{kind=link}

Dollar fell broadly again today, pressured by renewed risk appetite as global equities pushed higher. The greenback struggled to attract safe-haven demand despite lingering geopolitical and trade uncertainties, with investors favoring higher-beta currencies instead.

Asian markets set the tone. Both Nikkei 225 and KOSPI hit fresh record highs, tracking the tech-driven rebound in the US overnight. Hardware and AI-linked names continued to draw inflows as dip-buying behavior dominated. The AI disruption theme remains ever-present in markets, but it has yet to spark a durable correction. Instead, volatility episodes are being treated as opportunities to add exposure rather than exit positions.

Trade and geopolitical risks continue to simmer in the background. Tariff uncertainty and elevated tensions with Iran have injected caution, but they have not derailed the broader constructive tone. Risk appetite may be tempered, but it is not reversing. Many analysts now place roughly a 50% probability on a US-led military strike against Iran. That risk has been reflected in higher oil and precious metals prices, yet broader asset classes show limited signs of stress.

Attention now turns to the next round of US-Iran talks in Geneva tomorrow. Diplomatic signals will be closely scrutinized, especially after President Donald Trump reiterated in his State of the Union address that negotiations are ongoing and that he prefers a diplomatic resolution.

On trade, Trump’s remark that tariff revenue could eventually replace federal income tax reinforced the message that tariffs are a structural pillar of his policy agenda. Markets increasingly see tariffs as permanent features rather than temporary tactics.

In currency markets, Aussie led gains, buoyed by improved sentiment and firmer domestic inflation data that strengthens expectations of another rate hike from the RBA in May. Kiwi and Sterling followed, also benefiting from the risk-positive backdrop. In contrast, Dollar languished at the bottom of the performance board, trailed by Loonie and Yen. Euro and Swiss Franc held mid-pack.

In Asia, Nikkei closed up 2.30%. Hong Kong HSI is up 0.42%. China Shanghai SSE is up 0.66%. Singapore Strait TImes is down -0.26%. Japan 10-year JGB yield is up 0.022 at 2.135. Overnight, DOW rose 0.76%. S&P 500 rose 0.77%. NASDAQ rose 1.04%. 10-year yield rose 0.004 to 4.033.

Australia trimmed mean CPI climbs to 3.4%, RBA hike seen inevitable

Australia’s monthly CPI for January came in hotter than expected, reinforcing expectations of further tightening from the RBA. Headline inflation held unchanged at 3.8% yoy, above the 3.7% consensus and marking the joint highest reading since mid-2024.

More concerning for policymakers, trimmed mean CPI rose from 3.3% yoy to 3.4%, also exceeding forecasts and standing at its highest level since Q3 2024. Core inflation has now been at or above 3% since July 2025, remaining clearly outside the RBA’s 2–3% target band.

Housing (+6.8%), food and non-alcoholic beverages (+3.1%), recreation and culture (+3.7%), were the largest contributors to annual price pressures.

Markets had already leaned toward a May rate hike, and today’s data does little to challenge that view. Some economists argue the RBA may be “a little bit behind the curve,” risking a scenario where inflation becomes entrenched and requires more forceful tightening later. With price pressures proving persistent, another rate increase is increasingly viewed as close to inevitable.

CPI supports AUD, but breakout pending; AUD/CAD bullish, GBP/AUD bearish

Australian Dollar strengthened following January’s stronger-than-expected CPI data, but the move has resembled a “steady climb” rather than a “breakout surge”. While markets interpreted the firm headline and core readings as reinforcing the hawkish stance of the RBA, positioning remains measured.

One reason is that a May rate hike is already largely priced in. After the RBA’s hawkish increase earlier this month, traders had moved quickly to factor in another step. The latest CPI print confirms that narrative but does not materially extend it. For further upside momentum, markets would likely need to price tightening beyond May. That, however, may depend more heavily on the comprehensive Q1 quarterly inflation report due April, rather than the monthly indicator.

As RBA economic analysis chief Michael Plumb noted yesteday, it will take time to understand the properties and seasonal patterns of the new monthly data. For now, policymakers continue to place greater weight on quarterly measures, limiting the immediate impact of monthly fluctuations.

Global uncertainty also tempers enthusiasm. Ongoing trade tensions, fresh US tariff measures, and persistent US–Iran geopolitical risks act as a natural ceiling for risk-sensitive currencies like the Aussie.

Still, the broader tone for Aussie remains bullish. With inflation holding above target and core measures edging higher, the policy bias is clearly toward further tightening, keeping AUD underpinned on dips.

