Global markets are attempting to recover from the shock of a brutal Asian session as trading moves into Europe. Major European indices have managed to stage a modest rebound, helped in part by strong policy signaling from the US aimed at stabilizing energy markets. However, the recovery remains fragile. The underlying risks tied to the widening Middle East conflict have not disappeared, and markets remain highly sensitive to developments in the Strait of Hormuz.

While oil prices have eased slightly from earlier spikes, the geopolitical premium remains firmly embedded in energy markets. WTI crude has retreated from its session highs but is still trading near 75, well above levels seen before the escalation . The persistence of this war premium suggests that traders remain cautious about the potential for further disruptions to global oil flows.

The threat to shipping routes has become the central economic concern. Tanker traffic through the Strait of Hormuz had plunged earlier in the week as vessels avoided the area amid escalating military risks. In response, the U.S. government has moved to reassure markets that energy supply lines will remain protected.

Treasury Secretary Scott Bessent confirmed that Washington will introduce a series of measures aimed at supporting the flow of oil through the Persian Gulf. One key initiative involves the U.S. International Development Finance Corporation providing insurance coverage for oil tankers and cargo vessels operating in the Gulf region. This measure is designed to prevent insurers from withdrawing coverage and paralyzing energy shipments.

The announcement follows remarks from President Donald Trump, who said the US could deploy naval escorts to protect tankers navigating the Strait of Hormuz if necessary. Together, these measures have acted as a financial “tourniquet” for global markets.

Yet the improvement in market mood is being counterbalanced by another source of uncertainty: trade policy. The U.S. administration confirmed that its recently announced global tariff measures will soon take effect. Bessent said the planned 15% global tariff will be implemented this week.

More importantly, the Office of the U.S. Trade Representative and the Commerce Department will conduct additional studies that could justify further trade restrictions. In around five months time, Bessent expected tariffs to be back to the level before they were struck down by the Supreme Court.

The combination of geopolitical risk and rising trade tensions is keeping investors cautious. U.S. equity futures are currently hovering near flat levels, suggesting that traders remain reluctant to take aggressive positions.

Currency markets reflect a similar sense of restraint. Most major currency pairs remain within the previous session’s ranges, indicating that volatility has cooled for now. Even so, Dollar continues to dominate as the preferred safe-haven asset this week. Canadian Dollar is the second-strongest performer, benefiting from higher oil prices, while Yen holds the third position. Euro remains the weakest major currency, while Swiss Franc and Kiwi follow close behind. Sterling and Aussie trade in the middle of the performance table.

In Europe, at the time of writing, FTSE is up 0.87%. DAX is up 1.63%. CAC is up 1.12%. UK 10-year yield is down -0.007 at 4.400. Germany 10-year yield is up 0.004 at 2.770. Earlier in Asia, Nikkei fell -3.61%. Hong Kong HSI fell -2.01%. China Shanghai SSE fell -0.98%. Singapore Strait Times fell -2.11%. Japan 10-year JGB yield fell -0.014 to 2.119.

US ADP jobs grow 63k, pay premium for job switchers falls

US private sector employment grew moderately in February, coming in stronger than market expectations. Figures from ADP showed payrolls increasing by 63k during the month, compared with forecasts of around 45k.

The increase was driven primarily by the services sector, which added 47k jobs, while goods-producing industries contributed 16k. Small companies accounted for most of the growth, adding 60k positions. Large firms increased employment by 10k, while medium-sized businesses saw payrolls decline by -7k.

Wage growth remained steady but showed signs of cooling momentum for job changers. Pay growth for job-stayers held at 4.5% yoy, while wage gains for those switching employers slowed slightly from 6.4% to 6.3%.

According to Nela Richardson, hiring picked up and wage gains remain solid overall, but job growth remains concentrated in a limited number of sectors and the pay premium for switching employers has fallen to a record low.

Eurozone PPI surges 0.7% mom in January as energy costs climb

Eurozone industrial producer prices rose sharply in January, signaling renewed upstream inflation pressures. According to data from Eurostat, PPI increased 0.7% mom, significantly above expectations of a 0.2% rise.

The increase was broad-based across industrial categories. Prices for intermediate goods climbed 1.0% mom, while energy prices rose 1.3%. Capital goods prices increased 0.6% and durable consumer goods rose 0.8%, while non-durable consumer goods was the only category to decline, slipping -0.2%. Excluding energy, total industry prices still rose 0.6% during the month.

Across the wider European Union, PPI increased 0.8% mom. Among member states, the largest increases were recorded in Estonia (+13.7%), Bulgaria (+7.1%), and Finland (+6.9%). In contrast, producer prices declined in several countries, including Cyprus (-0.9%), Czechia (-0.7%), and both Germany and Slovakia (-0.6%).

