Dollar strength remained the defining theme in currency markets on Friday, although gains slowed somewhat as US markets observed the Juneteenth holiday. Investors continued to digest the Federal Reserve’s hawkish shift earlier this week, which revived expectations for another rate hike this year and left open the possibility of a second if inflation remains stubborn. With the market increasingly pricing a higher-for-longer Fed, the greenback has maintained broad support even as trading activity thinned.

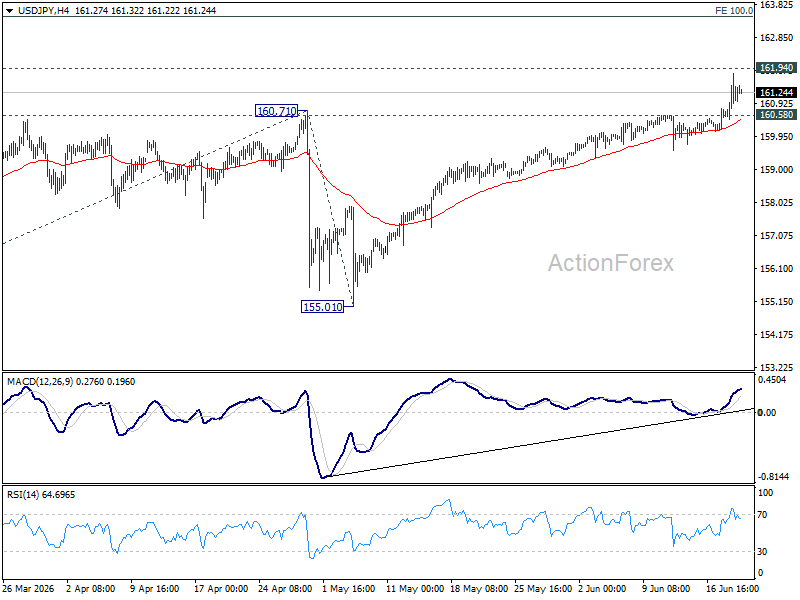

The clearest expression of that theme was USD/JPY’s surge above the 161 mark, extending its rally to fresh two-year highs. The move came despite renewed warnings from Japanese officials. Finance Minister Satsuki Katayama reportedly told G7 counterparts that Japan was “prepared to take decisive action on speculative moves” in foreign exchange markets. Bank of Japan Deputy Governor Ryozo Himino said the central bank was closely monitoring currency developments because of their implications for growth and inflation. So far, however, markets appear unconvinced that verbal intervention alone will be enough to counter a broad-based Dollar rally driven by widening rate differentials.

Elsewhere, Sterling staged a modest recovery following much stronger-than-expected UK retail sales data, which highlighted continued resilience in consumer spending. Nevertheless, the Pound remains among the week’s weakest performers as investors continue to scale back expectations for aggressive Bank of England tightening. Strong retail activity may help stabilize sentiment in the near term, but it has done little to alter the broader view that the BoE is more likely to remain on hold than deliver another rate hike.

For the week so far, Dollar remains the strongest major currency, followed by Aussie and Yen, while Kiwi, Sterling and Swiss Franc sit at the bottom of the rankings.

On the geopolitical front, optimism surrounding the US-Iran peace framework was tempered after follow-up negotiations scheduled in Switzerland were unexpectedly called off. Switzerland’s foreign ministry confirmed that talks planned at Bürgenstock would not proceed, while the White House said Vice President JD Vance would no longer travel to Switzerland due to unresolved logistical issues.

Yet the muted market reaction suggests investors still view the broader agreement as intact. Brent crude continues to trade around the USD 80 level rather than staging a renewed surge. Markets appear willing to give negotiators the benefit of the doubt for now, though a sustained return to pre-conflict oil prices will likely require tangible evidence that supply chains are normalizing, including a reopening of Strait of Hormuz shipping routes and a decline in elevated maritime insurance costs.

Canada Retail Sales Rise 0.6%, But Core Spending Remains Weak

The headline looked solid. The details were softer. Fuel-related spending lifted Canadian retail sales, but core purchases fell for a second consecutive month. Read More.

ECB’s Lane Says Staying at 2% Was Not an Option, Wunsch Signals Hike Risk

The ECB isn’t talking like a central bank that’s finished hiking. Philip Lane defended June’s rate increase, while Pierre Wunsch openly discussed the possibility of another move if inflation stays stubborn. Read More.

UK Retail Sales Surge 1.2% in May as Warm Weather and Promotions Boost Spending

Consumers ignored the gloom. UK retail sales more than doubled forecasts in May as warm weather, promotions and strong online demand drove the biggest upside surprise in months. Read More.

EUR/GBP Gains as Markets Scale Back BoE Tightening Expectations, More Upside Ahead

EUR/GBP gained as confidence in additional BoE rate hikes faded. Investors now see a higher hurdle for hawks to win support within the MPC, while the ECB has already delivered its latest rate increase. Read More.

Japan Core Inflation Holds at 1.4%, Fuel Subsidies Continue to Suppress Price Pressures

Japan’s inflation slowdown may prove temporary. Core-core inflation fell to its weakest pace since 2022, but growing pipeline pressures continue to point toward future price increases. Read More.

New Zealand Exports Jump 18%, But Faster Import Growth Limits Trade Surplus

Exports were strong. Imports were even stronger. New Zealand’s trade surplus narrowed despite an 18% surge in exports as domestic demand and petroleum imports drove a sharp rise in imports. Read More.

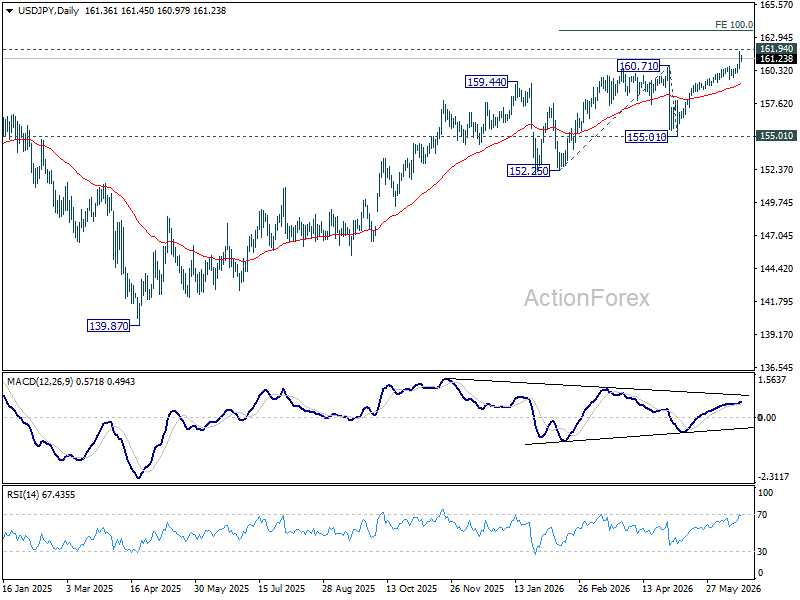

USD/JPY Daily Outlook

Intraday bias in USD/JPY remains on the upside for 161.94 high. Firm break there will resume larger up trend. Next near term target will be 100% projection of 152.25 to 160.71 from 155.01 at 163.47. On the downside, break of 160.58 minor support will turn intraday bias neutral first.

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. So, break of 161.94 is expected at a later stage to resume the long term up trend. However, sustained break of 55 W EMA (now at 155.13) will dampen this view and bring deeper fall back towards 139.87 to extend the pattern from 161.94.

{kind=link}