Dollar is extending recent rally against Euro and Swiss Franc in early US session. EUR/USD breached 1.19 handle as it’s now trying to get rid of 1.2 firmly. USD/CHF reaches as high as 1.0055 and breached 1.0037 resistance. Weak Eurozone data is a factor weighing on the comment currency, as seen in EUR/GBP too. Nonetheless, the greenback is still held in tight range against Sterling, Aussie and Loonie despite rally attempts. USD/JPY also recovers but struggle to extend through 109.39 yet. 1.3485 in GBP/USD, 0.7472 in AUD/USD and 1.2913 in USD/CAD are the levels to watch to confirm underlying momentum.

Eurozone Sentix investor confidence dropped to 19.2, lowest since Feb 2017

Eurozone Sentix investor confidence dropped to 19.2 in May, down from 19.6, missed expectation of 21.0. That’s the 4th decline in a row, and hit the lowest level since February 2017. Current situation index dropped 0.2 to 42.8, lowest since October 2017. Expectations dropped to -2, lowest since October 2014. Sentix noted that “uncertainties about the introduction of punitive US tariffs and the danger that this could lead to an expansion of protectionist measures are weighing on us.”

Eurozone retail PMI at 48.6, Italy sales decline accelerated sharply

Eurozone retail PMI dropped to 48.6 in April, down from 50.1. Weakness was driven by sharp decline in Italy which hit 21 month-low at 42.7. Germany retail PMI dropped to 9-month low at 51.0. France continued to outperform with retail PMI hit 2 month high at 50.1. Markit noted that “the latest data highlighted a disappointing month for the eurozone retail sector. Monthly sales were down for the first time for over a year as signs of restricted consumer demand and increased uncertainty begin to show. This was particularly evident in Italy, where the rate of decline in like-for-like sales accelerated sharply and was the most marked for the better part of two years.

And, “forward-looking indicators add to the dull picture, with falls in purchasing activity and stocks of goods suggesting retailers are taking an increasingly cautious approach to their business operations. The one shining light was a further rise in staffing numbers. That said, without a rebound in customer demand we may see employment slip back into contraction territory in the coming months as well.”

Also release in European session, Swiss CPI rose 0.2% mom, 0.8% yoy. Foreign currency reserves rose to CHF 757B

ECB research: Significant increase in protectionism could have material impact on global trade and output

In article titled “Implications of rising trade tensions for the global economy“, ECB researcher Lucia Quaglietti warned of the impact of escalation of trade tensions. Based on simulations carried out by ECB staff, in event of a significant increase in protectionism, “the impact on global trade and output could be material.” In particular, if US increases tariffs “markedly” on imported goods from all trading partners that “retaliate symmetrically”, the outcome for the world economy would be “clearly negative. And, “the impact could be particularly severe in the United States”

For other countries, those with “closest trade relations” with the US would be most negatively affected. And, “only a few open economies with little exposure to the tariff-imposing country may benefit from trade diversion effects, as they would gain competitiveness in third markets.”

In addition, the impact of trade tension escalation could be “felt via a number of channels. Higher import prices would lead to higher production costs and lower household purchasing power. Consumption, investment and employment will also be affected. Moreover, there will be economic uncertainty that leads to delay and consumer spending and business investment. Credit supply could be reduced with requirement for higher compensation. And there could be broad spill over to the global financial markets.

China FX reserves dropped to five month low in USD term

According to the latest data from People’s Bank of China, the country’s foreign exchange reserves dropped to a five month low in April. Reserves dropped USD 17.97B in April from USD 3.143T to USD 3.125T. In SDR terms, Foreign currency reserves rose 11.3 B from 2.162T to 2.173T. Gold reserves was unchanged at 59.24 Million oz. Total reserves dropped from USD 3.240T to USD 3.221T. In SDR terms, total reserves rose from 2.229T to 2.240T.

BoJ March meeting minutes: Not the time to consider stimulus exit yet

In the minutes of March BOJ meeting, some members emphasized the need to have the best communications to the markets. To be more specific, “it was important for the BOJ to thoroughly explain to the public … that the economy had not yet reached a phase where it should consider the timing and measures of a so-called exit from monetary easing,” Also “while normalization, or a gradual reduction in the degree of monetary accommodation, could become a topic for consideration in the future, the BOJ needs to explain to markets that normalization … would be different from monetary tightening,”

Australia NAB business condition hit record high, but RBA could delay rate hike to 2019

Australia NAB business condition rebounded notably from 15 to 21 in April. That’s also a rerecord high since the survey started in March 1997. Business confidence also rebounded from 8 to 10. Alan Oster, NAB Group Chief Economist noted in the release that the results reinforces the evidence of “robust” business activity. Except manufacturing and retail, conditions increased in all industries. And, strength in both business conditions and confidence suggest that “economic growth will strengthen and that over-time”.

Meanwhile, falling unemployment rate should “eventually translate into upwards pressure on private sector wages”. That would put RBA into a position to “start increasing the current emergency low policy rate:. NAB maintained the forecast for RBA to hike later this year. However, “as hard evidence of a firming in wages growth is yet to appear in the data, and unemployment for the moment stuck at around 5.5%, the risk is that any action by the RBA will be delayed into 2019”.