Eurozone services PMI finalized at 51.9 as Germany leads growth

Eurozone business activity strengthened modestly in February, with services providing continued support to the region’s fragile recovery. The final PMI Services reading came in at 51.9, up from January’s 51.6. PMI Composite index was finalized at 51.9, up from 51.3 in the previous month

Among the major economies, Germany led the expansion with a composite reading of 53.2, marking a four-month high. Italy followed with a reading of 52.1, while Spain registered 51.5 despite slipping to a nine-month low. Ireland also remained in expansion territory at 52.5. France remained the weakest performer, however, with a composite reading of 49.9, still slightly below the 50 threshold separating expansion from contraction.

According to Cyrus de la Rubia of Hamburg Commercial Bank, the data suggest the ECB may have little reason to consider additional rate cuts in the near term. He noted that service sector costs remained elevated in February, driven by higher wages as well as rising energy and transport expenses. Germany could increasingly become the growth engine of the eurozone, as expanding infrastructure and defence spending begin to support broader economic activity.

UK PMI composite finalized at 17-month high, cost pressures persist

The UK service sector continued to expand steadily in February, with final PMI Services reading coming in at 53.9, only slightly below January’s 54.0. PMI Composite index was unchanged at 53.7, maintaining the 17-month high reached at the start of the year.

According to Tim Moore of S&P Global Market Intelligence, service providers reported rising new business inflows and stronger sales pipelines, driven largely by domestic demand. Businesses cited improved spending from both companies and consumers within the UK, though export orders remained relatively subdued and growth in that segment eased to a three-month low.

Despite the improving activity backdrop, employment declined across the sector. Companies continued to cut jobs as part of efforts to boost productivity and offset rising costs. Firms widely cited higher payroll expenses as a key driver of input cost inflation, alongside increases in food and technology costs. These pressures led to another robust rise in prices charged by service providers, with inflation in selling prices remaining close to January’s five-month high.

Swiss CPI rises 0.6% mom in February, annual inflation holds at 0.1%

Switzerland’s consumer prices rose more than expected in February, offering a modest sign of price pressure despite still subdued annual inflation. Data from the Federal Statistical Office showed CPI increased 0.6% mom, slightly above the expected 0.5% gain.

Core CPI, which excludes fresh and seasonal products as well as energy and fuel, rose by 0.2% mom on the month. The monthly increase was largely driven by higher domestic prices, which climbed 0.6%, while imported product prices rose 0.8%.

According to the FSO, the monthly increase was mainly driven by higher housing rents and air transport costs. Prices also rose for hotels and package holidays, while declines in items such as berries and fruit and vegetable juices partly offset the increase.

On an annual basis, headline inflation remained very subdued but slightly stronger than anticipated. CPI held steady at 0.1% yoy, slightly above expectations of a mild -0.1% yoy contraction. Core CPI edged down from 0.5%. Domestic prices accelerated modestly from 0.5% to 0.6%. Meanwhile, imported prices continued to decline, falling further from -1.5% to -1.6%.

Australia Q4 GDP beats with 0.8% qoq growth, reinforcing RBA demand concerns

Australia’s economy expanded faster than expected in the fourth quarter, reinforcing concerns that domestic demand may still be running hotter than the RBA would like. GDP grew 0.8% qoq, beating forecasts of 0.7% and accelerating from the previous quarter’s 0.5% pace. On an annual basis, growth came in at 2.6% yoy, also above expectations of 2.2%.

The expansion was broad-based, with output rising in 17 of the economy’s 19 industries. Both public and private demand contributed equally to the result, each adding 0.3 percentage points to overall growth. Household activity also showed resilience, with discretionary spending increasing 0.4% during the quarter, helped by strong retail events such as Black Friday.

At the same time, households continued to rebuild financial buffers. The saving ratio climbed to 6.9%, the highest level in more than three years, while per capita GDP rose 0.9% yoy — its strongest reading since 2022.

The strength of the data places the RBA in a difficult position. Just a day earlier, Governor Michele Bullock warned that demand may be outpacing the economy’s capacity. The GDP figures appear to reinforce that view, suggesting the current 3.85% cash rate may not yet be restrictive enough to cool activity.

Japan PMI composite finalized at 53.9, firms pass rising costs to customers

Japan’s service sector maintained steady momentum in February, with the final PMI Services reading edging up to 53.8 from January’s 53.7. The figure marks the strongest level since May 2024 and signals continued expansion in business activity, supported by improving demand conditions.

The broader picture for the economy also strengthened. PMI Composite rose to 53.9 from 53.1, pointing to the fastest pace of private sector expansion in nearly three years.

According to Annabel Fiddes of S&P Global Market Intelligence, the services sector recorded its quickest rise in sales in almost two years, while manufacturing performance also remained robust.

At the same time, cost pressures intensified across the private sector. Input costs climbed at a historically sharp pace, but improving demand allowed businesses to pass those increases on to customers. Selling prices rose at the fastest rate in nearly twelve years, suggesting firms are regaining pricing power while inflationary pressures remain elevated.

China PMIs show two-speed economy as official data contracts

China’s February PMI data revealed a widening divide between official indicators and private surveys, highlighting the uneven nature of the country’s economic transition.

