{kind=link}

Market reaction to US President Donald Trump’s highly anticipated speech at the World Economic Forum was relatively muted, suggesting investors had already priced in a confrontational tone. Greenland remained the central issue for market participants. Trump’s remarks offered partial relief, as he appeared to rule out military action to secure control of the island, addressing one of the market’s most immediate tail risks.

Trump explicitly said he would not use force, stating that while the U.S. could act with “excessive strength,” he had no intention of doing so. That clarification removed the most extreme scenario from the near-term outlook and helped cap further risk escalation.

However, the relief was narrow. Trump continued to press firmly for U.S. control of Greenland, repeatedly framing the issue as one of strategic necessity, not negotiation posture. He argued that ownership—not leasing or basing rights—is essential for defense, saying the U.S. cannot protect Greenland under a lease arrangement. He framed the island as a future strategic battleground, emphasizing missile trajectories and North Atlantic security.

He also launched a pointed critique of Denmark, arguing it lacks the capacity to secure Greenland and asserting that the island is effectively part of North America. Trump said no country other than the U.S. could guarantee Greenland’s security. Crucially, Trump reiterated his intent to pursue immediate negotiations over acquisition, keeping geopolitical uncertainty firmly alive. While the threat of force was dialed back, the broader standoff with Europe remains unresolved.

Markets reflected this mixed message. U.S. equity indexes opened mildly higher, suggesting relief that rhetoric did not escalate further. Meanwhile, the 10-year Treasury yield eased back toward 4.28%, stabilizing after recent volatility. Yet beneath the surface, stress signals persist. Gold remains firm above 4,800, hovering just below the 5,000 psychological level. The inability of gold to correct meaningfully despite calmer headlines points to underlying distrust and hedging demand.

In FX markets, Dollar remains at the bottom of the weekly performance table, followed by Yen and Sterling. Kiwi Leads, with Swiss Franc and Aussie close behind, while Euro and Loonie sit mid-pack—consistent with a market that is calmer, but far from comfortable.

In Europe, at the time of writing, FTSE is up 0.19%. DAX is down -0.64%. CAC is up 0.18%. UK 10-year yield is down -0.006 at 4.456. Germany 10-year yield is up 0.015 at 2.876. Earlier in Asia, Nikkei fell -0.41%. Hong Kong HSI rose 0.37%. China Shanghai SSE rose 0.08%. Singapore Strait Times fell -0.38%. Japan 10-year JGB yield fell -0.056 to 2.288.

SNB Schlegel sees no issue with negative inflation prints if temporary

The SNB is not alarmed by recent soft inflation data, according to Chairman Martin Schlegel. He said inflation is expected to pick up, but the SNB is prepared to tolerate temporary negative readings, provided medium-term price stability remains intact.

“If we have some negative prints this year, for example, this is not a problem with the Swiss National Bank, because we look at the medium-term price stability,” he added.

He also pointed to recent global political turbulence as a driver of Swiss Franc appreciation, reflecting its traditional safe-haven role. On reserve management, Schlegel declined to comment directly on whether the exchange-rate move would lead to changes in Dollar holdings, but reiterated the SNB’s commitment to diversification across currencies and asset classes, noting the bank continuously reviews its “investment universe” and stands ready to act if needed.

ECB’s Lagarde: Tariffs manageable, Trump’s constant reversals more damaging

ECB President Christine Lagarde said she expects only a “minimal” inflationary impact from additional U.S. tariffs, arguing that Eurozone price pressures remain firmly under control. Speaking to RTL, Lagarde noted that inflation is currently around 1.9%, leaving little scope for tariffs to materially disrupt the ECB’s inflation outlook.

Though, she acknowledged that the impact would not be evenly distributed, with Germany likely more exposed than France given its export-heavy manufacturing base. However, Lagarde argued that Europe would be far more resilient if it focused on removing non-tariff trade barriers within the EU, strengthening internal trade and competitiveness rather than reacting defensively to external shocks.

Lagarde’s sharper warning was reserved for uncertainty, not tariffs themselves. Referring to renewed threats from US President Donald Trump, who has vowed to impose escalating tariffs on several European countries over Greenland, she said the “constant reversals” and unpredictability pose a more serious risk. Trump, she added, often takes a transactional approach, setting demands at “sometimes completely unrealistic” levels.

UK CPI rises to 3.4%, core holds at cycle low of 3.2%

UK inflation firmed at the end of 2025, with headline pressure coming in slightly hotter than expected. CPI rose to 3.4% yoy in December, up from 3.2% and above expectations of 3.3%, while prices increased 0.4% mom, pointing to ongoing near-term inflation momentum.

