Risk aversion deepened across global markets as the combination of escalating energy conflict and a more inflation-focused Federal Reserve weighed on sentiment. While the initial selloff in US equities overnight was triggered by a sharp spike in oil prices, the late-session decline pointed to a second driver—markets reacting to the Fed’s message that inflation risks heightened due to geopolitical uncertainty.

The escalation in the Iran conflict has moved into a more dangerous phase, with both sides targeting critical energy infrastructure. Reports that Israel struck Iran’s South Pars gas field were followed by retaliatory attacks on facilities in Saudi Arabia, the UAE, and Qatar, including the Ras Laffan LNG hub. This shift toward targeting core supply nodes signals a structural increase in energy risk premium.

Importantly, the nature of these attacks suggests that the disruption is strategic rather than temporary. By targeting alternative supply hubs, Iran appears to be attempting to “equalize the pain,” ensuring that global supply remains constrained even if its own exports are curtailed. This dynamic implies that elevated oil prices may persist even in the absence of continuous escalation.

Against this backdrop, the Fed’s latest decision and projections added further pressure on markets. While rates were left unchanged, the upward revision in inflation forecasts—particularly the rise in 2026 PCE to 2.7%—signaled that policymakers see a more persistent inflation path than previously expected.

Chair Jerome Powell reinforced this message, noting that inflation progress would continue but “not as much as we had hoped.” More importantly, he made clear that rate cuts remain conditional, stating that “if we don’t see that progress, then you won’t see the rate cut.” This underscores that the Fed is not prepared to ease policy in the face of rising inflation risks.

At the same time, Powell appeared to temper concerns about growth. While acknowledging that higher energy prices would exert “downward pressure on spending and employment,” he emphasized that the US’s position as a net energy exporter could offset these effects through increased production and investment.

The result is a policy framework that places greater weight on inflation risks than on potential growth headwinds. With inflation already trending higher before the onset of the Iran conflict, the additional energy shock is seen as compounding an existing problem.

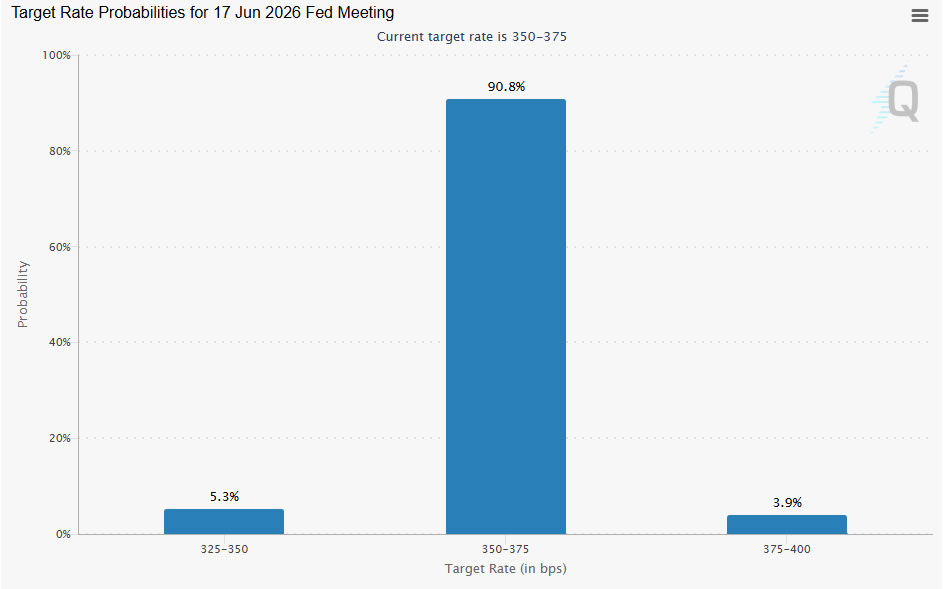

Fed fund futures pricing reinforces this interpretation. Markets now assign over 90% probability that rates will remain unchanged at 3.50–3.75% through the first half of the year, with only a marginal chance of a hike. This reflects growing acceptance that the Fed is in no rush to ease policy.

Market reaction reflects this recalibration. US equities extended losses into the close, and the selloff carried into Asian trading, indicating a broad reassessment of risk. However, the response in FX markets has been notably contained, with major pairs largely confined within recent ranges.

Meanwhile, currency performance suggests positioning rather than panic. Aussie led gains, followed by Kiwi and Euro, while Swiss Franc underperformed despite the risk-off tone. Dollar also failed to dominate, reflecting the absence of a clear flight-to-safety dynamic and reinforcing the view that markets are grappling more with inflation repricing than systemic stress.

With SNB, BoE, and ECB decisions ahead, attention now turns to whether other central banks will validate or push back against the emerging inflation narrative. For now, markets remain in a phase of controlled risk aversion, driven less by immediate crisis and more by the realization that inflation risks may persist longer than previously anticipated.

In Asia, Nikkei fell -3.50%. Hong Kong HSI is down -1.82%. China Shanghai SSE is down -1.15%. Singapore Strait Times is down -0.68%. Japan 10-year JGB yield is up 0.045 at 2.263. Overnight, DOW fell -1.63%. S&P 500 fell -1.36%. NASDAQ fell -1.46%. 10-year yield rose 0.057 to 4.259.