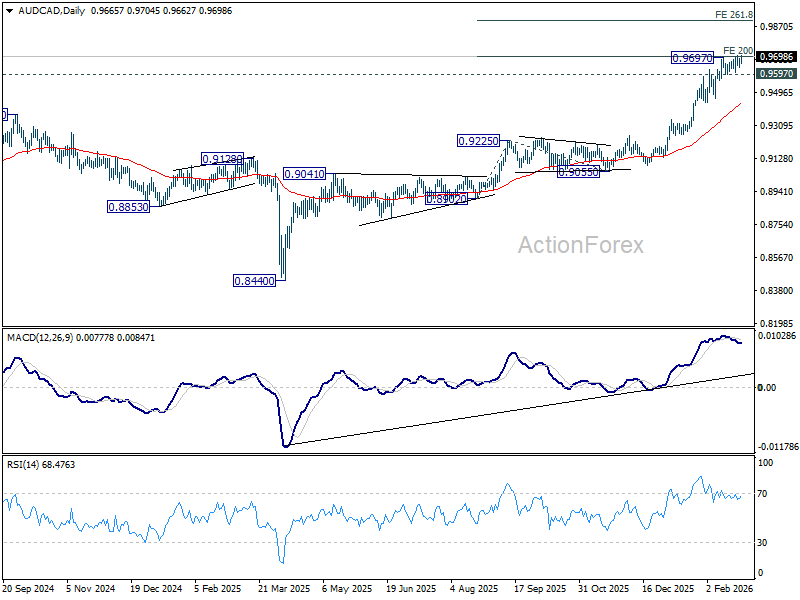

Technically, AUD/CAD has returned to test 0.9697 resistance level with today’s bounce. Decisive break would confirm resumption of the broader rally from the 0.8440 (2025 low) and open the way toward 261.8% projection of 0.8902 to 0.9225 from 0.9055 at 0.9901.

However, failure to clear that resistance cleanly could invite consolidation. Break below 0.9597 support would would bring deeper correction to 55 D EMA (now at 0.9439) first.

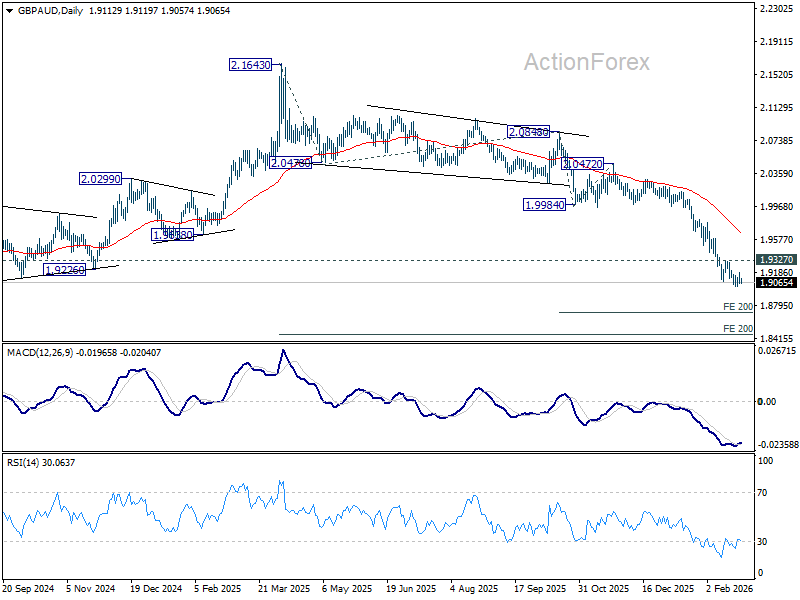

While GBP/AUD shows waning downside momentum as daily MACD divergence emerges, there is no clear sign of bottomg yet. The downtrend from 2.1643 (2025 high) high remains intact, with next target at 200% projection of 2.0848 to 1.9984 from 2.0472 at 1.8744.

However, firm break of 1.9327 resistance will indicate short term bottoming, and bring stronger rebound towards 55 D EMA (now at 1.9674).

Fed’s Collins sees mildly restrictive rates on hold “for some time”

Boston Fed President Susan Collins indicated that the Fed is likely to keep interest rates steady “for some time”, pointing to improving labor market conditions and unresolved inflation pressures. In remarks delivered at at event overnight, she said employment data show “at least some more signs” of stability.