The upside in headline inflation, however, masked relative stability in underlying pressures. Core CPI—excluding energy, food, alcohol and tobacco—was unchanged at 3.2% yoy, undershooting expectations of 3.3%, and marking the joint-lowest reading since December 2024. Core inflation was last lower in September 2021, reinforcing the view that underlying disinflation progress, while slow, remains intact.

By component, services inflation edged up to 4.5% yoy from 4.4%, keeping the sector firmly in focus for the BoE, while goods inflation rose to 2.2% from 2.1%.

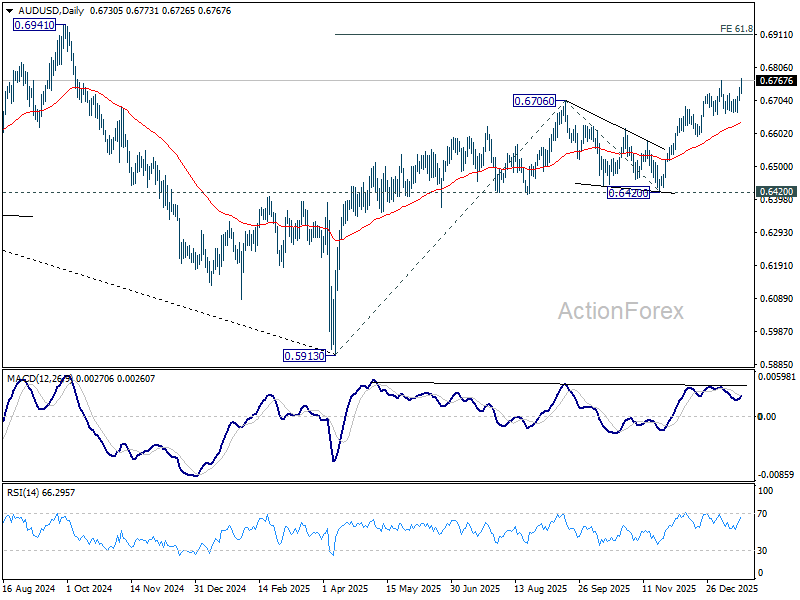

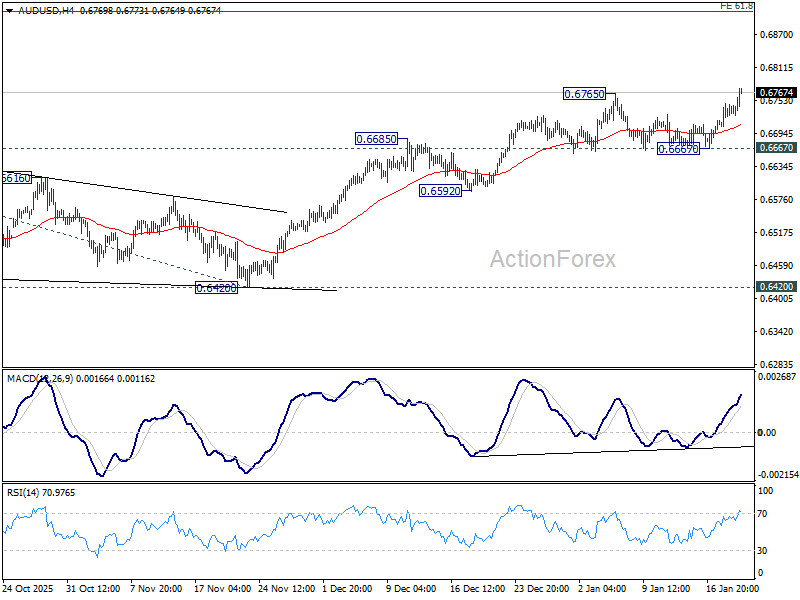

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.6713; (P) 0.6730; (R1) 0.6753; More...

AUD/USD’s rally from 0.5913 resumed by breaking through 0.6765 resistance today. Intraday bias is back on the upside. Further rise should be seen to 61.8% projection of 0.5913 to 0.6706 from 0.6420 at 0.6910 next. For now, near term outlook will stay bullish as long as 0.6667 support holds, in case of retreat.

In the bigger picture, current development argues that rise from 0.5913 (2024 low) is reversing whole down trend from 0.8006 (2021 high). Further rally should be seen to 61.8% retracement of 0.8006 to 0.5913 at 0.7206. This will remain the favored case as long as 0.6420 support holds, even in case of deep pullback.