SNB, BoE, ECB set to hold as BoE votes and ECB guidance drive volatility

Rates are expected to stay unchanged, but BoE vote split and ECB policy signals could trigger FX moves as markets weigh inflation and growth risks. Read more.

BoJ holds rates, signals further hikes despite temporary inflation dip

BoJ kept rates at 0.75% and reaffirmed tightening bias, looking through a near-term inflation dip as wage growth and rising oil prices support outlook. Read more.

Mixed Australia employment data: Hiring strong, but job quality slips

Employment jumped 48.9k in February, but unemployment rose to 4.3% as full-time jobs fell and labour supply increased. Underlying softness tempers the strong headline. Read more.

NZ GDP disappoints at 0.2% as momentum fades into year-end

New Zealand GDP rose just 0.2% qoq in Q4, missing expectations and slowing sharply from Q3. Weak construction and flat per capita growth highlight a fragile recovery. Read more.

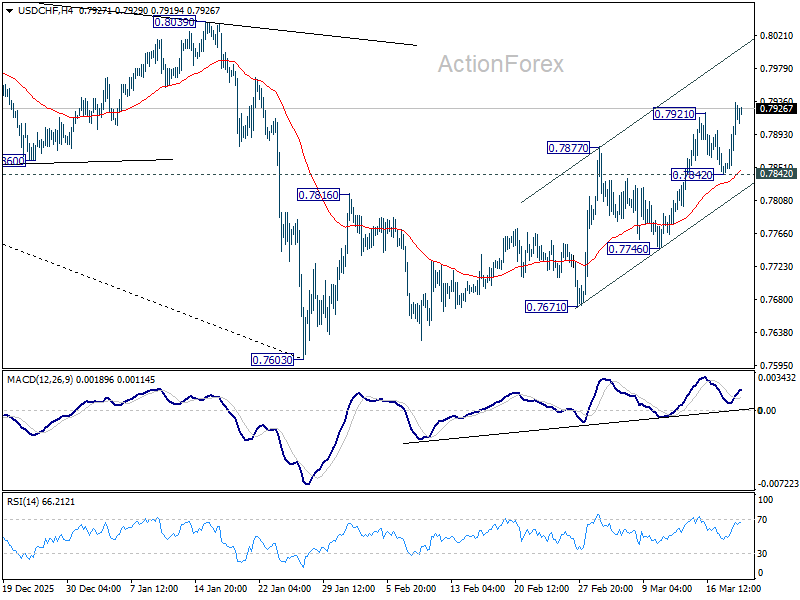

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7867; (P) 0.7903; (R1) 0.7967; More….

USD/CHF’s rise from 0.7603 resumed by breaking through 0.7921 temporary top. Intraday bias is back on the upside. The current rally is seen as correcting whole down trend from 0.9200. Next target is 38.2% retracement of 0.9200 to 0.7603 at 0.8213. On the downside, below 0.7842 support will turn intraday bias neutral first.

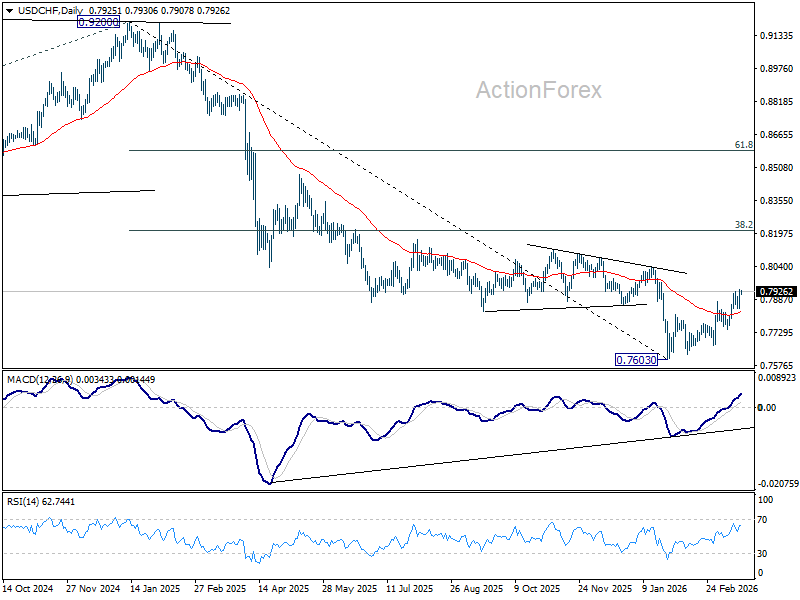

In the bigger picture, a medium term bottom should be in place at 0.7603 on bullish convergence condition in D MACD. Rebound from there is seen as correcting the fall from 0.9200 only. However, decisive break of 55 W EMA (now at 0.8091) will suggest that it’s probably correcting the larger scale down trend from 1.0146 (2022 high). On the other hand, rejection by the 55 W EMA will setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage.

{kind=link}