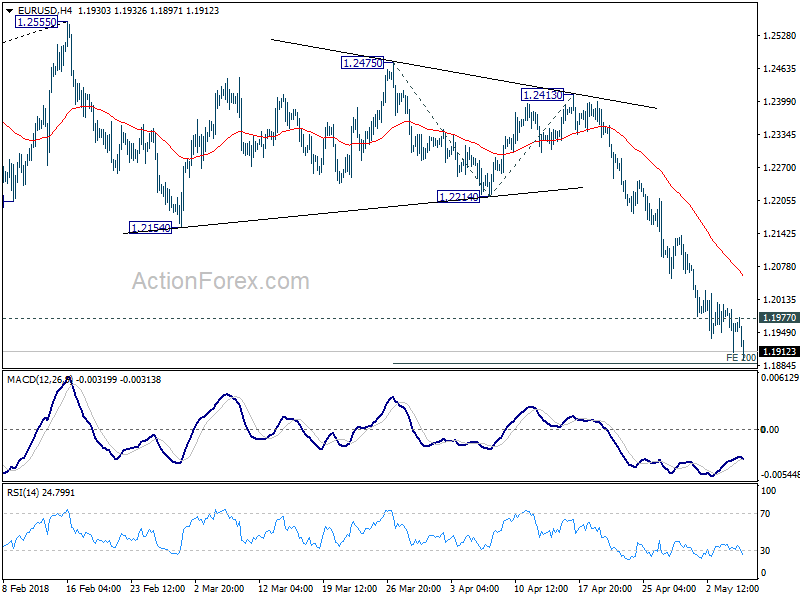

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1914; (P) 1.1955 (R1) 1.1999; More….

EUR/USD reaches as low as 1.1897 so far as recent decline continues. Intraday bias remains on the downside for 200% projection of 1.2475 to 1.2214 from 1.2413 at 1.1891. Firm break will target 261.8% projection at 1.1730. Meanwhile, considering diminishing downside momentum as seen in 4 hour MACD, break of 1.1977 minor resistance will indicate short term bottoming. In that case, intraday bias will be turned to the upside for 4 hour 55 EMA (now at 1.2064) or above for rebound.

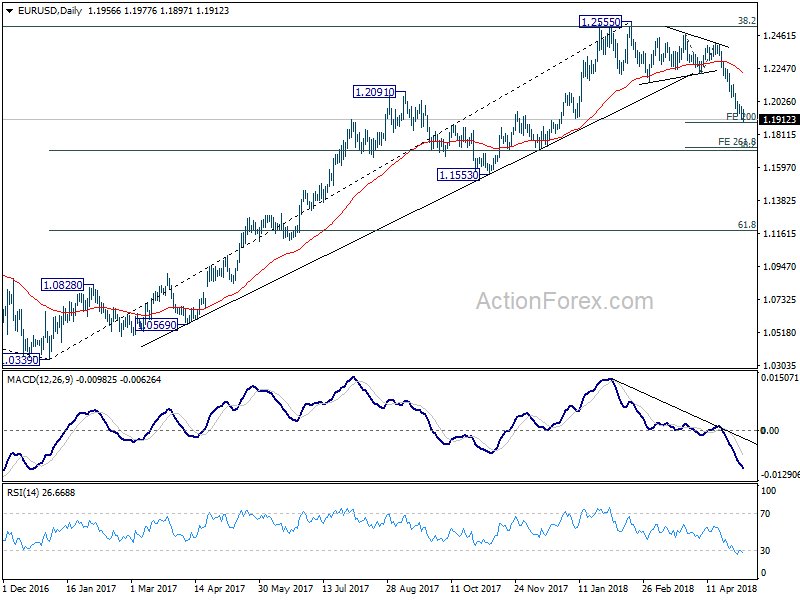

In the bigger picture, current decline and firm break of 1.2154 support confirms rejection by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. A medium term top should be in place at 1.2555 and deeper decline would be seen back to 38.2% retracement of 1.0339 to 1.2555 at 1.1708 first. With current downside acceleration, there is prospect of hitting 61.8% retracement at 1.1186 before completing the decline. But still, we’ll need to look at the structure to before deciding if it’s a corrective or impulsive move.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BoJ Minutes | ||||

| 1:30 | AUD | NAB Business Conditions Apr | 21 | 14 | 15 | |

| 1:30 | AUD | NAB Business Confidence Apr | 10 | 7 | 8 | |

| 6:00 | EUR | German Factory Orders M/M Mar | -0.90% | 0.50% | 0.30% | |

| 7:00 | CHF | Foreign Currency Reserves (CHF) Apr | 757B | 738B | ||

| 7:15 | CHF | CPI M/M Apr | 0.20% | 0.30% | 0.40% | |

| 7:15 | CHF | CPI Y/Y Apr | 0.80% | 0.90% | 0.80% | |

| 8:10 | EUR | Eurozone Retail PMI Apr | 48.6 | 50.1 | ||

| 8:30 | EUR | Eurozone Sentix Investor Confidence May | 19.2 | 21 | 19.6 |

{kind=link}