The official manufacturing PMI, released by the National Bureau of Statistics of China, slipped to 49.0 from January’s 49.3, missing expectations and marking a second consecutive month of contraction. Activity in services and construction also stayed weak, with the non-manufacturing PMI edging slightly up from 49.4 to 49.5.

However, private-sector surveys paint a starkly different picture. According to data compiled by RatingDog, manufacturing PMI surged from 50.3 to 52.1, its strongest level since December 2020. The services PMI jumped even more sharply, rising to 56.7, the highest reading in nearly three years.

This divergence suggests a “dual-track” economy emerging in China. State-dominated sectors tied to construction and traditional heavy industry appear to be cooling, while private, export-oriented firms are experiencing a resurgence in demand, particularly in higher-value manufacturing and technology-linked industries.

Part of the discrepancy may also reflect seasonal distortions around the Lunar New Year. Large state factories often shut down for extended periods during the holiday, while smaller and more flexible private firms tend to ramp up production quickly to capture early-year export orders.

The February data may therefore capture both the growing pains of China’s structural shift toward “new productive forces” and the short-term disruptions created by the holiday cycle.

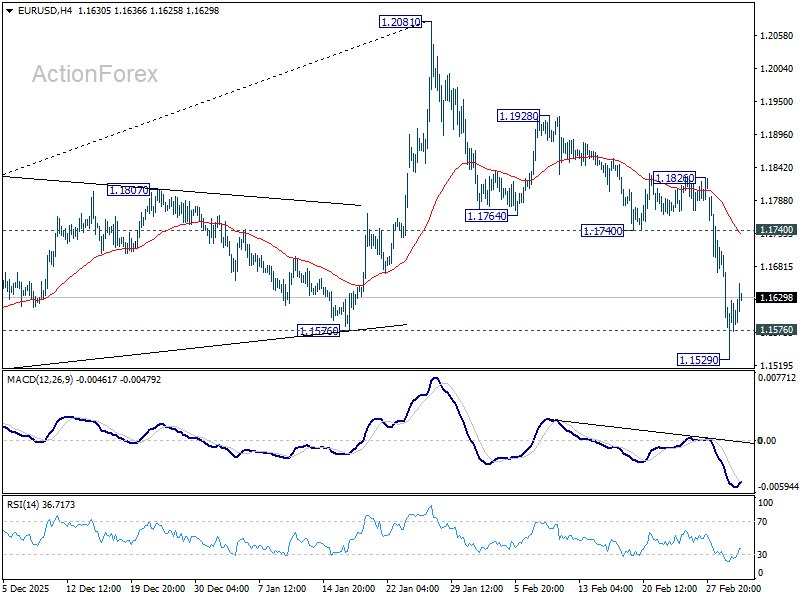

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1526; (P) 1.1617; (R1) 1.1703; More….

A temporary low should be formed at 1.1529 with current recovery. Intraday bias in EUR/USD is turned neutral first. On the downside, below 1.1529 will resume the fall from 1.2081. Sustained break of 1.1576 structural support would confirm rejection by 1.2 key psychological level. That should also confirm medium term topping on bearish divergence condition in D MACD. Further decline should be seen to 38.2% retracement of 1.0176 to 1.2081 at 1.1353 next. However, firm break of 1.1740 support turned resistance will revive near term bullishness, and bring stronger rebound back to retest 1.2081 high.

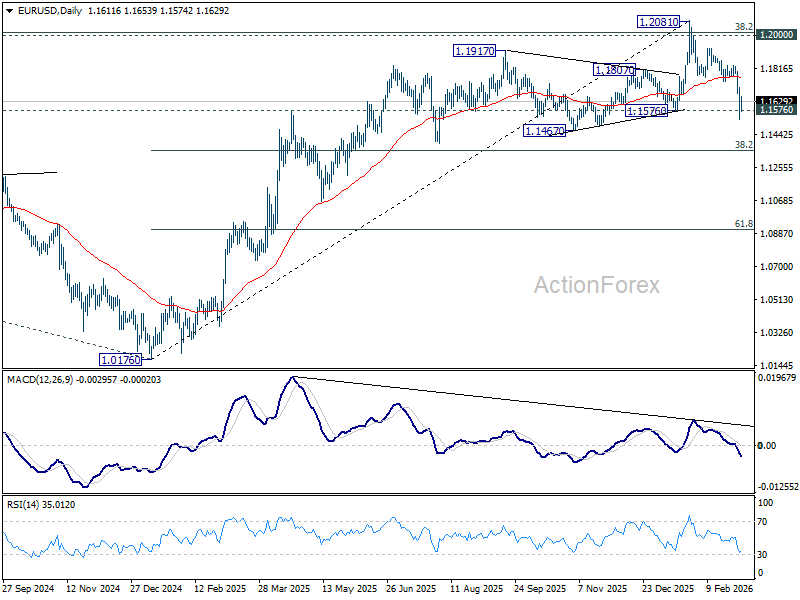

In the bigger picture, as long as 55 W EMA (now at 1.1494) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.

{kind=link}