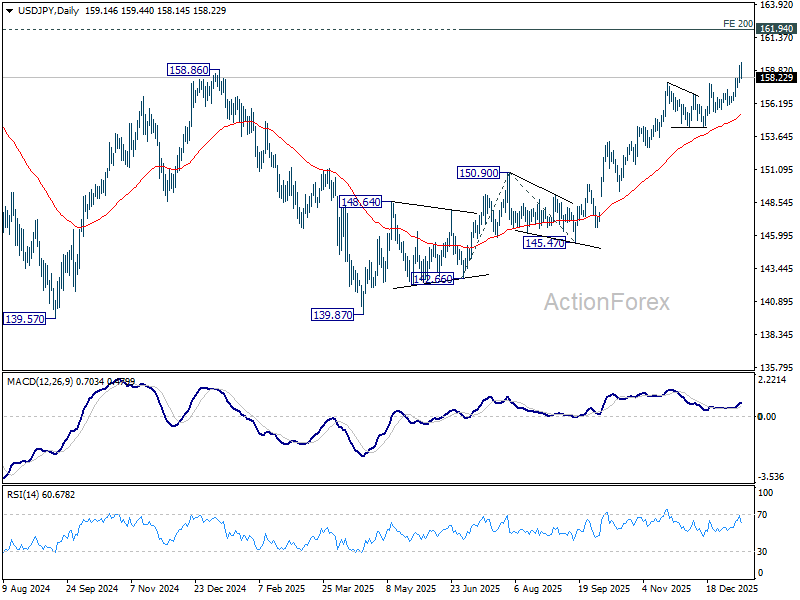

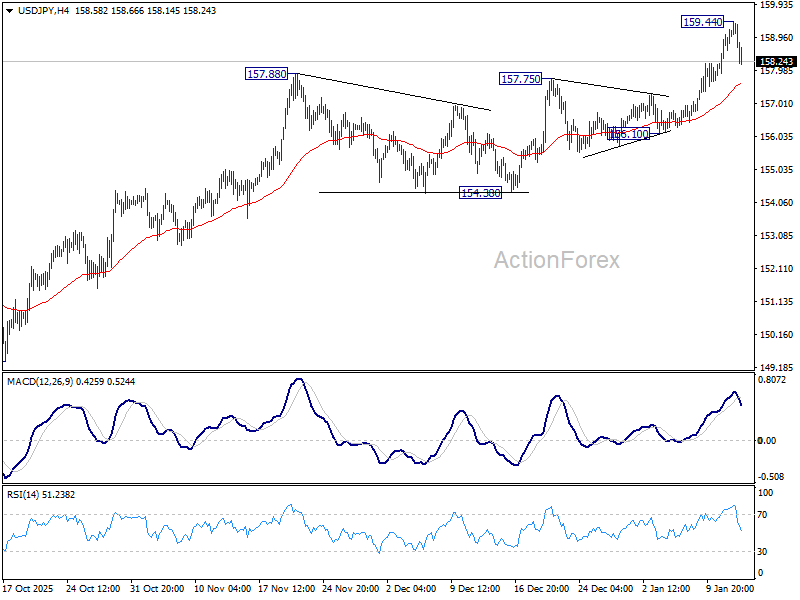

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 158.32; (P) 158.75; (R1) 159.61; More…

Intraday bias in USD/JPY remains neutral at this point. Retreat from 159.44 temporary top could extend lower. But downside should be contained above 156.10 support to bring another rally. On the upside, above 159.44 will resume larger rise from 139.87. Next target is 200% projection of 142.66 to 150.90 from 145.47 at 161.95, which is close to 161.94 high.

In the bigger picture, corrective pattern from 161.94 (2024 high) could have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 154.38 support will dampen this bullish view and extend the corrective range pattern with another falling leg.