Collins argued that after 175 basis points of easing, policy is now only mildly restrictive and may already be close to neutral. Given that backdrop, she said it is “quite likely” the current rate range will remain “appropriate” while officials seek “more evidence” that inflation is firmly moving back toward 2%.

Turning to trade policy, Collins noted that the Supreme Court’s ruling against sweeping tariffs injects fresh uncertainty into the outlook. She warned that if companies have already passed higher import costs through to consumers, those price increases are unlikely to be reversed, potentially keeping inflation elevated.

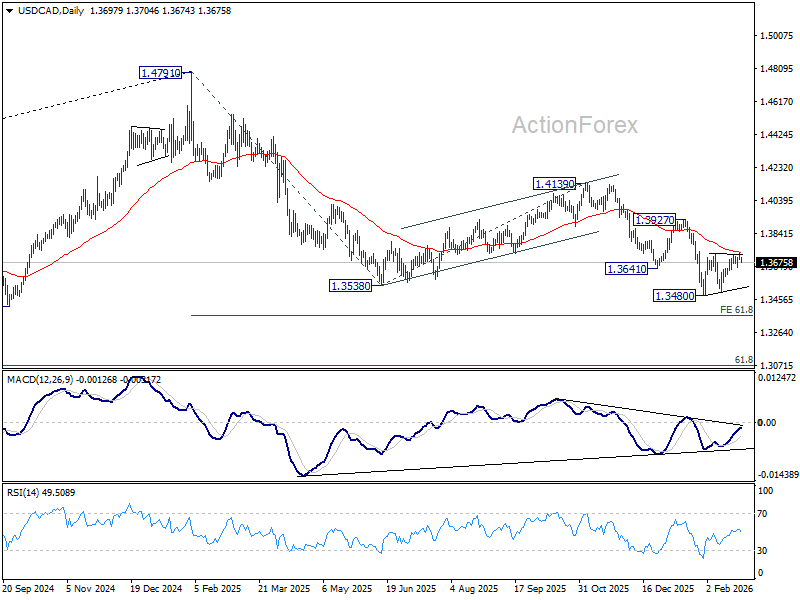

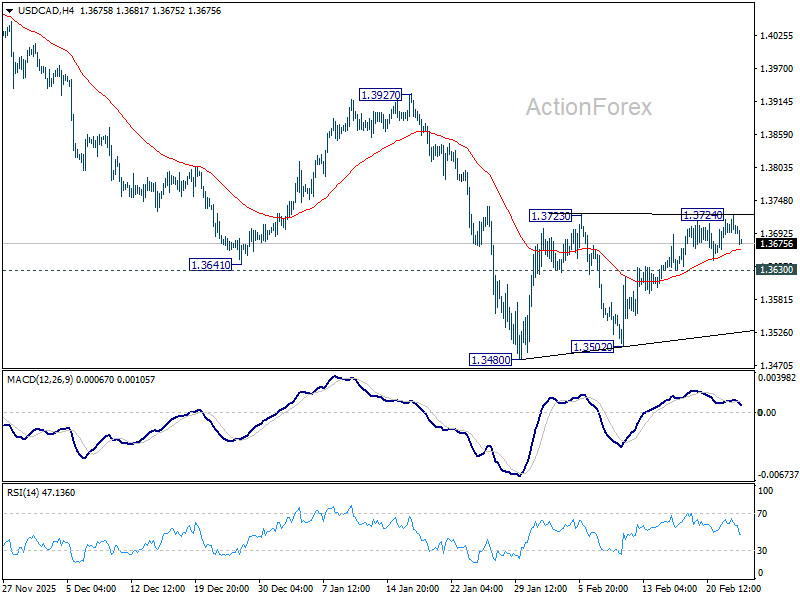

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3686; (P) 1.3705; (R1) 1.3719; More…

USD/CAD edged higher to 1.3724 but quickly retreated. Intraday bias stays neutral for the moment. Consolidations from 1.3480 is in progress and stronger rebound might be seen. But upside should be limited by 55 D EMA (now at 1.3733) to complete the pattern. On the downside, below 1.3630 minor support will bring retest of 1.3480 low. Firm break there will resume larger down trend from 1.4791 to 61.8% projection of 1.4791 to 1.3538 from 1.4139 at 1.3365. However, sustained break of 55 D EMA will bring further rise to 1.3927 resistance and above.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. For now, medium term outlook will be neutral at best, until there are signs that the correction has completed, or that a bearish trend reversal is confirmed.